This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Dixon-James launched Resilient Wealth Management in 2020 and now manages about $250 million in advisory, brokerage and retirementplan assets. California RIA Deals & Moves: Focus Partners Wealth Merges in $5.6B based advisor Brandon Dixon-James has moved his book of business from Osaic to LPL Financial.

But to illustrate the relative protection that bonds may be able to provide compared to stocks, heres what happened to the bond market in the 2008 great financial crisis and recession and 2020 market crash. How do bonds perform during a recession? The chart below shows what happened to fixed income (bonds) in 2008.

Mike McGlothlin , CFP, CLU, ChFC, LUTCF, NSSA, Executive Vice President, Retirement, at Ash Brokerage , is the 2024 recipient of the Kenneth Black Jr. McGlothlin served on the Society of FSP National Executive Committee from 2018 to 2021 and was National President in 2020-2021. Leadership Award.

When you actively contribute to your workplace retirement account, invest in a separate portfolio , and funnel money into your savings account, it can be difficult to open – let alone manage – another account. IRAs are a great addition to your retirement savings journey. Do you plan on using the funds for K-12, college, or both?

The title of the Man article is Why Alpha Matters for Retirement Savers and in it, they make their case for portable alpha. It also fell 37% in the 2020 Pandemic Crash but it took that back in just four months. Portable alpha combines plain vanilla exposure with alternatives in such a way that leverages up.

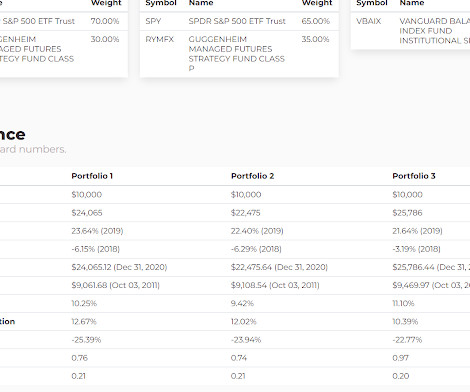

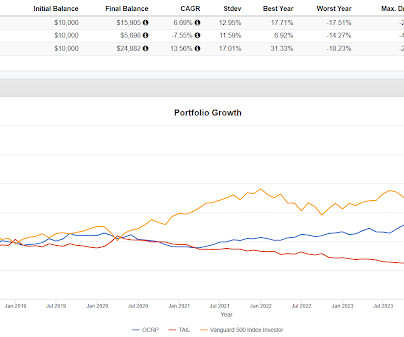

From 2020 on, VBAIX outperformed four times. And plugging into Testfol.io which goes back further and comparing it to VBAIX. Swensen did better over the course of the backtest with a little more volatility and bigger drawdowns. From 2000 to 2019, Swensen outperformed 14 times.

Portfolio 1 does not keep up with portfolios that have close to a normal allocation to equities but that portfolio was less volatile, did have an adequate real return and had much smaller drawdowns except in the 2020 Pandemic Crash. Another important observation is that Portfolio 1 is truly differentiated from 60/40.

Barron's wrote about the difficulty of spending down accumulated assets in retirement. You can see that the market started to care about price inflation around the time of the 2020 Pandemic Crash. Starting the clock in March 2020 gives a much different picture. Several quick hits today. XME is a client holding.

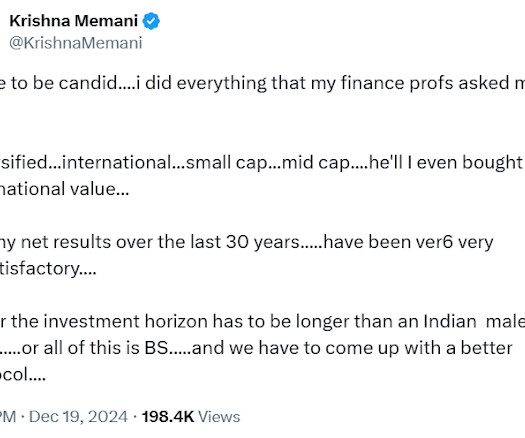

That leads to a Tweet from Krishna Memani who worked at Oppenheimer for a long time and who has been running the Endowment at Lafayette College since 2020. The min vol version is valid longer term but 2020 would have been a challenging time to hold.

It did decline about 5% in the 2020 Pandemic Crash and in 2022 it was up 1.36%. The backtest runs from the start of 2011 to the end of 2020. Um ok, but MSTR started buying Bitcoin in 2020. The USAF backtest and RAAX don't really look too similar to me. RAAX is much more volatile. In the period studied, CPI compounded at 2.5%

Yes the dividend funds did better than SPY in 2022 but not 2020 and in the financial crisis, I believe DVY was the only one that was around and being heaviest in financials, it did very badly. Lagging the market cap weighted SPY doesn't have to be a bad thing but the max drawdown numbers are not compelling and neither is the volatility.

It had a big drawdown in the 2020 Pandemic Crash which, ok, something like that sure but it had a surprisingly big drawdown in 2022 as you can see at 13%. It's growth rate since inception is 3.58% going back to September, 2018 but a lot of that comes from a 15% lift in 2021 (numbers per testfol.io).

In the partial year of 2020, Portfolio 1 was down 83 basis points while the S&P was up 18%. You can see just by looking that Portfolio 1 has actually taken a very different path to a similar result as the S&P 500. In 2021 it lagged the index by 12%.

The S&P 500 doesn't fall 20% in a quarter very often but obviously it can happen, it happened in Q1 of 2020 and the 3rd quarter of 2008 and I imagine there were others. The next day the fund would have a new buffer 20% down from there. If someone is actually going to use this, it is crucial they sell before the 20% threshold is hit.

Portfolio 1 lagged by quite a bit in 2019 and then even more in 2020. I took what he was saying to be expressed as follows in a portfolio. And compared to just VBAIX in Portfolio 2 The longer term result is interesting. Then it made it back in 2022 when it was only down 1.1%.

Looking at the 2020 Pandemic Crash, that was a fast decline but it played out over several weeks and while in real time we could recognize it as more of a crash than a long slow bear market, it didn't feel that fast. Moving to markets which hopefully we understand just a little better.

I saw where this was the worst single day drop since one of the bad days during the 2020 Pandemic Crash. Markets got pasted today of course. Ok, so a quick reminder that bad days have happened before, obvious statement. There have probably been more truly terrible market days than any of us could possible remember.

The worst deviation between the two was in 2020 when Portfolio 2 lagged by 740 basis points. The deviation was greater than 300 basis points only three times, including 2020. But invoking Karl Popper, it only takes one negative to disprove a theory.

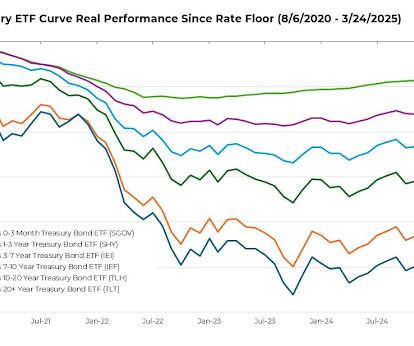

From its all time high in July 2020, TLH is down 41%. My assertion has been that retail investors want bonds to kick off an income stream without moving in price and that is not what you get with this sort of ETF. The price might literally never recover.

The post How Do You Turn Retirement Savings into a Reliable Income Strategy? How Do You Turn Retirement Savings into a Reliable Income Strategy? You’ve likely spent years building your retirement nest egg—saving diligently, investing wisely, and contributing to retirement accounts along the way.

The Bloomberg article included a couple of quotes about dialing down the equity exposure in retirement which has been the default approach but that chart shows why dialing down is a bad idea. The simplest example would be the person to retired at the end of 2007 and then 12 months later, the stock market was 39% lower.

It offered no crisis alpha though in the 2020 Pandemic Crash and in 2018 it was down 13.5% The article mentioned that SYLD benchmarks to midcap stocks. There's kind of a mixed bag here for the results. In addition to what is shown above, in 2022 SYLD only dropped 6.12%. versus 4.5%

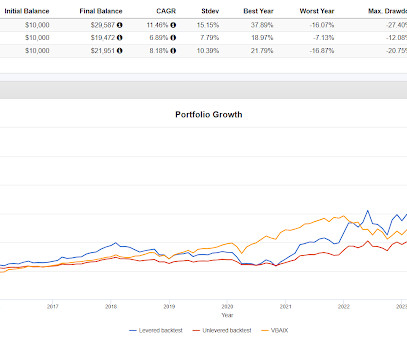

Both unleveraged versions were down 800-900 basis points less than the others during the 2020 Pandemic crash. In 2022, the two unleveraged versions were down 66 basis points and up 3.56% respectively while the leveraged version fell 6.87%, a great result, while plain VBAIX dropped 16.87%.

Both True North portfolios also held up relatively well in the 2020 Pandemic Crash which are the max drawdown numbers in the chart. Despite all the leverage, Portfolio 1 has a very smooth ride including up a lot in 2022. It's only down year was 2018 with a decline of 7.91%.

In 2022 it was only down 3.32% which is really good of course but in the 2020 Pandemic Crash it fell 20%. That might not be a useful way to look at though as the fund currently owns a lot of ETFs that weren't around in 2020. TRTY has had mixed results with crisis alpha.

The "endowment" result is very close to red line VBAIX every year except 2020 when it lagged by almost 600 basis point and 2022 when it outperformed by about 500 basis points. It did worse in the 2020 Pandemic Crash by 200 basis points which isn't problematic for how quickly everything snapped back. Is it this?

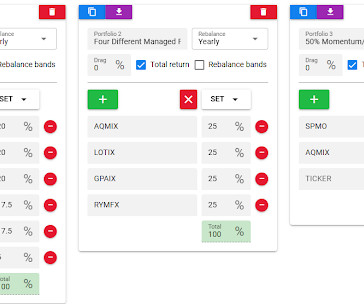

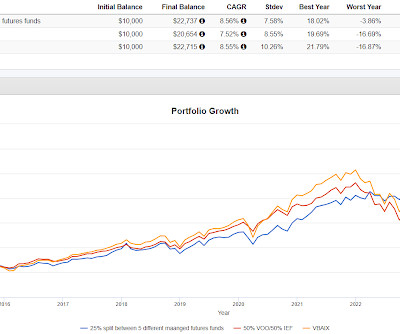

All five funds really struggled from 2015-2020 but there was variation among the five. You wouldn't say they are lowly correlated but the correlations aren't that tight so maybe there is some insulation against things going wrong versus putting 25% into just one managed futures fund. We looked at a similar chart the other day.

I expanded on it a little bit and noted it's not particularly relaxing but I would reiterate that this is a great time to lean forward and learn about some things in real time versus looking at a backtest from a benchmark event like the 2020 Pandemic Crash or 2022. All of the different factors have their moments in the sun.

It did go down almost 9% in the 2020 Pandemic Crash but that was just a fraction of what the S&P 500 dropped and in 2022, OCRP was up 9.15%. If they can have single stock ETFs why not an ETF with just two holdings? I threw tail in as well as the S&P 500. In late 2018 OCRP moved up when the market had a fast drop.

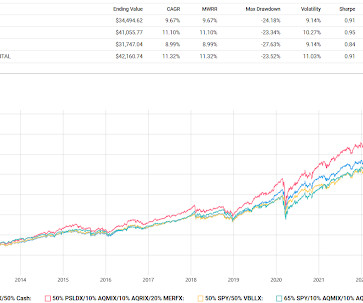

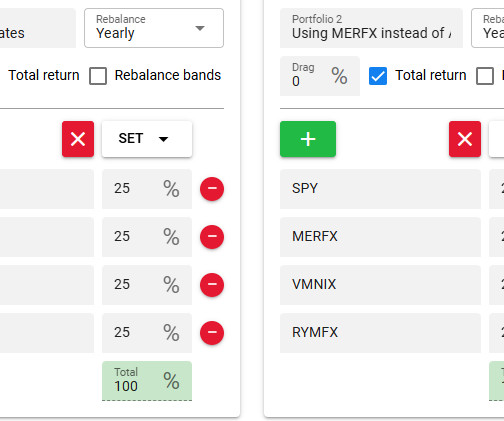

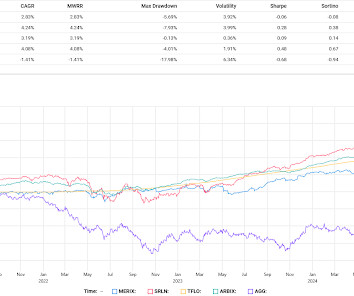

None of them helped though in the 2020 Pandemic Crash. MERIX is a client and personal holding. The 50/50 version is the most interesting to me. The 50/50 version did far and away the best in 2022. It probably will eventually unless the next bear market comes before that happens.

The struggles for AGG have been prolonged of course but it is also important to mention that MERIX, SRLN and ARBIX all got hit hard in the 2020 Pandemic Crash so they are not infallible but the snap back was quick and the hit was no where close to that of equities. AGG's duration isn't that long.

The 2022 numbers are of course favorable but they did get hit hard in the 2020 Pandemic Crash. Neither version differentiates in terms of volatility versus VBAIX but in 2022 the ACWI version was only down 4.84% and the SPY version was only down 4.75% versus 16.87% for VBAIX. This isn't radically different from a lot of ideas we look at.

Qualified Charitable Distributions (QCDs) Your distributions from your retirementplans are reported on your 1099-R form , but the form doesnt specify how much went to a QCD. NOLs from tax years ending after 2020 can only be carried forwardand carryforwards are limited to 80% of taxable income in any one tax period.

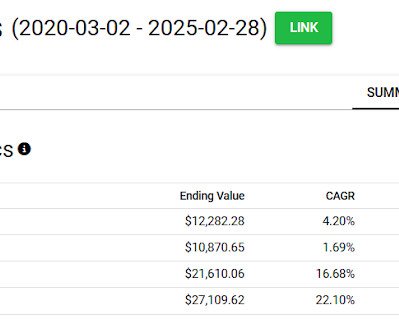

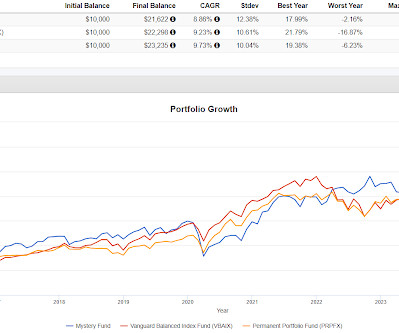

In 2020 and 2023 the fund was unchanged versus up a lot for the other two. To be clear though, the Mystery Fund is not intended to be a single portfolio solution. The year by year tells a slightly different story in case it isn't apparent from the chart.

Looking at how it has actually traded though, yes more volatility and you can see in the chart it got pasted in the 2020 Pandemic Crash (poor first responder?) Maybe not rigorous study, but if you shorten the time frame of any of the above to start after MDCEX fell 36% in the 2020 Pandemic Crash, the Kurtosis comes way down.

MCW also did great in 2021, 2020 and 2019. For the last couple of years, I think a lot of people gravitated to just using market cap weighted in their accounts, that seems like it has been the conversation and for 2023 and 2024 the returns for MCW have been great. Occasionally of course, MCW gets pasted.

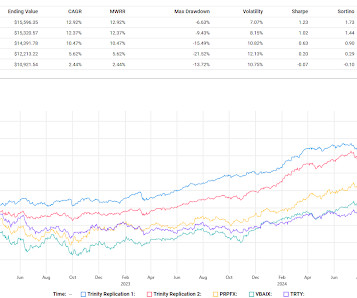

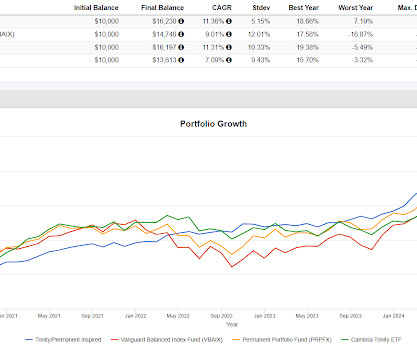

The full term backtest of Trinity/Permanent Inspired is compelling of course but it trailed VBAIX and PRPFX in 2020, 2021 and 2023. I built out the following, allocating 25% to each holding and compared to VBAIX, PRPFX and TRTY. In 2024 it was slightly behind PRPFX and slightly ahead of VBAIX.

It might be debatable whether we've gone through a full cycle from the start of 2020 but it certainly has been a full five and a half years. Clearly, no attempt at resilience can be infallible but I do think being reliable most of the time is possible.

When we do these exercises, I'm not really trying to find something that will compound miles ahead of plain vanilla, the objective is more about smoothing out the ride and trying to build a portfolio that will have a robust result in the face of a market event like in 2022 or maybe even a fast decline like the 2020 Pandemic Crash.

Two of the three strategies have traded sideways in the 2020's. I said I was interested enough to start following it, having no idea what to expect. This chart from the paper doesn't paint a rosy picture.

In the 2020 Pandemic Crash, PUTW went down in lockstep with the S&P 500 but in 2022 it was only down 10% versus 18%. With less dramatic declines, ISPY usually holds up better than the index. WDTE sells put options. I'm not sure about WDTE specifically but PUTW which also sells puts has had mixed results with going down less.

Recall last week , we were discussing thinking about the impact of retiring Baby Boomers on the equity markets and of rising rates on housing. The demographic question touches on a big issue: $6 trillion dollars in 650,000 (401k) retirementplans held by 10s of millions of Americans.

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. But when they get market timing wrong, they lose subscribers. I sure as hell don’t want to either.

After a significant drop in March of 2020 in the wake of the pandemic, the S&P 500 has staged an amazing recovery. The index finished 2020 with a gain in excess of 18%. As someone saving for retirement , what should you do now? Approaching retirement and want another opinion on where you stand? Review and rebalance

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content