This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

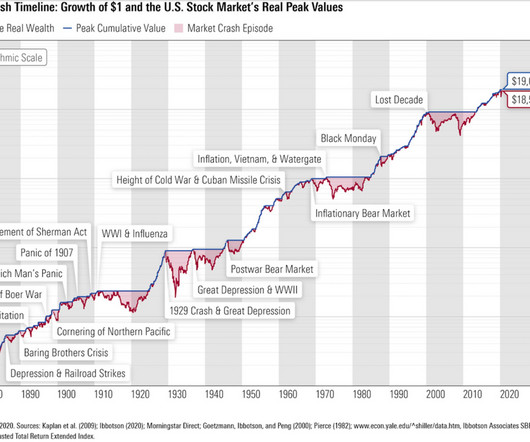

Chart above is from March 2009, but that’s cheating) Compare this to the average 15-year return periods over the past century, which generated ~8.7%. In October 2009, I called the move off the lows The Most Hated Rally in Wall Street History. Financial Repression was the rallying cry for underperforming managers.

Investors looking for a diversified portfolio that performs well in all market conditions have long been drawn to the All Weather Portfolio, a strategy pioneered by Ray Dalio of Bridgewater Associates. The portfolio allocates across U.S. equities, gold, commodities, and long-duration and intermediate-term Treasury bonds.

Their focus is on generating alpha with high conviction concentrated portfolios. As you, as you may recall, the insurance companies had huge commercial loan portfolios in those days that they were using to backstop long dated life insurance liabilities. 00:14:50 [Speaker Changed] Yeah, it was about the middle of 2009.

So far, this year hasn’t seen a full-blown crisis like 2008–2009 or 2020, but the ride has been very bumpy. Investing involves risks including possible loss of principal. No investment strategy or riskmanagement technique can guarantee return or eliminate risk in all market environments.

We are currently experiencing one of the most volatile times in decades, on top of the start of the pandemic and the 2008-2009 recession. Setting a strategic asset allocation and stress testing it, as part of the riskmanagement exercise, is a critical component in “pre-experiencing” such downturns. Retirement plan sponsors.

Though inflation remains the most significant perceived risk for business owners, more than two-thirds expect a recession before the end of 2023. And of those expecting a recession, the majority believe it will be as bad or worse than the Great Recession of 2007-2009. It’s important to remember that most recessions in the U.S.

One of the few movies which portray the 2008 financial market crisis in the most accurate way possible, this thrilling movie’s inciting incident begins when a risk-management division head is laid off due to the company’s downsizing. Rather than investing in a single product, your portfolio should be diversified.

Northern Arc Capital IPO – About the Company The company was founded in 2009. Fund Management includes managing debt funds and providing portfoliomanagement services. It uses data-driven riskmanagement and credit underwriting processes. Keep reading to learn about the company.

And my answer was, “Hey, not everybody wants to buy a passive index around the satellite of a core portfolio or even just, hey, I have an idea, I think this is going to change the world.” BERRUGA: So many of our clients were struggling to find alternative sources of income for their portfolios. Is that who the Global X investor is?

The transcript from this week’s, MiB: Antti Ilmanen, Co-Head, Portfolio Solutions, AQR , is below. BARRY RITHOLTZ; HOST; MASTERS IN BUSINESS: This week on the podcast, I have an extra special guest, Antti Ilmanen is AQR’s Co-head of the Portfolio Solutions Group. CO-HEAD, AQR’S PORTFOLIO SOLUTIONS GROUP: Thanks, Barry.

The company primarily focuses on individual retail housing loans, with a significant portion of its portfolio consisting of low-risk salaried customers. in 2009 to 12.3% Diverse product portfolio: The company offers a range of mortgage products. Effective riskmanagement: The company maintains low GNPA and NNPA ratios.

That’s a really easy portfolio to create. It allows you to understand, generally speaking, what is a reasonable beta for that whole portfolio. The other thing it allows you to do is to benchmark your ability to select managers that outperform both in each areas and across the sleeve. That allows you to do two things.

And it restarted in, I wanna say March of 2009, but like onlya little bit. It was derivatives math, it was like working with the traders on like riskmanagement. And if you’re thinking about your portfolio systemically, like that creates different incentives for you and for your portfolio company’s managers.

Focus on Risks and Opportunities: Our ESG research approach seeks to assess ESG riskmanagement, and identify sustainable opportunities that address key environmental and/or social challenges, which we believe can lead to improved performance and impact. Our approach is consistent and systematic across our platform.

Our sustainable investing philosophy and process were developed in-house and are supported by a robust team of ESG research analysts, portfoliomanagers and other dedicated professionals. Our approach is consistent and systematic across our platform.

Focus on Risks and Opportunities: Our ESG research approach seeks to assess ESG riskmanagement, and identify sustainable opportunities that address key environmental and/or social challenges, which we believe can lead to improved performance and impact. Our approach is consistent and systematic across our platform.

Focus on Risks and Opportunities: Our ESG research approach seeks to assess ESG riskmanagement, and identify sustainable opportunities that address key environmental and/or social challenges, which we believe can lead to improved performance and impact. Our approach is consistent and systematic across our platform.

And Wall Street didn’t work out for a variety of reasons, but I ended up working sort of an adjacent industry in the portfoliomanagement software business, and really wasn’t where my passion was. They’ll construct the portfolio. They have a riskmanagement technology. RAMPULLA: Yeah.

And we’ve talked about whether we go deeper on existing strategies, we build new businesses, we find somebody who can help him more as almost a co-CIO with riskmanagement, with the investment process. Back in 2009 or maybe it was ’10, if you remember, hedge funds were largely short Lululemon.

So a very different dynamic than we saw back in 2007, 2008, 2009. So obviously, riskmanagers, you know, and CROs were very focused on how do we manage that risk and diversify that credit risk that they were taking on in mid-market companies. Yes, there’s a lot of liquidity in private equity.

And the third, the one that nobody talks about is riskmanagement. Riskmanagement. And so that’s not just, we talk about riskmanagement in terms of buying at a big discount to intrinsic value and then that gives you that capital sort of buffer. That’s a long time. It’s a long time.

And it not only has the advantages of there being inefficiencies, so there’s the potential to generate alpha, but if you do it right, it’s pretty non-correlated with probably the rest of your portfolio. So with no further ado, my interview with Gramercy Funds Management’s Robert Koenigsberger. That’s it.

Not, not terribly busy in 2007 to be honest, but in 2008, 2009, 10, it was by far the busiest time in my career in investing. So, so let’s talk about some of those legacy portfolio issues. We see this because we are a pub, we own a, we manage a publicly traded b d C and so do a lot of our peers.

The DJIA closed 1999 at 11,497 and 2009 at 10,428. At the GFC bottom, March 9, 2009, the Dow traded at 6,547. ” Harry Markowitz won the Nobel Prize for exploring the mathematical tradeoff between risk and return. Some years ago, The Wall Street Journal asked him how, given his work, he structured his own portfolio.

And what we figured out in 2009, really when we started buying homes is that we made the bet that it, I mean, it wasn’t a very exotic bet, but we made the bet that the subprime mortgage market wasn’t coming back at all. And so, so starting in 2009, we, we, there was no flip market.

BROWDER: I just gone the riskmanagement committee. The currency devalued by 75 percent and my portfolio, which was above $1 billion, went down 90 percent. And this had an unbelievably positive affect on the value of my portfolio. Things got worse and worse and on November 16th, 2009, Sergei went into critical condition.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content