This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Would you like to diversify but also defer paying big capital gains taxes? I’m Barry Ritholtz and on today’s edition of at the money we’re going to discuss how to manage concentrated equity positions with an eye towards diversification and managing big capital gains taxes. And that’s the broad market.

I took a lot of math classes. I couldn’t give up math in computer science. And then I moved to San Francisco after business school and was again, quite focused on the private equity space Right before 2009, I felt I was ready to do something else. So I moved to Zurich in 2009 and I left Bain in 2017. at Wellesley.

He’s got a fascinating background at both Bank America, Merrill Lynch, and since 2009 at BGI and BlackRock. It’s sort of like math with dollar signs attached to it. So how did you find your way over to BlackRock in 2009? He helps to oversee over a trillion dollars in bond ETFs. I really like it. I really enjoyed it.

But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. And then on top of that, of course we ran straight into the 2008, 2009 great recession. So what do you discuss with your wife and kids about taxes?

And then the next step up seems to be full on wealth management, where you’re dealing with philanthropy, generational wealth transfer, a lot of bells and whistles including estate planning tax. 00:31:40 [Speaker Changed] So there’s the emotions and then there’s the math, right? 00:26:17 [Speaker Changed] Absolutely.

Obviously math, there’s a ton of symbolic logic wherever you look, that classic syllogism, right? We have the financial crisis, and you decide to launch Rich Bernstein Advisors in 2009. Although we get great tax and cost benefits with ETFs, how much of this is just simply comes down to human behavior and human nature.

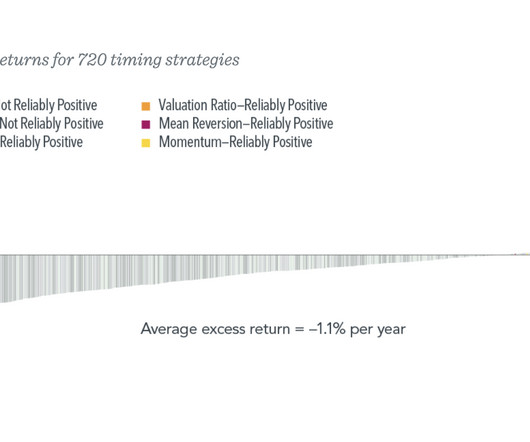

Dates like the lows in 1982, 2009, and 2020 show up this time, which always catches our attention. Early 1987, March 2009, August 2011 (after the US debt downgrade), and the COVID lows in March 2020. The math is just Earnings * (Price / Earnings) = Price, since the Earnings parts cancel.

The US population today is 341,814,420; in 2009 it was 308,512,035. Economy in 2022 was $25,439.70B; in 2009, it was $14,478.06B; ignore that also? from 2009, and by 2024 you get (wait for it) $193.44T. Do we simply ignore the growth in the size of the economy and the U.S. population? Do we just ignore that?

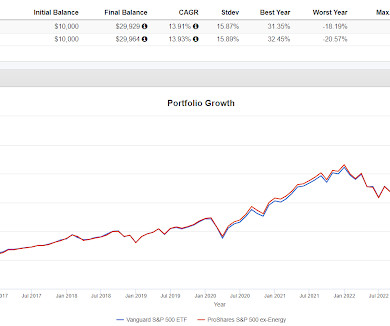

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. The dotcom top, the double bottom in Oct 02-March 03; the highs in 2007, the lows 2009. Let’s add some color to the discussion on timing itself and add a little nuance.1

If you dig even deeper, you may also think about tax implications, including the alternative minimum tax and qualified holding periods. But the basics of equity compensation and tax aside, theres something else you might want to be mindful of something that is a bit more difficult to define or quantify.

You wouldn’t be surprised to learn the tax consequences of owning a mutual fund is a part of it. I’d say management consulting is any of the other thing that least at that time was the other career trajectory, just my personality, more of a math oriented introvert. Really fascinating guy. So I was at Harvard.

I published what’s called a comment, so like a very short one about this great tax law case with this guy who like won the lottery and then wanted to get his lottery winnings treated as capital gains. So like a component of it was like the standard derivatives math, right? Matt Levine : 00:03:44 You know, I did. And he lost.

You have the liquidity, the tax efficiency, the transparency. And I did the math, and I think at that point in time, roughly speaking, assets in ETS were roughly just 10 percent, 12 percent of assets in mutual funds and I was pretty convinced that that number was to increase significantly. Wait, markets go down? RITHOLTZ: Wow.

Betterment is great at reducing any taxes you have to pay on your investments, and they work with you to give you the best financial advice through their algorithms. Since Kickstarter’s launch in 2009, 18 million people have backed projects. Below is a rundown of a few of the leading robo-advisor platforms.

So for a taxable investor, hedge funds generally aren’t tax efficient. And when you look at the assets that are invested, the three trillion in hedge funds, I would guess that north of 90% of that are in institutions that don’t pay taxes. It’s part of their own tax planning. RITHOLTZ: Right.

And I think that has been true since 2009 until now. SETHI: When I show people for example that if you take a mortgage, you might as well just add on 50 percent to that mortgage to account for taxes, interest, maintenance, opportunity costs they are shocked they can’t believe it. It’s much deeper than math.

ANAT ADMATI, PROFESSOR OF FIANCE AND ECONOMICS, STANFORD GRADUATE SCHOOL OF BUSINESS: So, my journey starts where I took a lot of math. I was good in math and I love the math. So, I was kind of, in my romantic mind when I was in my early 20s, I was going to take but not give back to math, that kind of thing.

I am guessing they chose that timeframe to coincide with the March 2009 bottom. We've talked just a couple of times about the market becoming increasingly concentrated which just in terms of math means that a diversified strategy will lag for as long as the big names do well.

So I, I did a math degree at Oxford, which is more pure math. You know, pure math can be very theoretical and detached from the real world, and it’s getting worse. You don’t have to pay any tax and just let the rest ride. It’s just math stick to it over long periods of time. You give out 5%.

I’m good at math and science and you know, I always had an idea what go into business, but I felt that electrical engineering would be a good foundation. You know, I, it always, I I see different numbers all the time, so it’s always kinda like, who’s math if you will? He had been a tax lawyer.

And what we figured out in 2009, really when we started buying homes is that we made the bet that it, I mean, it wasn’t a very exotic bet, but we made the bet that the subprime mortgage market wasn’t coming back at all. And so, so starting in 2009, we, we, there was no flip market. And this is proprietary data.

Unfortunately for these people, the minimum wage has not increased since 2009, nor, to state the obvious, has it kept up with inflation. They'll cite the fact that companies are going to buy back $1 trillion in stock this year, due to the excess cash provided by the tax cuts. million people are “near-minimum-wage” workers.

So, I did the math, 20 million times a hundred. So, let me just repeat the math. And so, again, I went through this simple math. And they said as a result of them earning zero, the $230 million of taxes that was paid in the previous year is paid in error and we’d like that money back. It is $2 billion on the ship.

My mom was a math teacher so — RITHOLTZ: Okay. Some famous periods of reversals in market, the most famous spring of 2009 when we came off the GFC. You can argue they’re — RITHOLTZ: A more tax efficient than that? ASNESS: More tax efficient dividend. He’s the genius in math. RITHOLTZ: Yeah.

And I said, I’ll go get a master’s and things will be better in 2009, because these are one year programs. Burger King Tim Hortons, I remember very clearly because it was in the middle of those waves of kind of tax dodgy, those inversion deals. And that’s sort of the math. RITHOLTZ: Right. RITHOLTZ: Right.

Jeffrey Sherman : Well, what it was was, so I, as I said, with applications, there’s many applications of math, and the usually obvious one is physics. Barry Ritholtz : It seems that some people are math people and some people are not. The, the math came easier. And I really hated physics, really. It’s so true.

And I, and I really like the application of math and statistics and computer science to markets. And so graduating right into 2009, right out of the financial crisis, I said, I don’t think I’m gonna get a job. You learn the math that can help you with, with market making operations. And I just caught the bug.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content