This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To find out more, I speak with Jeremy Schwartz, Global Chief Investment Officer of WisdomTree, leading the firm’s investment strategy team in the construction of equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Present value of future cash flows, any asset is present value of future cash flows.

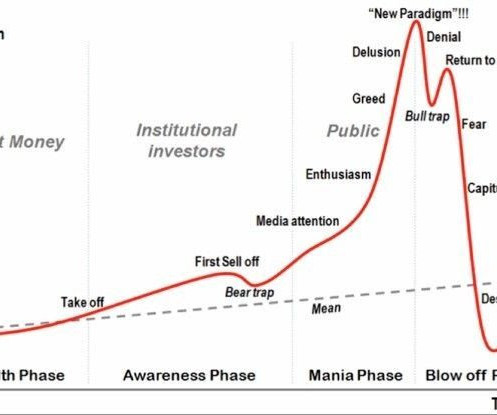

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

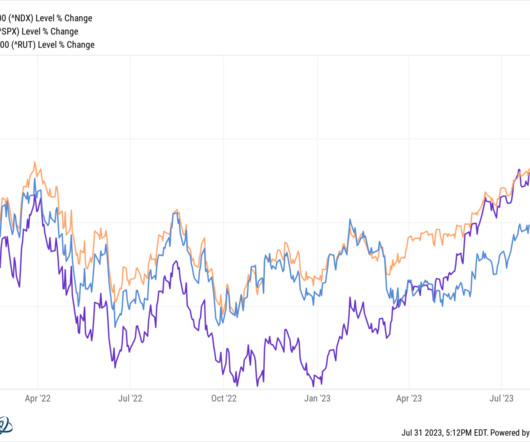

but the giveback off the highs was substantial: S&P 500 was down ~23%, Russell 2000 was off 27%, and the Nasdaq 100 came down 32%. But we won’t know how big a losing trade it might be until early 2024, when we see the updated valuations. Investors hold asset classes, to benefit from long-term value creation and compounding.

In this post, we break down the most important differences between SPY and QQQ across key dimensions: performance, volatility, valuation, sector exposure, factor makeup, and fees. Using Portfolio Visualizer data from 2000 to May 2025, QQQ outperformed SPY slightly with a 7.77% annualized return vs. 7.52%. Standard Deviation 15.3%

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

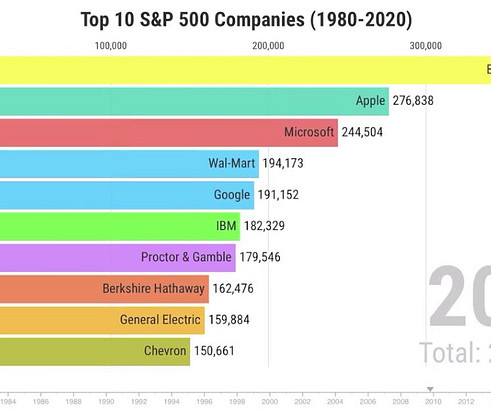

Four of 1990’s top ten were still there in 2000. IBM topped the list in 1980 and 1990, but was off it entirely by 2000. Also off the list for 2000: Philip Morris (still profitable due to international markets, but tobacco was more and more a social pariah in the U.S.), Only Microsoft remained from the 2000 list.

After lagging the S&P 500 for much of 2024, the Russell 2000 small cap index has staged an impressive rally in recent weeks. As smaller companies catch up to their large cap counterparts, investors may be wondering which Russell 2000 stocks look most attractive. over 10 years Manageable debt levels Projected 10-year return of 16.8%

Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. But investors may still want to consider layering in various other asset classes to help protect from this unexpected risk in the future. With future stock returns higher than they were at the start of the year and the U.S

The basic concept is when one of these asset classes starts a long move, they tend to go much further and much longer than people typically expect, and you want to capture as much of that move as possible. So different time horizons, different assets. What assets are they in? I don’t know if all our listeners are.

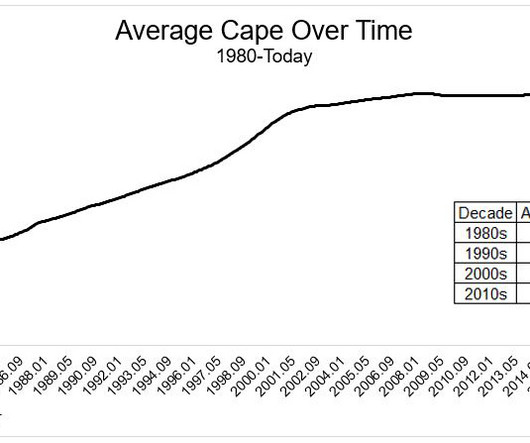

No matter what metric you looked at, the peak valuations for growth stocks in mid-2021 were extreme. This is a chart of the valuation of the most expensive decile of our investable universe using the Price/Sales ratio. But even after that decline, the overall valuation remains about 30% above its average for the full period.

. ~~~ About Jeremy Schwartz: Jeremy Schwartz is Global Chief Investment Officer of WisdomTree, leading the firm’s investment strategy team in the construction of equity Indexes, quantitative active strategies, and multi-asset Model Portfolios. Barry Ritholtz : So we’ve talked about 66-82, 2000-2013, equities did poorly.

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. But valuations strongly favor value over growth. The S&P 600 small cap index has returned about 1.5%

CIO Perspectives Webinar, 2022 Asset Allocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe.

CIO Perspectives Webinar, 2022 Asset Allocation Outlook. Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. CIO Perspectives Webinar, 2022 Asset Allocation Outlook . Inflection Points: 2022 Asset Allocation Perspectives and Outlook Report.

A client said – I understand market valuations are expensive but it doesn’t seem that it will correct much. The fundamental driver of market peaks and exorbitant valuations is the perception that there is nothing to worry about – there is no investment risk. Certainly not if you are sticking to your asset allocation.

The Russell 2000® Index (which tracks small-cap stock performance) was up only 0.44%. Are the Russell 2000’s weak returns a sign of slowing economic growth, or is the recent underperformance of small caps reflecting investor sentiment about current market opportunities? times earnings over the same period.

So it’s, 00:09:11 [Speaker Changed] You’ve become an enterprise, it’s 10 x what it once was in terms of headcount, it’s much bigger in terms of assets. Then what enables that you have to have some asset ability capability that competitors can’t equally duplicate. In 2000, right. Are you prudent?

He began with a single restaurant, a single cookie store, and eventually parlayed that into a series of acquisitions, mergers, expansions, ultimately leading to the Panera Bread concept, which now has 2000 locations and does about six and a half billion dollars. He sold the company in 2017 or so for about seven and a half billion dollars.

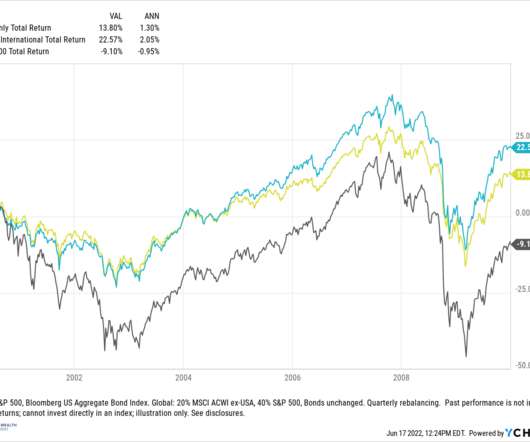

assets the cold shoulder. stocks that started in the early 2000s. Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% equities to an asset allocation. From 2000 to the end of 2009, the global allocation would have outperformed by nearly 8.8% Valuations. Source: J.P.

So, so you’ve held analyst roles and a number of asset managers. And so I had a lot of contacts in Australia at that point, and one of them was the CEO of what was at the time called Colonial First State Global Asset Management. But there’s always gotta be some element of the valuation really being compelling.

When he began, PE was a little bit of a niche boutique sort of investment, and over the ensuing 25 years, it has grown to be really a major asset class with giant opportunities that have been expressed by then small, now very large companies, of which Blackstone is one of the largest. It is an institutionalized asset class.

Investors may find opportunities at more reasonable valuations when comparing different asset classes across the market. For example, small caps have lagged the NASDAQ 100 this year, with the Russell 2000® Index of small-cap stocks down nearly 10% year.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. Some might argue that the Fed’s policy could trigger another crisis as asset prices become overly inflated.

In his latest piece, Waiting For The Last Dance , he writes: "I believe this event will be recorded as one of the great bubbles of financial history, right along with the South Sea bubble, 1929, and 2000." tech in 2000, and more or less everything in 2007. stocks are based on traditional valuation metrics, via Michael Cembalest.

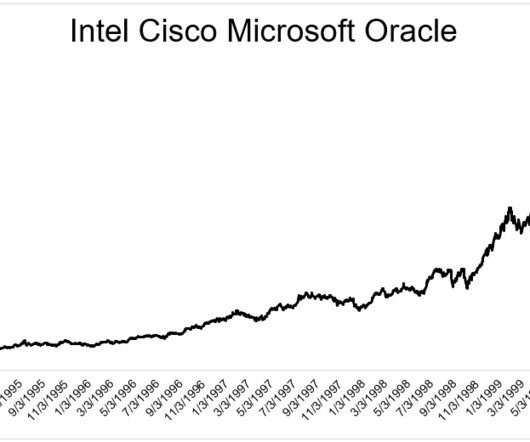

From 1995 until the peak in March 2000, these four added $1.768 trillion in market cap. The combined four companies were trading at 100x earnings and 26x sales by early 2000. There were plenty of people warning about valuations during the late 90s. Unlike the late 90s, you can justify the valuations.

Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of asset allocation— the single biggest driver of long-term gains. Reassess asset allocation. Now that allocation has fallen to about 12%, with the remainder in more volatile assets.

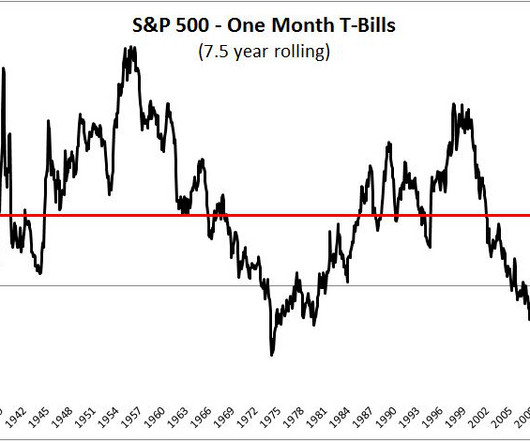

This range is determined by a number of factors, including but not limited to the business cycle, valuations, interest rates, inflation, and the collective mood of millions of investors. Since the top in March 2000, the S&P 500 has outperformed risk-free assets by just 2.7% a year, the largest spread over a 7.5

The problem is the level of valuations. Popular investment sectors or themes gain momentum as more investors join, driving prices much higher than the worth of the underlying assets. Because it has been a popular narrative for quite some time. But, what’s the problem with investing in popular narratives?

And so we’ve grown from a very small company with 29 partners back in 1979 to, as you noted, over a trillion dollars of assets and it become very diversified. So fixed income is now a substantial percentage of our assets. For, for hedge fund or for, 00:06:29 [Speaker Changed] So that was actually Montgomery Asset Management.

Ratios like the PE ratio and price/book can be more popular among investors, but both have significant drawbacks, especially in a world driven by companies with high intangible assets. Free cash flow (FCF) represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets.

1999, 2000, the internet was blowing up. The SNL crisis Tiger Chase had started, you know, in the wake of the internet melding down in 2000. I I was speaking at the Javits Center, 2000 people in the audience. If you think back to 2000, Amazon was the disruptor to Walmart or to Macy’s. And that was 25 years ago.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. While no two downturns are the same, we believe this approach can again be effective in the current period.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. While no two downturns are the same, we believe this approach can again be effective in the current period.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Risks in Bonds.

The discussion dissects technology sector valuations, what rising rates could mean for markets and the most important investment trends in the decade ahead. The group also shares their thoughts on the role unconventional assets like gold and Bitcoin can play in client portfolios. Learn more >.

Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e.,

Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e., Less Efficient Asset Classes.

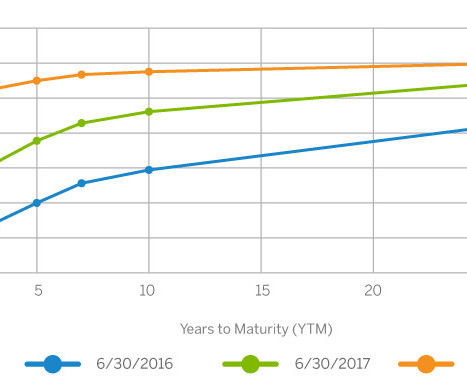

The LPL Research Strategic and Tactical Asset Allocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. While we acknowledge that interest rates could move higher still, we think the risk/reward profile of adding to rate-sensitive fixed income assets has improved.

billion Attractive dividend yield of 4.27% The stock also performs well (93%) on the P/E Growth Investor model, indicating a favorable balance between its valuation and growth prospects. Key strengths include: Large market capitalization of $295.7 billion Strong cash flow per share of $19.74 Substantial trailing 12-month sales of $194.7

.: Grantham, who is well-known for identifying bubbles before they burst such as the dot-com bust in 2000 and the housing market crash in 2008, has been outspoken about his belief that the market was in a “super bubble” that has yet to truly burst. Valuations are still high, despite rampant inflation and an economic slowdown.

Ratios like the PE ratio and price/book can be more popular among investors, but both have significant drawbacks, especially in a world driven by companies with high intangible assets. Free cash flow represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets.

While new highs were set before bear markets in 1987, 2000, 2007, and 2020 in recent memory, the market has also made spectacular gains following new highs. According to quarterly Federal Reserve data, money market assets were more than $6 trillion at the end of the third quarter of 2023, roughly double what they averaged from 2011 to 2017.

A Moment of Zen: The Wisdom of Staying Invested achen Wed, 07/19/2017 - 15:28 When discussing the merits of cash as an investment, Warren Buffett doesn’t pull his punches, saying that those who hold cash or its equivalents “have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.”

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content