This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

"How much can I spend in retirement?" Advisors want to help clients set a secure, reliable retirementplan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree. Ideally, retirement spending would align perfectly with a client's needs – neither too much nor too little.

For many financial advisors, a core part of the retirementplanning process involves simulating whether the client's assets will last through retirement. That emotional connection supports confidence and increases the likelihood that the client will stick with their plan and stay committed through both good markets and bad.

Many financial advisory clients might work for 40 years or more, ideally seeing their income – and capacity to save for retirement – increase over time as they advance in their careers. Still others, including adherents of the Financial Independence Retire Early (FIRE) movement, may hope to retire even sooner.

Also in industry news this week: Why the announced acquisition of RIA custodian TradePMR by retail brokerage firm Robinhood could prove to be a boon for RIAs on TradePMR's platform, who could receive a wave of referrals from Robinhood's massive base of next-generation retail clients How Morningstar is cutting the "Medalist Ratings" of thousands of (..)

Also in industry news this week: A recent survey indicates that younger "DIY" investors are more likely to be interested in working with a human advisor than their older counterparts, suggesting an opportunity for advisors to tap into this demographic (perhaps by setting minimum planning fees that ensure these clients can be served profitably today (..)

The report suggests this might be due in part to increased RIA valuations and the assumption of some firm founders that next-generation employees won't be financially able to buy out the firm from them, though additional data indicates that many firms don't have career paths in place that could help next-generation advisors envision their path to firm (..)

That means if your retirementplan underestimates medical costs, you risk serious shortfalls. For instance, a retired government employee receiving a fixed monthly pension of ₹40,000 ten years ago might find its value significantly reduced today if inflation averaged around 6% annually. on June 6, 2025 , and cut CRR by 100 bps.

citywire.com) The latest in advisor fintech news including saturation in the portfolio management tech space. kitces.com) Estate planning Estate plans are a big lift for everyone, including advisers themselves. kindnessfp.com) Why clients need to organize their digital assets for estate planning purposes.

Podcasts Peter Lazaroff talks with Christine Benz about the most overlooked parts of a retirementplan. awealthofcommonsense.com) Things you can do while your portfolio is down. peterlazaroff.com) Steve Chen talks all things Social Security with Devin Carroll, author of "Social Security Basics." tonyisola.com) Stress is natural.

Many of us are covered by one or more types of defined contribution retirementplans, such as a 401(k), 403(b), 457, or any of a number of other plans. What many of these plans have in common is that they are referred to as Cash Or Deferred Arrangements (CODA), as designated by the IRS. How, you might ask?

barrons.com) Don't let bad energy ruin your portfolio. tonyisola.com) Aging 10 steps to prepare financially for retirement, including 'Design a retirement paycheck.' theretirementmanifesto.com) How to think about retirementplanning even though it may be decades off. blairbellecurve.com) Learning is unlearning.

Retirementplanning is a journey that generally takes decades to complete and most of us start out along the do-it-yourself path. More than likely, your first step was to enroll in an employer-provided plan such as a 401(k) or setting up an individual retirement account, also known as an IRA.

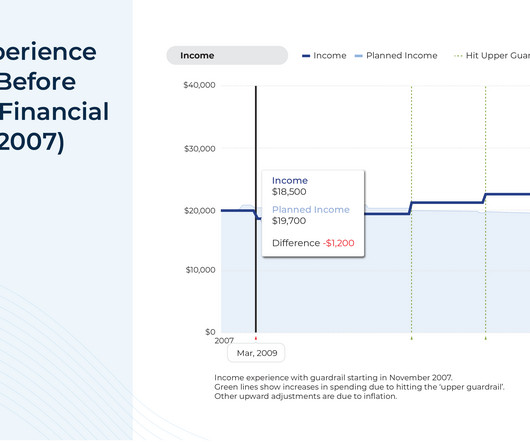

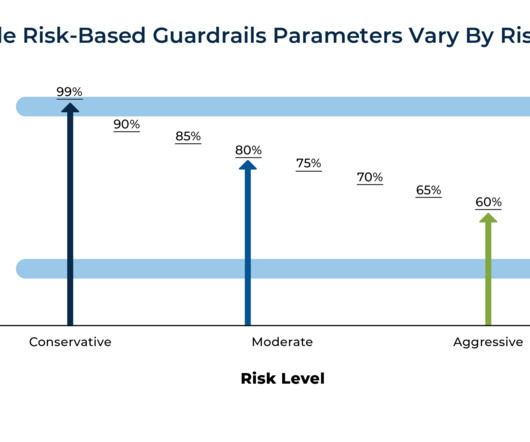

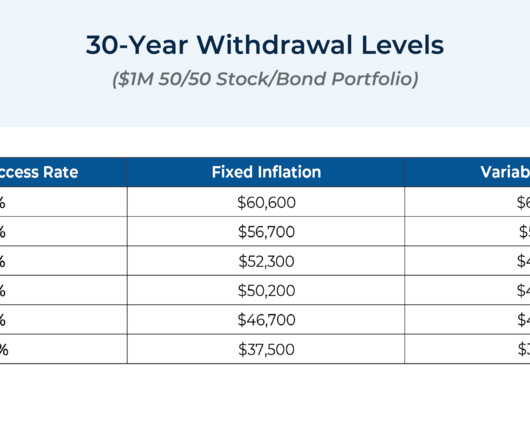

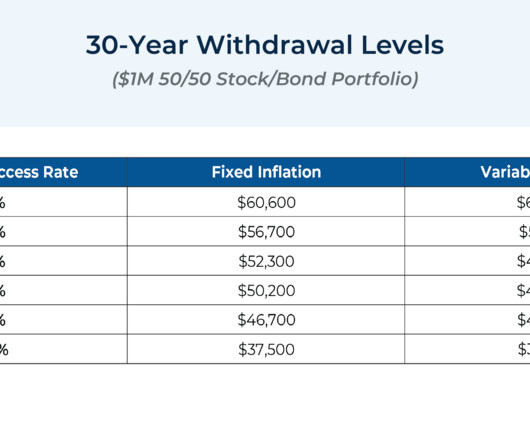

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirementplanning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

Imagine yourself on your last ride home from work on the day you retire. It probably depends on whether you have a strong plan in place for income during your retirement years. Having a retirementplanning checklist can help make this final commute the time of reflection and joy it should be.

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M.

ritholtz.com) Steve Chen talks with Robert Brokamp about retirementplanning and purpose. newretirement.com) Retirement Don't let too risky a portfolio ruin your retirement. bestinterest.blog) Private equity is not the solution to retirement shortfalls.

a ski chalet), assessing whether it will lead to greater overall wellbeing, or, alternatively, more stress, is more challenging Enjoy the 'light' reading! a ski chalet), assessing whether it will lead to greater overall wellbeing, or, alternatively, more stress, is more challenging Enjoy the 'light' reading!

At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations. This guide consolidates what we’ve learned to help you refine, update, or pressure-test your current retirement and estate strategy with confidence.

million Americans turning 65 in 2024, advisors are navigating four core risks that will impact their portfolios in retirement: longevity, inflation, volatility, and emotions. With nearly 4.5 We will discuss new research by Dr. Wade Pfau, professor at The American College of Financial Services.

(morningstar.com) Dan Haylett talks with Eric Brotman, who is the founder and CEO of BFG Financial Advisors, about retirement as 'graduation.' humansvsretirement.com) Estate planning Why you should update your estate plans periodically. obliviousinvestor.com) Estate planning should most importantly include talking about it.

morningstar.com) Christine Benz and Jeff Ptak talk with Mike Moran, managing director and pension strategist for Goldman Sachs ($GS) about the state of retirement preparedness. nytimes.com) Retirement Some alternatives to a fixed retirement withdrawal rates. thinkadvisor.com) What makes up the three-legged stool of retirement.

youtube.com) Retirement Why planning in retirement is so challenging. Rowe Price about non-financial considerations in retirement. morningstar.com) People work in retirement for any number of reasons. humansvsretirement.com) 3% rates make holding a mortgage in retirement easier. In fact, it's a distraction.

Enjoy the current installment of "Weekend Reading For Financial Planners"– this week's edition kicks off with the news that a recent analysis from Morningstar suggests that the Department of Labor's (DoL's) new Retirement Security Rule (aka Fiduciary Rule 2.0)

Also in industry news this week: The SEC this week announced a proposed rule that would require RIAs to collect and verify their clients' personal information in an effort to prevent illicit activity, though many firms likely are taking many of these steps already Why larger RIAs and those that have been acquired tend to have worse client and staff (..)

From there, we have several articles on retirementplanning: Why an individual’s portfolio of relationships could be just as important as their investment portfolio when it comes to happiness in retirement.

Also in industry news this week: Concerned about the (insufficient) frequency of its examinations of RIAs, an SEC committee has recommended that the regulator allow third parties to conduct these examinations and to request Congressional authorization to charge investment advisers under its purview a ‘user fee’ that would provide steady (..)

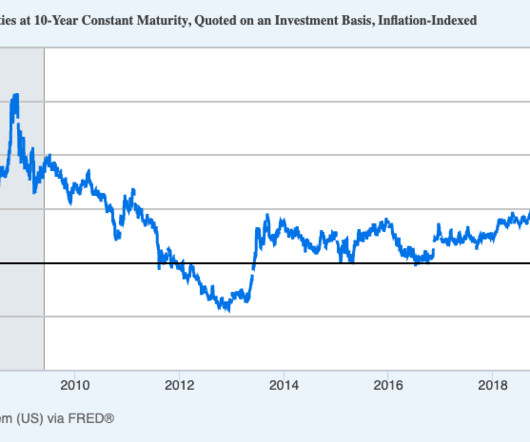

From there, we have several articles on retirementplanning: The latest rules for 2023 Required Minimum Distributions from inherited retirement accounts. Why relying on Treasury Inflation-Protected Securities (TIPS) to support the bulk of retirement income needs could be risky.

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

Also in industry news this week: The SEC settled its first charges related to its new marketing rule with a firm that advertised 2,700% annual returns A survey suggests that older Americans prefer the term "longevity" to "aging", perhaps informing the way advisors discuss related issues with their clients From there, we have several articles on retirement (..)

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. Start planning early. And the best way to do that?

Also in industry news this week: While the number of RIA M&A deals has not surged in 2024, the average size of deals has increased, demonstrating interest from (often private-equity-backed) firms in pursuing larger targets Off-channel communication tops the list of concerns amongst RIA compliance professionals, with advertising and marketing coming (..)

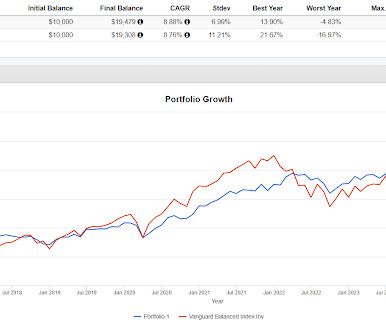

A fun rabbit hole over the years has been the 75/50 portfolio devised by John Serrapere which he wrote about several times at the old IndexUniverse site. For anyone new, the big idea is for the portfolio to capture 75% of the upside with only 50% of the downside. Portfolio 2 has a normal, even if not heavy, allocation to equities.

I wanted to have a little more fun with portfolio construction comprised of ETFs that " no one should use." Below, leverages up the Permanent Portfolio. Portfolio 1 just levers up the stocks, gold and bonds. Portfolios 1 and 2 lagged VBAIX over the backtested period but were quite a ways ahead of the PRPFX mutual fund.

Also in industry news this week: A recent survey suggests that advisors who best understand their prospects' and clients' unique needs and communicate their value and fees clearly could be best positioned to win and retain clients Why a dearth of advisor talent could spur additional M&A activity and 'poaching', and what firms can do to attract (..)

Also in industry news this week: While an infusion of Private Equity (PE) capital has shaken up the RIA M&A market, the ultimate implications for advisors, their clients, and the PE firms themselves remain unclear A recent study has found that a significant portion of 'DIY' investors are open to working with a human advisor (and paying for the (..)

Retirement sets in motion a new life—one that promises freedom from day-to-day grind but also requires prudent planning of finances. Thankfully, India provides a range of safe and sound passive income alternatives designed exclusively for retired citizens. Linked to the market and thus involve some degree of risk.

The post Investing for Retirement: Strategies for Long-Term Success appeared first on Yardley Wealth Management, LLC. Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. What lifestyle do you envision?

You're 81 and been taking income from your portfolio for 15 years, what matters to you more, that you can continue to take what you need from your portfolio or that four year run in your mid-50's when you beat (or lagged) the market? If you're 81 and can no longer meet your income need from your portfolio, that is what matters.

The portfolio on the left was up a little in 2012 but lagged VBAIX, on the right, that year by almost 400 basis points. If we extrapolate Portfolio 1 out over the next 20 years and there were to be a similar result, that would be great but there would be quite a few years where Portfolio 1 got completely dusted.

Early on in my savings journey I prioritized tax-deferred retirement accounts over all else. The set-it-and-forget-it nature of a workplace retirementplan is one of my favorite features. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account.

As owners of financial planning firms approach retirement, some may decide to sell to an external buyer, while others may plan for an internal succession. Sometimes, this succession plan can include the owner's child, providing an opportunity to keep the business in the family.

While the downgrade has made headlines and might be startling to advisory clients (particularly those with significant portfolio allocations to U.S. government's creditworthiness from an AAA rating to AA+.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content