This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

That’s where everyday costs—like housing and transport are rising, squeezing retirees. That means if your retirementplan underestimates medical costs, you risk serious shortfalls. over that period. If you planned to live on ₹1 lakh per month today, you might need ₹1.5 – ₹1.7 50,00,000.00 10 7% 50,00,000.00

Freelancing is liberating, but without a solid financial plan, it can also be unpredictable. As a freelancer, you juggle not only your craft but also your finances, taxes, and retirementplanning. That’s where financial planning for freelancers comes in. Plan for taxes ahead of time 4. Plan for retirement 5.

Retirement marks a significant transition in life, especially after nearly three decades of military service. For our family, my husbands upcoming retirement after 29 years in the military was not just about financial planning for the futureit was also about making his long-held dream a reality. One of his biggest goals?

Floor plans, regular updates to your documentation, and a clear boundary between personal and business space help establish the legitimacy of your home office deduction. Vehicle and transportation expense deductions Vehicle expenses often represent one of the most significant opportunities for tax savings for small businesses.

The basic no spend month rules Spend only on essentials : Rent/mortgage, food, insurance, transportation, and bills are allowed. Follow your existing budget : Stick to your pre-planned necessities and nothing extra. Look ahead and stay motivated Saving money for the future isn’t just about retirement.

Infrastructure includes communications, data centers, utilities, satellites, transportation and energy pipelines. Tyler Rosenlicht, a senior vice president at Cohen & Steers, said infrastructure and natural resources were two examples that illustrate where active management can add value.

This article will explore how to navigate complex tax situations arising from multiple income sources, examining various income types, reporting requirements, self-employment obligations, and strategic approaches to record-keeping and tax planning that can help protect your financial interests.

The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one. Strategic tax planning serves both to keep companies on the right side of IRS regulations and to preserve necessary capital during those precarious early stages when the startup is most vulnerable.

On the whole, its advisable to consult a tax adviso r to develop a dependable tax plan. Business-related travel: Costs associated with traveling for business purposes, including transportation, lodging, and meals (subject to limitations). Do Freelancers Need to Pay Quarterly Estimated Taxes?

Josh also had an anecdote about shipping companies, the kind that transport oil and the like and have crazy high yields. This won't matter of course to IRA accounts and the effective tax rate on dividends can be very low depending on having a low earned income but with a low enough income, long term capital gains can be taxed at 0%.

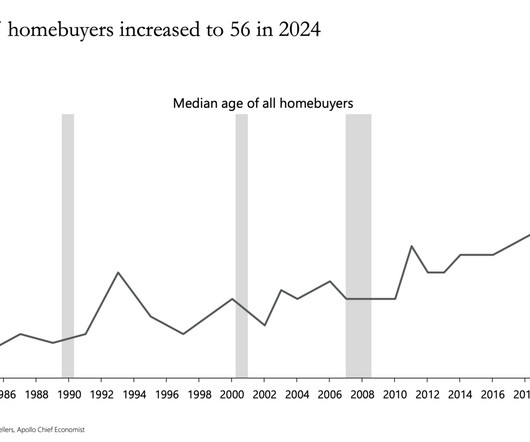

00:39:24 [Speaker Changed] Another quote from the book, why should investors care about the day-to- day or even month to month fluctuations in prices if they have no plans to sell anytime soon? And then the second question is, when do you plan to sell your securities? And most people say, well, what do you mean when do I plan to sell?

Home office space deductions Business equipment deductions Travel expense deductions Vehicle mileage deductions Business meal deductions License fee deductions Health insurance deductions Retirement contribution deductions How do I claim home office tax deductions? Contribution limits vary depending on the type of plan.

The post Strategic RetirementPlanning Guide for Single Women: Expert Financial Advice appeared first on Yardley Wealth Management, LLC. Without a partner to rely on for financial support, single women must take proactive steps to ensure a secure and comfortable retirement.

WA was the career plan, always economics and finance. How do we make sure that there are enough retirement savings for our population? It was not our plan. But that being said, it is still the case that if there is uncertainty, that does obviously have implications for business planning, for household planning.

What, what was the original plan Stephanie Kelton : To be a dentist. And then at some point when you get to energy, you know, then all bets are off because it’s transportation, it’s fertilizer which gets food, which gets, and then it’s just, you know, we, we sort of lived that before in the seventies.

Just as the rise of modern air transportation allowed highly contagious diseases to spread across the globe in days, the rise of social media allows highly contagious ideas to infect financial markets.( If we think of bitcoin investing as a virus, this virus can evolve, mutating and spreading to susceptible minds.

Let’s figure out that with this article, where we break down the real expenses across rent, food, transport, healthcare, and lifestyle to see how far a family can live a comfortable life, or are they just able to merely survive with a monthly income of ₹2 lakhs.

Lynn O'Shaughnessy , Columnist: College Planning June 12, 2025 4 Min Read 12875116/iStock/Getty Images Plus When I took on this task years ago, it was challenging to figure out the itinerary for a 12-day trip that included nine private liberal arts colleges in Massachusetts, New York and Pennsylvania.

We speak daily with clients who are contemplating where they might live in retirement. Now is the time to explore various retirement housing options and strategies for aging individuals. From aging in place to retirement communities, consider your individual preferences and needs when choosing the most suitable housing option.

marketwatch.com) Why Christine Benz wrote "How to Retire: 20 Lessons for a Happy, Successful, and Wealthy Retirement." spectator.co.uk) Financial potholes High housing and transportation can blow a hole in your finances. awealthofcommonsense.com) Seven steps to an estate plan including 'Take stock of your assets.'

In an earlier post, I summarized many of the housing options people can consider in retirement. This post takes a deeper dive into CCRCs (Continuing Care Retirement Communities also known as Life Plan Communities) CCRCs are an all-in-one solution to aging in place for people over 60. You can check out the article here.

Retirement is an exciting milestone—a time to leave behind the hustle and bustle of work and embrace a new chapter filled with more freedom and opportunities to enjoy life. Planning well in advance ensures that your retirement years will be financially secure, fulfilling, and less stressful than your working years.

Lawmakers are trying to restrict these investment choices in workplace retirementplans, but big fund managers are trying to give shareholders a voice. ( There is a real possibility that China will soon be uninvestable to outsiders. ( A Wealth of Common Sense ) • On Wall St., Socially Responsible’ Is Common Sense.

Writing can be a great hobby to pick up in retirement. It is the sensory details that will help transport you into the world of the story. Click HERE to sign up for a complimentary review of your retirementplan with us at Integrity Financial Planning to take one step closer to achieving the enriching lifestyle you deserve.

Navigating the journey to retirement can often feel like a complex puzzle, especially when it comes to figuring out how much you need to save. The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years.

Allocating retirementplanning I introduce asset allocation with clients by dividing retirement life into two parts: basic life and high-quality life. Basic life is daily expenses, like food, clothing, housing and transportation. These basic things must be planned with a certain income.

Category: Client Relations Financial planning is difficult for anyone, and even more so for someone who is a special needs person or has such a family member. Other than the benefits provided by the federal government, there are various plans and relief programs in place that are provincial or territorial based.

Here’s how it works: 50% for essentials : Allocate 50% of your income to essential expenses such as rent, utilities, groceries, transportation, and minimum debt payments. This includes contributions to your emergency fund, retirement accounts, and paying off any outstanding debts beyond the minimum payments.

Key Takeaways: The 4% rule is a general retirement guideline suggesting that retirees can safely withdraw funds equal to 4 percent of their savings during the first year of retirement and then adjust for inflation each subsequent year for 30+ years. It has pitfalls which must be considered. What is the 4% “rule”? We’ve all heard of it.

Key Takeaways: Choosing a city in which to retire won’t be a one-size-fits all approach; there are many factors for your clients to consider such as cost of living, climate, taxes, access to healthcare, cultural amenities, and social opportunities.

The cinematic spectacle is immaculately produced—the sets, costumes, and dialogue are eloquently crafted in concert to transport you back in time. Retirement is about living the retirement you dream of and finally achieving financial independence. Watching each episode places you right in a ’60s Madison Avenue office!

According to the data from the US Census Bureau , 50% of women aged 55-66 have no personal retirement savings. So, how much should you save before you retire? Can you retire with 500k, or do you need more? Keep reading to find out if it’s possible to retire with 500k — and how to do it. The good news? Cost of living.

RetirementPlanning How to Calculate How Much You Need to Retire Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. While many financial experts discuss specific percentages people should aim for to have a fulfilling retirement, the ultimate retirement income formula does not exist. Will you move?

Preparing for retirement is a significant life transition that demands a clear understanding of your financial situation. This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age.

That’s why this is not a plan for better budgeting in the long-term. You can use a budget planning notebook or an app if you prefer. Fortunately, learning about budget meal planning can go a long way in helping you stick to a tight food budget so you can avoid waste. Sound restrictive? It definitely is.

Everything else Using percentages for your budget categories Expert tip: It’s ok if your budget categories change How do you plan your budget categories if you are focused on paying off debt? This group of categories includes: Retirement account contributions e.g. 401k/403b/IRA Non-retirement investing (e.g. Essentials 3.

If you’ve attempted to make a budget in the past and “failed” due to budget challenges , maybe it’s time to rethink your plan. If you’d like an even more streamlined budget plan, you could check out the 80/20 budget and apply it to your budget instead.) With this budget, you plan to save 20% of your total income. That’s it. (If

Freelancing is liberating, but without a solid financial plan, it can also be unpredictable. As a freelancer, you juggle not only your craft but also your finances, taxes, and retirementplanning. That’s where financial planning for freelancers comes in. Plan for taxes ahead of time 4. Plan for retirement 5.

The beneficiary may only make this contribution if they are not participating in any employer sponsored retirementplan. The current tax law also allows for a rollover from a 529 plan to an ABLE account up to the annual limit amount. Qualified Disability Expenses : ABLE accounts provide flexibility in how the funds can be used.

RETIREMENT 6 Steps to Effectively Prepare for Pre-Retirement Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. As you get closer to retirement age, you may be inclined to wait until you relinquish some responsibilities at your company before planning. Determine Your Retirement Income and Expenses .

It is important to note that while $25 is not a high hourly rate, it is still possible to live on this salary with careful budgeting and financial planning. In your budget, you should plan to set aside money to cover future expenses, such as a vacation, a house downpayment, retirement , etc.

What comes to mind when thinking about retirement? By understanding the inner workings of retirement income, you can enjoy retirement without worrying about finances. The starting point is understanding your retirement needs and how you’ll pay for them. The last thing you should do is worry about your finances.

A budget plans out exactly how you'll use your money and this can be tailored to suit your specific lifestyle and situation. In its simplest form, the 50-30-20 budget rule divides your after-tax income into three distinct buckets, which are: 50% to needs 30% to wants 20% to savings This plan keeps your finances simple and also easy to follow.

The numbers in the 60/30/10 each represent a percentage of your financial plan. With this system, you will use 60% of your take-home pay to build your savings or even an early retirement account , invest, save up for a down payment, or repay debt. As an example, one of my major savings goals is retirement.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content