This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

(youtube.com) Christine Benz and Amy Arnott talk with Peter Mallouk, President and CEO of Creative Planning, about the 'messy' business of financial advice. morningstar.com) Thomas Kopelman and Jacob Turner talk with Ankur Nagpal about tax considerations when selling a business. obliviousinvestor.com)

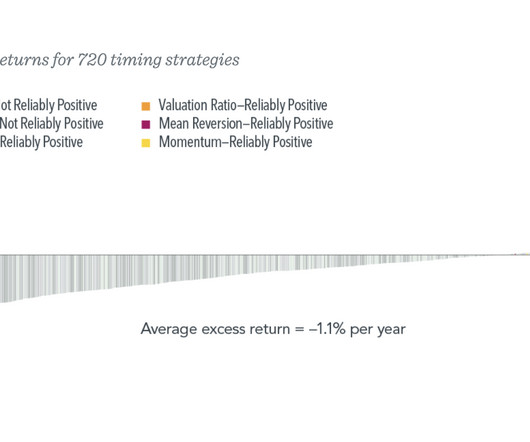

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. When you get it wrong, it crushes your retirementplans. Let’s add some color to the discussion on timing itself and add a little nuance.1 By Jeff Sommer New York Times, Nov.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well.

This article will explore how to navigate complex tax situations arising from multiple income sources, examining various income types, reporting requirements, self-employment obligations, and strategic approaches to record-keeping and taxplanning that can help protect your financial interests. What is an RSU?

To show you what’s possible and what’s necessary, if early retirement is something you want to pursue seriously. Even if you don’t plan to retire unusually early, starting your retirementplanning now can dramatically improve your options later. What’s the earliest you can retire? Retiring at 55?

. $6300 in today's dollars goes a long way for us, that's quite a bit more than our fixed monthly expenses but might be about equal to regular monthly expenses plus once or twice a year type expenses like property tax, home owners insurance and so on. What's the risk to Social Security income?

First, is the math right based on my numbers? They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. If we guess just 2 billion people, and that is just a guess, and divide that into the 15.2 How can it solve anyone's problem?

A couple making $100,000 has an effective tax rate per Gemini of just under 8%, then less another $7500+/- for the employee share of Social Security puts them at about $85,000. Hopefully they're saving a little bit, call it 10% or $10,000 and their net is $75,000 (a little more than that for the tax not owed on their 401k contributions).

If you retired at 62 and lived to 92, you’d have to cover three decades. A million dollars breaks down into an annual amount of about $30,000 over 30 years (not counting taxes, etc.). Let’s look at a few 401(k) planning basics to get you started. 1. If your employer has a 401(k) program, they probably have a matching plan.

It's been a while since this sort of thing was relevant for my day job so something could have changed, weeklies didn't exist for example, but if my math is correct then it was way over exposed which would account for last week's decline in the fund price. Please leave a comment if I did the work incorrectly.

There was an article on LinkedIn (via Abnormal Returns) by Victor Haghani that dug into the math working against leveraged ETFs. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

However, if the goal is to pay off a mortgage before retirement to spend would-be mortgage payments on other things during retirement, the math may not work out. For one, any savings from retiring home debt is a one-time savings (the interest expense). After-tax cost of borrowing and hurdle rates.

One advisor noted that these events draw not only current clients but also curious prospects who are actively exploring retirementplanning options. Tax Strategy Workshops Workshops like “Creating Tax Efficient Retirement Strategies” attract attendees who are serious about their financial future.

Do the math, it would be a fantastic long term result but very difficult to pull off. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Maybe the model providers don't really want their models to differentiate.

Part of the equation is that he is convinced that tax rates have to go up to pay for out debt and so converting to a Roth now before tax rates do go up will result in people ending up with more after tax dollars versus just going the RMD route at what is now 73 on its way to 75. This has been his thing for a long time.

James and Pamela’s Big Dream Excerpt from The Smart Person’s Guide to Financial Planning & Investments: A Simple and Straightforward Approach to Understanding Your Personal Finances By Michael J. Their retirementplan is strong, their kids are independent, and they are debt-free. So—problem solved, right? Well, actually, no.

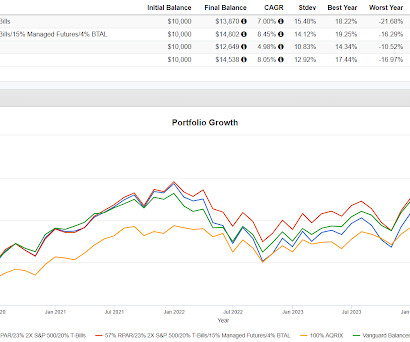

The way Portfolios 1 and 2 are weighted, the math works for being a 60/40 portfolio and then from there we add portable alpha/capital efficiency/return stacking. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Taking volatility out of a fixed income portfolio is fairly simple.

Simple math, it looks like the carry index has compounded at less than 3%. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. This next chart from Bloomberg compares just the carry component of the FOXY fund to the S&P 500 and T-Bills.

A harsh reality is that $50,000 is not a retirement fund but it is a pretty robust emergency fund. We've gone over the math before that starting as late as 55 can catch a lot of the way up if they can afford to save a very high percentage of their income. Smart Asset calculates $70,000 gross income working out to $57,187 after tax.

The article devoted a good amount of space to bond market math, focusing on the pain of owning the iShares 20+ Year Treasury ETF (TLT) and bond funds in general. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

These items for us include things like propane delivery (we could pay monthly), property tax and so on. Simple math is that this person needs to save $23/yr to come up with that additional $350,000. But simple math tells you that adding $5000/yr likely won't cut it. BTW, I mean that literally, it is all on a spreadsheet.

Calculation Breakdown Let’s break down the math to find out how much you could earn annually with a $30 hourly wage: Consider an average workweek of 40 hours and an average year consisting of 52 weeks. Keep in mind that this calculation represents the gross annual salary, not accounting for taxes, insurance, 401K, or deductions.

The course covers an introduction to personal finance, credit cards, life insurance, health insurance, investment instruments, loans, income tax and planning, budgeting and building a strong portfolio. Also, you will learn how to plan your taxes, credit score importance and how to budget your income to create a portfolio.

Generally they all plan to work to 70 or beyond out of necessity. There was an odd and I believe inaccurate emphasis on workplace retirementplans pivoting from defined benefit plans (pensions) to defined contribution plans (401k) starting around the turn of the century. That is Rooster. Rooster loves duck toys.

Figure out how much money you make in after-tax income. More accurately, 70% of your take-home pay, or net income after taxes, not pre-tax income. Once you know your weekly or monthly income, you can do the simple math of calculating how much 70% would be. Time is one of the most powerful tools in retirement savings.

In the case of real estate a 2.29% weighting and for "private equity" companies it's about 17 basis points (looked at XLF holdings and then did a little math), that's just not going to move the needle. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

The webinar talked about the future of model portfolios transitioning from a combo of ETFs for passive and mutual funds for active to include more direct indexing to allow for "tax optimization." So using simple math, the total return is 34% versus 72% for the common. Based on an initial price for NVDY of $20, the $4.53

Generally speaking, pensions are less viable than they used to be, the math doesn't work as well. About 40 years ago employers started to pivot away from pensions to 401k, they started to pivot away from defined benefit plans to defined contribution plans. So that's quite a bit to chew on even if it isn't a new idea.

Despite the leveraged semiconductor ETFs, when blended with USMV, the portfolio is underweight technology versus the S&P 500 using simple math, it works out to about 26% versus closer to 40% for the S&P 500. Consider the following two portfolios.

If it is going to happen, it won't be for ten years +/-, plenty of time to factor that into your math. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. There is simply no way that a cut in Social Security payouts should catch anyone off guard.

As a financial advisor or other investment professional, you’re no doubt already well aware that the “math” side of the conversation is a large part of what your clients need help with every day. RetirementPlanning. Retirementplanning is a very precise process, and one that is unique to the individual.

The math is only off by a shade using leverage via UST and a little bit of SSO, remember RPAR is leveraged. I find this to be interesting but anyone needing normal stock market growth in order for their retirementplan to work, probably isn't going to get it from any of these portfolios.

Part of the math that determines options premiums is the risk free rate of return from T-bills. Building a plan based on assuming an 11% payout forever is really going to hurt this guy if that is what he is saying. Covered call funds have many favorable attributes. Keeping up with the broad stock market is not one of them.

Paid Time Off for Hourly Employees Earning $35 per Hour How Much Is $35 An Hour After Taxes? It doesn’t include deductions like taxes, insurance, 401K contributions, etc. This is the gross amount before any taxes and deductions are applied. Remember : These figures represent gross income before taxes and deductions.

A 20% drop in managed futures that is leveraged to a 40% weight would have added another 800 basis points to the decline (simple math). They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. In 2008, VBAIX was down 23%.

The way the math works out, 4% has a success rate in the low 90's based on simulations and has never failed looking backward. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

They charge $495 per month for on-going investment management, retirementplanning and financial advice as-needed. If you have a large concentrated position that it takes a ton of time to unwind in a tax-aware manner If you have are an executive with stock options that come with complicated terms, etc. Firstmetric.

Invest In the Stock Market, Passively Effort Level: 1 Upfront time commitment: Upfront money commitment: Passive income probability: Investing in public stocks and bonds is the main way people build long-term wealth and passive income through their retirementplans or brokerage accounts. It could save you thousands in the long run!

It has to be such a different set, the retirementplanning is different, the safety net is different. You have the liquidity, the tax efficiency, the transparency. So a phenomenal learning experience with both Jefferies and Morgan Stanley. RITHOLTZ: So you move here from Spain. What is the financial advice world like in Europe?

Few vehicles offer this kind of triple tax advantage. Strategically control your MAGI Your Modified Adjusted Gross Income (MAGI) plays a much bigger role in retirement healthcare costs than most people realize. Tax-loss harvesting: Strategically selling investments at a loss can offset capital gains and reduce your MAGI.

After you’ve done this math, you might be wondering if you have “enough,” and certainly that’s hard to assess when there are so many unknowns. Understand Your Tax Situation It’s easy to forget about managing taxes in retirement, but the old adage applies: It’s not what you make, it’s what you keep.

The less reliant a retirementplan is on an investment portfolio, the less need there is for flexibility. I say that because the math in most simulations and with several IRL clients, is they die with a lot of money leftover. Counting on an inheritance might be risky but a little bit of planning in case you get one makes sense.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content