This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

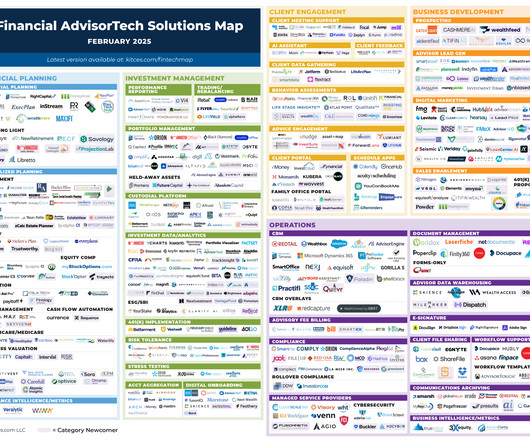

Welcome to the February 2025 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

The post Tax Strategies for High-Income Earners 2025 appeared first on Yardley Wealth Management, LLC. Tax Strategies for High-Income Earners in 2025. In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations.

Tax season can be overwhelming, but understanding how to leverage deductions and credits can significantly impact your bottom line. While both mechanisms help reduce what you owe, they operate in fundamentally different ways that affect your final tax bill. And tax law is not static. of your AGI. of your AGI.

represents our current state of healthcare, in which genetic makeup and the environment play a major role in illness and disease, and where the focus of doctors lies primarily on the administration of treatments to cure and mitigate human ailments; and Medicine 3.0 In the context of the financial planning industry, whereas Financial Advice 1.0

Tax deductions can save you thousands annually by reducing your taxable income through legitimate business expenses. Understanding these deductions is more critical than ever as tax laws evolve, presenting new opportunities for savings. Understanding this distinction is crucial for maximizing your tax benefits effectively.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. Life happens. You buy a business.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . Tax-Planning Possibilities.

A financial advisor can help with maximizing your retirement income through taxplanning After retirement, your income sources may become limited to pensions, Social Security benefits, and investment income. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income.

The rise of remote work and digital nomadism has made FEIE a common tax minimization strategy for Americans living abroad. What is the Foreign Tax Credit (FTC)? Financial and lifestyle considerations of living abroad The importance of professional tax advice for expats FAQs about the FEIE What is the Foreign Earned Income Exclusion?

Key Takeaways: The Harness Marketplace allows your tax firm to be paired with high-value tax clients whose unique needs align with your expertise. The Harness Marketplace attracts employees, founders, and investors in tech, healthcare, management consulting, and other high-earning industries who need help managing complex tax needs.

While these can be avoided, there is another cash outflow that can considerably lower your savings and returns and is also hard to avoid – tax. Taxplanning is essential. Tax is charged on every penny you earn. Tax evasion is a crime, and missing tax payments can lead to legal hassles that can be hard to get out of.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools.

A bridge plan for health insurance (since Medicare only begins at 65). And a tax-efficient withdrawal strategy that won’t sabotage your nest egg early. Retiring is easy with planning, and retiring early is also doable. Healthcare costs can be brutal This is one of the most overlooked challenges of early retirement.

Filing taxes in Hawaii requires a clear understanding of the specific forms and procedures unique to the state. Unlike federal tax forms, Hawaii tax forms are tailored to meet the state’s tax laws and regulations, ensuring residents and non-residents alike comply with local requirements.

Retirement planning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

Zoe’s Tell-All: 2023 Tax Season Published February 14th, 2023 Reading Time: 5 minutes Written by: The Zoe Team If you’re a golfer, you know a lot goes into the brilliant game. Similarly, filing taxes includes many steps and details everyone needs to know about. Taxplanning can be overwhelming , but it doesn’t have to be.

It doesn’t factor in your healthcare coverage situation, it isn’t designed to avoid the 3 strikes of taxplanning , and it doesn’t account for the location and liquidity of your wealth and savings. However, the 4% Rule may be used as a conversation starter with your financial advisor on how to turn your savings into income.

According to the Fidelity Retiree Health Care Cost Estimate, the financial burden of healthcare in retirement is substantial. As a couple aged 65 in 2023, you may need approximately $315,000 saved (after tax) to cover your healthcare expenses. The absence of a dedicated healthcare fund can lead to unexpected financial hardships.

As a company founder, early startup employee, or small business owner, you may find yourself in a higher tax bracket as your business grows or you realize gains from equity compensation. But that doesn’t mean you simply have to accept a higher tax bill. Here are 20 tax-efficient actions to consider when filing your taxes in 2024.

Reduce Tax Payments. Taxes are inevitable, but the amount you pay each year doesn’t have to be. There are several actions you can take to avoid higher tax rates and retain more money, including: . Distributing tax-smart assets into the different tax categories (taxable, tax-deferred, and tax-free) to limit liability .

Financial Planning Needs: Retirement planning Education and family planning Obtaining appropriate insurance coverage Business and taxplanning Significant asset purchases Strategies for Serving Clients in This Stage: Clients at this stage are experiencing life events — both large and small — that will impact their financial planning needs.

They help you optimize taxplanningTaxplanning is an important aspect of financial planning that can significantly impact your long-term wealth accumulation. It helps you strategically minimize the amount you pay in taxes and maximize your investment returns to preserve more of your hard-earned money.

While it may seem like a luxury that is only available to the wealthy, anyone is capable of building an effective financial plan and putting it into action. Without effective personal financial management, you risk losing money to poor budgeting, poor taxplanning, or even just to inflation.

Planning for retirement is one of the biggest financial challenges you will ever face, and a financial advisor can help you adopt a strategy that can take you to your goals, mitigate risk, and adapt to the changes that will inevitably come your way. Retirement planning can be a long-term journey, and a lot can change along the way.

Contributions to your 401(k) are pre-tax, meaning that for every dollar you contribute, you actively lower your taxable income. If you’re covered by a workplace retirement plan, you likely won’t be eligible to make deductible (pre-tax) contributions to your traditional IRA, but investing in it still provides valuable benefits in retirement.

By helping you lower your tax The impact of proper taxplanning on your eventual retirement balance cannot be overstated. Engaging with a skilled financial advisor can empower you to manage your taxes proactively. HSAs allow you to make contributions on a pre-tax basis, allowing for tax-free growth of earnings.

Pain Points: These are issues like market ups and downs, tax problems, and money planning being hard. Explain how to manage your retirement funds and pay for healthcare. TaxPlanning: Help clients learn smart tax strategies. Discuss estate planning and how financial decisions can impact taxes.

Other pay : Certain employees can be eligible for “pay in lieu of redeployment” (9 weeks) and an “additional separation bonus” (8 weeks) It’s important to note that severance payouts are taxed as ordinary income in the year of payout. Taxplanning for a transition out of Intel is critical.

If you dig even deeper, you may also think about tax implications, including the alternative minimum tax and qualified holding periods. But the basics of equity compensation and tax aside, theres something else you might want to be mindful of something that is a bit more difficult to define or quantify. or Europe).

At that point, you likely have a clearer understanding of what it takes to maintain your current standard of living, and that can be the starting point for your retirement planning. Although retirement may come with a lot of changes that include downsizing, travel, additional healthcare needs, etc.,

It is important to have a clear understanding of your budget post-retirement, factoring in housing costs, property taxes, and maintenance expenses. It is also essential to consider factors like climate, proximity to family, friends, and healthcare facilities. Different states have different rules when it comes to income taxes.

It can require a deep understanding of personal finance, investment strategies, tax implications, and more. A financial advisor can help you understand the intricacies of financial planning for physicians. Not creating a comprehensive financial plan Financial planning for physicians and healthcare professionals is essential.

Step 2: See if the financial advisor conducts an annual tax review Ensuring that your financial advisor reviews your tax return annually is a crucial step in maximizing your financial benefits. An effective financial advisor should be proactive in reviewing your taxplan before the year-end.

For instance, the level of education you get, the quality of healthcare you can afford, and the lifestyle you can adopt all depend on your wealth. A 401k account is a tax-advantaged account that will help you save tax and, at the same time, build wealth for the future. Do not undermine tax. can help you with taxplanning.

Furthermore, ChatGPT may have limitations in reflecting recent policy changes or potential mathematical fallacies that can impact retirement and taxplanning strategies. This blog explores the strengths and limitations of employing ChatGPT vs. a financial advisor when planning for retirement.

So for a taxable investor, hedge funds generally aren’t tax efficient. And when you look at the assets that are invested, the three trillion in hedge funds, I would guess that north of 90% of that are in institutions that don’t pay taxes. It’s part of their own taxplanning. I like Buffett’s idea.

Investment planning also plays a crucial role in tax optimization, enabling you to minimize tax liabilities and maximize after-tax returns. Additionally, tax-loss harvesting, and other tax-optimization strategies can further improve the tax efficiency of your investment portfolio, thereby enhancing overall returns.

Not only was the stock market fairly volatile, but there were also atypical tax regulation changes. Tax-loss harvesting. Paying taxes on investment gains can be a financial burden, but tax loss harvesting can reduce your bill. You can claim as much capital loss as your realized capital gain plus $3,000.

So there’s the, “Hey, I’ll work with you and we’ll develop goals and a plan how to get there.” They’ll do taxplanning, right? We’ll do estate planning and other complex financial planning. Let’s talk a little bit about portfolio analytics, financial planning tools.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content