This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The two most common pricing models are fee-onlyfinancial planners (flat-fee or fixed-fee advisors) and AUM-based financial advisors (who charge a percentage of assets under management). While AUM advisors may seem appealing, they often come with high lifetime fees and potential conflicts of interest.

Traditionally, investment planning has been at the forefront of how financial advisors add value for their clients. But, with the rise of index funds and the commoditization of investment advice, generating sufficient investment ‘alpha’ to justify a fee has become more challenging for advisors.

A part of this process might include hiring a financial advisor or hiring a new financial advisor if you have decided to move on from your current advisor. Here are six questions to ask when choosing a financial advisor: How do you get paid? Hiring the right advisor for your needs is critical. What can you do for me?

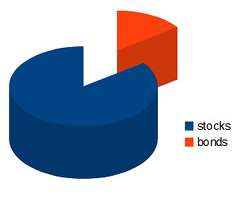

This might have been their own doing or the result of poor financial advice. This is the time to review your portfolio allocation and rebalance if needed. For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. Click To Tweet.

We have a great deal of participation in high ticket size products like Portfolio Management Services (PMS) & Alternative Investment Funds (AIF). Mis-selling would be at its peak during such times, only a certified professional can act on client first approach to help choose investors what is right for them.

When I started Vincere Wealth as a fee-only practice, the vision was to become the go-to place for Millennials who need help with their money. Along the way, I’ve gathered six key insights about financialplanning for Millennials. However, sometimes it gets to be too much when it comes to financial topics.

Active investing involves a hands-on approach to managing your portfolio. If you are a skilled investor and well-versed in market fluctuations, you may be able to capitalize on quick opportunities, or sell off a security before your portfolio takes a hit. It also means that when the market is down, your portfolio may be down with it.

However, these disturbances tend to be short-lived, and well-balanced portfolios can typically weather them just fine. About Your Richest Life At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-onlyfinancialplanning. We are at a unique point in U.S.

Many people have managed their own investment portfolios and have seen great results. But there is another group of investors who swear by their financial advisors. They credit their financial stability and success to their guidance. The only costs you pay are related to the actual investments you choose and nothing else.

Schedule monthly check-ins for your portfolio and more frequent check-ins for your bills and accounts to make sure youre not caught off guard by any shifts. Having a plan can cut down on your stress, and allow you to feel more in control of your finances. There are plenty of apps that can help you track your accounts and spending, too.

The best way forward is to keep an eye on your long-term plans, and try not to get derailed by uncertainty. 2025 may prove to be a bumpy ride, but a strong, well-balanced portfolio is designed to weather storms. The post 2025 Q1 Update: Federal Reserve Rates, Inflation and Financial Markets appeared first on Your Richest Life.

As the move to transparency in financialplanning takes hold, regulations are changing in Colorado and other states. Here’s the triumph of virtue that financialplanning transparency will (FINALLY) bring to planners across the country and the benefits to clients that come along with it. What should financial advisors do?

This is where diversifying your investment portfolio comes into play. Diversifying your investment portfolio is a vital strategy for managing risk, optimizing returns, and achieving your financial goals. However, diversifying your investment portfolio can help reduce your overall investment risk.

Welcome to the 371st episode of the Financial Advisor Success Podcast ! David is the Co-Founder and CEO of Element Pointe Family Office, a Fee-Only RIA based in Miami, Florida that oversees almost $1.6 My guest on today's podcast is David Savir. billion in assets under advisement for 50 client households.

The post Is FinancialPlanning a Pandemic Necessity? Is FinancialPlanning a Pandemic Necessity? FinancialPlanning magazine just released their annual tech survey and a corresponding article: Tech Survey 2020: Advisors losing faith in planning software. By Michael Garry Yardley Wealth Management .

I talk about some of those options in my “How to Adjust Your FinancialPlan” post. Remember that it’s perfectly normal for there to be ups and downs in the markets and the economy, and you’re likely going to see those fluctuations reflected in your own portfolio. . About Your Richest Life.

Just like with your portfolio, banking diversification helps to keep your money safe if something goes awry at one of your banks, and lets you maximize the benefits of each of those institutions. For more information on the services offered, contact Katie today.

How Conflicts of Interest Shape Financial Advice: A Conversation with Mike Garry and Amy Patterson Conflicts of interest in financial advice can greatly impact the recommendations that clients receive, especially from fee-only advisors. Today, many advisors have moved to a fee-only model.

Knowing the types of financial advisors and their compensation models can empower you to select a professional whose approach aligns seamlessly with your financial goals, risk tolerance, and overall budget. Below are the different types of financial advisors you can choose from based on their fee model: 1.

At the end of 2021, I “retired” after 33 years in the investment management industry, the last nearly 22 of them at Eaton Vance in Boston, where I served as a global equity portfolio manager and Director of Equity Strategy Implementation.

In the 10 years I’ve spent running a financialplanning firm, I’ve learned a lot about how people handle (or don’t handle) their finances. That’s why we typically prefer passive investing , with a balance of low portfolio expenses, minimal trading costs and tax efficiency. Money lesson #5: Be open to change.

The primary fee structures are: Fee-only : Advisors only receive payment from their clients for the services they provide, not receiving any commissions or other incentives from product providers. Fee-based : This structure is a blend of fees and commissions. Hourly FeeFee charged per hour of advice.

The 1 percent fee structure refers to the annual advisory fee charged by a financial advisor, typically calculated as a percentage of the Assets Under Advisory (AUA). This fee structure is common in the financial advisory industry and varies based on the size of the client’s portfolio.

A financial advisor is a certified financial planner who is licensed and regulated to take mandate decisions on multiple aspects of financialplanning. Financial planners plan and manage your portfolio in a way that saves your time. Financialplanning is a service that is often hard to define.

Big, broad dreams and more specific, immediate goals are both instrumental in figuring out the best way forward with your portfolio. Or, if you plan to buy a house within the year and your down payment is sitting in the stock market, you might run the risk of losing that money in a down market before you buy.

It can feel disheartening to check on your portfolio and see poor returns, but don’t panic; we’ll cover why it’s better to weather the turbulent times to get the long-term rewards. What does that mean for your portfolio? That’s why it’s so important to have a well-balanced portfolio. Stocks Weather Down Economies.

We’re going to talk about how he provides high value as an hourly financial advisor by saving investors from the “Humpty Dumpty portfolio” and the lessons other advisors can learn about serving clients with simplicity, transparency, and integrity, whether they choose to adopt the hourly fee model or not.

But many physicians are too busy to give their investments the time and attention they need, and their portfolios end up falling by the wayside. About Your Richest Life At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-onlyfinancialplanning.

Two weeks prior, I had a question from a client about how his investment portfolio had performed compared recently to the Dow Jones Industrial Average or “The Dow.” . We look at long-term expectations for various stock and bond returns and build portfolios around those for our clients. So here goes …. That’s in Bucks County).

My client’s estate planning attorney said they should hire a fee-only advisor to manage their assets, and then they asked me if I charge fees or commissions. My client just referred their out-of-state best friend to an advisor in Alabama, even though I am also licensed in Alabama.

When I started in the early 1980s, financialplanning was all about sales, all the time. Retirement projections took the historical rate of return and projected that same return, every year, from the date of the plan out to the date of retirement in order to calculate the terminal value of a portfolio.

Money books for financial literacy. You’re not limited to dry explanations about portfolio allocations and tax strategies. The Investment Answer breaks down into five basic decisions to keep you focused and help you build a profitable portfolio. Here are some good ones to get you started: Investing and financialplanning.

Working with a financial advisor during this process can provide a wide range of benefits, such as: A holistic view of your finances: A financial advisor can analyze your current financial situation, assess your financial goals, and develop a personalized financialplan that fits your unique needs.

Friends and relatives can contribute to a 529 plan for college, for example. But sometimes, like when inflation is high, bonds can help cushion the blow of the economic instability that could impact your portfolio. Just make sure they fit in with your overall investment plan and money goals before you purchase.

It’s expected that your portfolio will respond to economic changes like inflation. . A balanced portfolio will typically be able to weather turbulent times. At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-onlyfinancialplanning.

The cover article talked about this professional bait-and-switch, and the cover of the magazine featured a monkey in a business suit, with the caption: “These days, everybody is a financial planner. ”. In our interview, Moore pointed out that literally anybody can hang out a shingle as a financial planner. Pandemonium!

I am an irreverent and fun marketing consultant for financial advisors. What is an advice-onlyfinancial planner? Advice-onlyfinancialplanning is fee-only comprehensive financialplanning without the expectation or even the option to manage any client investments.

It doesn’t mean that you can always take 4% out of your portfolio adjusted for inflation and expect to have a safe retirement. We are a fiduciary, fee-onlyfinancialplanning, and wealth management firm in Newtown, Pennsylvania. Our law firm is Yardley Estate Planning, LLC , and is in the same place.

Many people in this bucket have set up a simple investment plan. Here’s an example of a financialplan to ensure you are on track. You’re looking for tax help Tax help should not be confused with financial advisory help. So if you need to make a tax plan, these professionals will be more helpful.

Many people in this bucket have set up a simple investment plan. Here’s an example of a financialplan to ensure you are on track. You’re looking for tax help Tax help should not be confused with financial advisory help. So if you need to make a tax plan, these professionals will be more helpful.

Of course, this was never finalized. The second petition asks the SEC to stop pretending that giving financial/investment advice is “solely incidental” to the current wirehouse business model. giving advice on managing a client portfolio). [Note the term ‘ his ’ throughout.

I was not surprised to see, in the NASAA survey, that 41% of brokerage and independent BD firms (firms, in other words, that pay commissions to their reps) recommended private securities, compared with practically zero for fee-only advisory firms.

The largest advisory firms today look, to me, kind of like the wirehouses look: the advisors work for the firm rather than the client and they are told what advice to provide and what portfolio advice to give. Hurley says that the giant firms will build strong brands. This white paper is an echo of Hurley’s original forecasts.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content