This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

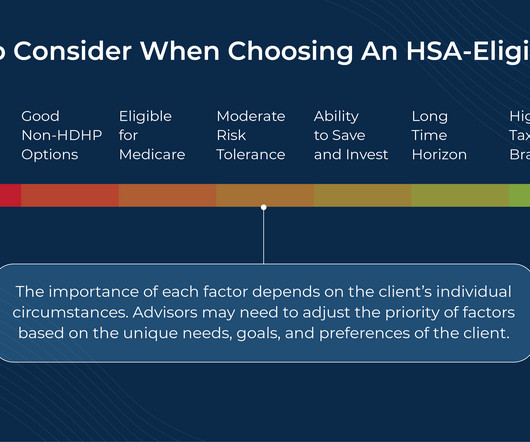

Health Savings Accounts (HSAs) have become an increasingly popular tool for financial advisors and their clients due in part to the 'triple tax savings' they offer: tax-deductible contributions, tax-free growth, and non-taxable distributions for qualifying expenses.

To achieve this, financial support may start at a very young age, allowing for a longer growth horizon and, in many cases, serving tax and estate planning purposes. 529 plans offer greater flexibility in ownership but restrict how funds can be used, particularly for educational expenses. Read More.

Related: Planning for Older Clients and Those with Disabilities Many GRATs include a so-called “swap” power in which the grantor is permitted to substitute assets of equivalent value with the GRAT. Handler is a partner in the Trusts and Estates Practice Group of Kirkland & Ellis LLP.

Also in industry news this week: A recent survey finds that next-generation employees at broker-dealers are looking for improvements in branding and social media promotion from their firms as they look to build their own practices and take the reins from a rapidly graying advisor population RIA M&A volume hit a record in the first half of 2025 (..)

Strategic charitable giving not only benefits the recipient but can also create significant tax advantages for the giver. While many people approach their financial planning with careful strategy, its easy to overlook the same level of intention when it comes to charitable giving. It just needs to be given to a qualified 501(c)(3).

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

The IRA and Roth IRA contribution limits are unchanged but income eligibility for tax-deductible IRA contributions and Roth IRA contributions have changed. Also updated: health savings accounts, flexible spending accounts, estate and gifting limits, qualified charitable distributions and other cost-of-living adjustments.

If you have no other IRA accounts, this conversion to Roth can be a tax-free event, especially if there has been no growth or gains on the investments in the account. The reader wanted to do just such a Roth conversion, but he also wanted to rollover some money from his 401(k) plan into an IRA.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

Would you like to diversify but also defer paying big capital gains taxes? Maybe it’s due to employee stock option plans. Their new ETF is coming out in December 2024: The Cambria TaxAware ETF – symbol TAX – is a solution to address just these challenges of concentrated positions. Maybe there was an IPO or a takeover.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

When you are preparing for retirement, you should keep in mind both financial strategies and what tax benefits you may gain. Older citizens can get helpful guidance from the Income Tax Department’s special brochure for retirement taxation matters. Key Tax Advantages for Retirees 1.

Without proper planning, taxes can unexpectedly take a large bite out of the proceeds, potentially reducing financial security and the legacy. When you understand various exit strategies and their tax implications early, you position yourself to make informed decisions that maximize after-tax value while ensuring a smooth transition.

Would you rather give that amount directly to the organization or withdraw $100,000, pay $40,000 in taxes and have only $60,000 of your contribution left to donate? Obviously, youd choose to avoid taxes and give the full amount, especially if that approach brought additional tax benefits with it. Note: This only applies to U.S.-based

. ~~~ About this week’s guest: Christine Benz is Director of Personal Finance & Retirement Planning at Morningstar; her new book is “ How to Retire: 20 Lessons for a Happy, Successful, and Wealthy Retirement. ” She joins Barry Ritholtz to discuss what you need to know about planning for retirement. Really, really interesting.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

These alternative investments can offer distinct advantages in the shape of portfolio diversification and the potential for higher returns, but they can come with equally distinct tax complications that need to be carefully planned for. What are the key tax strategies for alternative investments in 2025?

Donor-advised funds (DAFs) have emerged as powerful tools that deliver this exact combination, providing immediate tax advantages while offering flexibility to recommend grants to qualified organizations over time. Table of Contents What Are Donor-Advised Funds, and How Do They Work?

The post Tax Strategies for High-Income Earners 2025 appeared first on Yardley Wealth Management, LLC. Tax Strategies for High-Income Earners in 2025. In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations.

We also get you up to speed on the tax benefits of using a DAF. If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made.

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

Also in industry news this week: A recent survey indicates that younger "DIY" investors are more likely to be interested in working with a human advisor than their older counterparts, suggesting an opportunity for advisors to tap into this demographic (perhaps by setting minimum planning fees that ensure these clients can be served profitably today (..)

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well. 4 key benefits.

The post Securing Your Legacy: Financial Planning Tips for Your Children’s Future appeared first on Yardley Wealth Management, LLC. Securing Your Legacy: Financial Planning Tips for Your Children’s Future Introduction As parents, one of our greatest goals is to ensure our children’s future financial well-being.

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k). Complex setup process.

Without proper planning, healthcare expenses can quickly consume a significant portion of retirement savings. Financial advisors specializing in healthcare planning provide clarity and structure in this process. This is especially relevant for individuals who plan to continue working past the age of 65.

As dynamic as the secondary market may be, secondaries come with complex tax implications that can significantly impact returns if not properly managed. What are the tax implications of secondary transactions? What are the tax challenges in secondary transactions? What tax strategies optimize secondary investments?

For high-net-worth individuals, continuously refining your strategy over time is what keeps your plan efficient and aligned with evolving goals. At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations.

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

Estate planning is one of the most important steps in securing your financial legacy, but its also among the most complex. Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming.

While the appeal of real estate may be evident, complex federal, state, and local tax regulations can present a major challenge to the profitability of your property investments. Table of Contents Understanding real estate taxes What are the most tax-efficient ownership structures? Net Investment Income Tax (NIIT): A 3.8%

Keeping it safe, growing it wisely, and using it to support your future takes careful planning. Yet even the best financial plans can stumble. Mistake #2: Not having an estate plan in place Estate planning is essential for protecting what you’ve worked hard to build. Wealth management isn’t only for the ultra-rich.

When considering the various business structures available, understanding the tax implications is crucial for making informed decisions. A Limited Partnership (LP) offers a unique blend of operational flexibility and liability protection, but its tax treatment can be complex. Table of Contents What Is a Limited Partnership (LP)?

It probably depends on whether you have a strong plan in place for income during your retirement years. Having a retirement planning checklist can help make this final commute the time of reflection and joy it should be. Have a Financial Game Plan The importance of a plan cannot be emphasized enough.

The post Tax-Free Transfers from Your IRA to Charity: A Smart Financial Strategy appeared first on Yardley Wealth Management, LLC. Tax-Free Transfers from Your IRA to Charity: A Smart Financial Strategy At Yardley Wealth Management, we understand that many clients want to make a difference while also securing their financial future.

Photo credit: jb Employers have been giving us lots of opportunities to make this decision of late: when leaving an employer, whether voluntarily or otherwise, we have the opportunity to rollover the qualified retirement plan (QRP) such as a 401(k) from the former employer to either an IRA or a new employer’s QRP.

This can come from dividends, interest, rental income, and distributions from brokerage or retirement accounts. Understanding the full picture of income sources helps with financial planning and decision-making. Without a clear understanding of where money goes, it can be difficult to plan effectively.

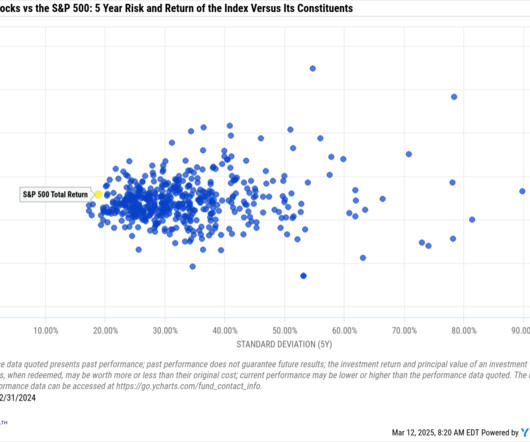

The situational nature of planning to diversify one large position cannot be over-emphasized, so it’s important to work with a financial advisor who has experience in this area. When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median stock underperformance was almost -10%.(J.P.

Private equity and alternative investments create unique tax reporting complexities that demand attention. This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on taxplanning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments.

A timely video explaining how recent Federal Reserve decisions might impact retirement planning can position you as the go-to advisor for your niche. For example, “The Complete Tax Optimization Guide for Healthcare Professionals” speaks directly to physicians and dentists who face unique tax challenges.

Traditional IRAs operate similarly to your workplace plan. Contributions are pre-tax, investments grow tax-free, and distributions are taxed as ordinary income. To add more tax-efficiency into your retirement planning, it’s also good to consider investing in a Roth IRA.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement.

The Growing Role of Philanthropy in Wealth Planning People today are more interested than ever in finding ways to align their long-term financial goals and their personal values. There are overall limits on charitable donation tax deductions, however. Values are among the most important things parents can pass on to their children.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content