This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: A recent survey indicates that younger "DIY" investors are more likely to be interested in working with a human advisor than their older counterparts, suggesting an opportunity for advisors to tap into this demographic (perhaps by setting minimum planning fees that ensure these clients can be served profitably today (..)

In case you don’t know what a 72t distribution is, this is shorthand for the Internal Revenue Code Section 72 part t (or IRC §72(t) for short), and the most popular provision of this code section is known as a Series of Substantially Equal Periodic Payments – SOSEPP is the acronym. Enough about the code section already.

Retirementplanning is a journey that generally takes decades to complete and most of us start out along the do-it-yourself path. More than likely, your first step was to enroll in an employer-provided plan such as a 401(k) or setting up an individual retirement account, also known as an IRA.

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirementplanning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

”, a series of measures that will have significant impacts on the world of retirementplanning. Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that Congress appears poised to pass “SECURE Act 2.0”,

From there, we have several articles on retirementplanning: The latest rules for 2023 Required Minimum Distributions from inherited retirement accounts. Why relying on Treasury Inflation-Protected Securities (TIPS) to support the bulk of retirement income needs could be risky.

This month's edition kicks off with the news that held-away asset management platform Pontera has raised $60 million in venture capital funding as advisors increasingly seek to directly manage clients' 401(k) and other outside assets – although an ongoing investigation by Washington state regulators over whether advisors' use of Pontera violates (..)

For instance, the Federal Adoption Credit provides a nonrefundable credit of up to $15,950 per child for adoptions in 2023 (claimed on 2024 tax returns), with no limit on the number of adopted children to whom this credit can apply.

A recent study shows that while many consumers have expressed an interest in ESG investing, such funds within retirementplans have received limited allocations from investors. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

Rowe Price has acquired Retiree Income, the parent company of popular retirement income planning software SSAnalyzer and Income Solver, to put its resources behind developing and distributing the company’s planning tools (albeit perhaps more to its retail and employee retirementplan clients than to advisors?).

This approach typically provides greater benefits to those who have significant assets and high taxable income in retirement. Note: most beneficiaries who inherit a retirement account from a non-spouse can no longer ‘stretch’ the distributions over their lifetime. Instead, they have to take the funds in 10 years.

We discussed the IRA Qualified Charitable Distribution (QCD) option for folks age 70½ or better in other articles. First of all, even though the age for RMD has increased to 72, the age for Qualified Charitable Distributions remains at 70½, so don’t get these two confused. and a number of miscellaneous credits.

Do you have a plan in place for your retirement? For many people, the extent of their retirementplanning includes signing up for the plan at work – which is often more of a starting point than a comprehensive retirementplan. You can use multiple accounts to help boost your savings.

RetirementPlanning 5 Ways to Catch Up on RetirementPlanning Later in Life Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Retirement is a significant investment, which is why so many financial experts recommend establishing goals and starting when still a younger adult. SIMPLE 401(ks) and IRAs

Whether or not rolling these assets into the Microsoft 401(k) plan is advantageous will depend on factors such as: Investment options in each plan compared to an outside custodian Consolidation and simplicity Whether you feel more comfortable with these assets in the Microsoft 401(k) than in an IRA with an outside custodian.

Retirementplanning for women can be trickier than most people may think. Most women I talk to are more concerned about paying less in taxes today than when they retire. Many people like the idea of paying less in taxes, But how does that relate to retirementplanning for women and a financially free retirement?

When you turn age 72, you’re required to begin receiving distributions from the plan. The distributions are generally based on your remaining life expectancy. And because that expectancy reduces as each year passes, the percentage distributed from your plan will increase slightly.

But here’s the thing: whether you retire at 50 or 67, it isn’t just about leaving work, but being ready for what comes after. Start planning early. It takes strategic foresight, hard numbers, and smart decisions that begin well before your final day at work. Yet far too many professionals delay the planning process.

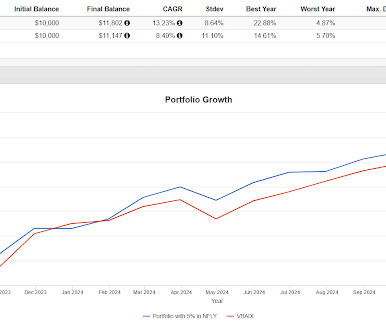

The YieldMax website says NFLY yields 40% and while that number moves around due to lumpiness in the monthly distribution and movement in the price of the fund, taken as a static number, 40% from a 5% holding implies getting 200 basis points of yield out of a pretty small portion of the portfolio.

And how does it compare to the 401k and other retirementplans that exist? With most 401(k)s you must work for the employer for a certain number of years to be vested. Being a self-employed retirementplan , the SIMPLE IRA gives you the discretion of what exactly you want your money invested into. .

Any benefit reduction due to earnings above the threshold will be recovered once you reach your FRA on a gradual basis over a number of years. Related Posts: Managing Inflation in Retirement Is a $100,000 Per Year Retirement Doable? The loss of benefits is temporary versus permanent. Photo by Sharon McCutcheon on Unsplash.

While distributions taken from a traditional IRA after age 59½ are subject to ordinary income tax, distributions made from a Roth IRA will be tax-free if the account has been in existence for at least five years. Otherwise, there’s no requirement for your child to make a direct contribution into the plan. Ads by Money.

These rates aren’t just static numbers; they should be assessed within the context of your financial future. Consider other donation options, like contributing appreciated securities or making qualified charitable distributions from IRAs if you’re eligible.

Matt Kory, Vice President, Retirement Programs As a retirement income vehicle, the 401(k) is second in popularity only to Social Security – and as CNBC reported in 2019 the number of 401(k) millionaires is at an all-time high. But is a million dollars even enough for your retirement needs? Just think of the numbers.

Further, both examples ignore other sources of income, such as wages, pre-tax retirement account distributions, dividends, etc., Considering tax planning strategies to reduce the impact of the new MA surtax. The simple examples above only illustrate the state tax impact, but federal tax implications will also apply.

Roth IRAs don’t come with Required Minimum Distributions (RMDs) at age 72 like a traditional IRA either, so you can continue letting your money grow until you’re ready to access it. When you do decide to take distributions from a Roth IRA, you won’t have to pay income taxes on that money. Not sure about your future tax brackets?

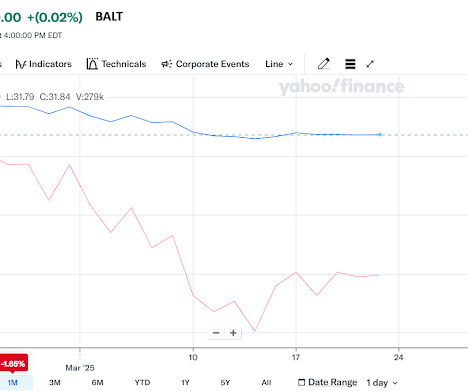

YTD it shows down 0.2%, so it went up a little for the first six or seven weeks of the year, down very little from the peak and the YTD number could be as simple as the last trade hitting the bid. BALT has never paid out a distribution so it is tax efficient. Is anyone using BALT as a fixed income substitute?

Employee Stock Ownership Plans (ESOPs) An ESOP allows owners to gradually sell their shares to employees through a qualified retirementplan. Buyers, however, may inherit more risk, which can affect the sale price or deal structure. This approach can create win-win outcomes for both you and your staff.

The distributions add up to $7.96 The S&P 500 excluding tech compounded negatively at 2.42% (taking numbers generated by Copilot and plugging them into testfol.io). TSYY shows on Yahoo as dropping from $11.15 at Wednesday's close to closing at $10.59 last Thursday. All this is per Yahoo.

According to the Department of Labor , “Based on the experience of Council members, and testimony and conversations with recordkeepers, the value of uncashed retirementplan checks likely exceeds $100 million per year but could be considerably larger. The next key step is to consolidate all of your retirement accounts.

Unless there is a BulletShares type of treasury ETF out there that matures, the typical treasury ETF will distribute at the prevailing interest rate. The road between Ramah and Gallup has a relatively high number of vehicle accidents though. The picture is from the Airbnb where we stayed for one night. It's on a 100 acre parcel.

Printed materials such as brochures, flyers or handbooks that detail the benefits package can be distributed. What we found surprising is that this is the first year that saving for retirement is not the primary financial stress factor for employees. Watch our video series on Business RetirementPlans to learn more.

More Generation X retirement doom today from both Bloomberg and Yahoo. Grim numbers aplenty with average 401k balances in the very low six figures and median numbers much lower than that. million for retirement which is up from $1.7 What are your numbers? What income streams will you have to cover those numbers?

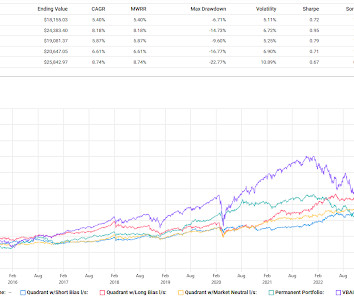

OMFL had the highest CAGR with a tradeoff being a standard deviation which makes sense but that the worst year number, 2022, is so much lower is very interesting. The time frame is short with these three because DYNF is pretty new but they are all close most of the time but not always. The above data is interesting. I wouldn't bet on it.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. In recent years, a number of states developed a sort of workaround for business owners to navigate the SALT cap. The TCJA has many provisions that are set to expire (sunset) at the end of 2025.

We've talked about these quite a few times noting that they have trouble outpacing their distributions and that the YieldMax TSLA ETF (TSLY) has already done a reverse split. The growth numbers assume dividends are not reinvested. These are the single stock, covered call ETFs that have extremely high yields that we mentioned yesterday.

So I take that as a good number to study for this blog post. The idea was similar to what ReturnStacked talks about in terms of adding enough alt exposure to matter without giving up equity exposure. " Now imagine you take 25% proportionally out of 60/40 and put it into the uncorrelated alternative."

How To Grow Your RetirementPlan Business In The 2020 Economic Crisis. We’ve partnered with the experts at The Retirement Learning Center to update advisors on how the retirementplan landscape has been altered by the 2020 economic crisis. Save your spot today! So I’ll let John take it away from here.

By weaving in extra savings into your spending plan, you can have enough money to cover gifts, cook your fancy holiday dinner, and keep the lights on (literally). . Max Out Your RetirementPlans. Saving for retirement should be as commonplace as meal prepping for the week. Let’s take a look at 2021 numbers. .

According to Claude.ai, 70% of BRW's April distribution was ROC. From 2023 on, it's been mostly able to keep up with the distributions which for a closed end fund is pretty good. The return numbers for all are price only for anyone interested in taking the income out.

Your asset allocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. But depending on the investment options in the retirementplan, as the balance grows, it may be advantageous to customize your asset allocation. Then work down, perhaps going to U.S.

Personal Information Social Security Numbers (SSN) or Individual Taxpayer Identification Numbers (ITIN): Needed for you, your spouse, and any dependents for identification purposes by the IRS. Bank Routing and Account Numbers: Required for direct deposit of any refunds or for payments due.

Yahoo had it down 17.01% in 2022 (add back about 4% in distributions). I think those numbers make for a good tradeoff especially since Portfolio 1 was down less than half VBAIX' 2022 decline. The Quadratic Interest Rate Volatility And Inflation Hedge ETF (IVOL) is a tough one to figure out.as in I can't figure it out.

Looking at something like Yahoo Finance shows XYLD down about 22% last year but you need to add back in 12% of distributions to get a more accurate picture which Portfoliovisualizer does. What they don't do is they don't look like the stock market despite correlation numbers that say otherwise. that vast majority of the time.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content