This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To achieve this, financial support may start at a very young age, allowing for a longer growth horizon and, in many cases, serving tax and estateplanning purposes. Parents often want to ensure their children have the resources to pursue their potential and lead fulfilling lives. Read More.

Strategic charitable giving not only benefits the recipient but can also create significant tax advantages for the giver. While many people approach their financial planning with careful strategy, its easy to overlook the same level of intention when it comes to charitable giving. It just needs to be given to a qualified 501(c)(3).

Irrevocable trusts lie at the heart of a variety of estateplanning strategies, as gifts to irrevocable trusts can allow for the transfer of assets outside of an owner’s estate for estatetax purposes with more structure than an outright gift. the assets' original owner).

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

Estateplanning is one of the most important steps in securing your financial legacy, but its also among the most complex. Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming.

obliviousinvestor.com) Estateplanning Changing an estateplan takes time. wealthmanagement.com) Do your clients have a digital estateplan? thinkadvisor.com) How tax treatment differs across states for 529-to-Roth IRA rollovers. advisorperspectives.com) Fidelity Charitable distributed $11.8

One of the most important decisions you’ll make when designing your estateplan is who to name in the various fiduciary roles: trustee, personal representative, executor and agent. While a critical decision, it’s often given significantly less thought than the distribution of your assets.

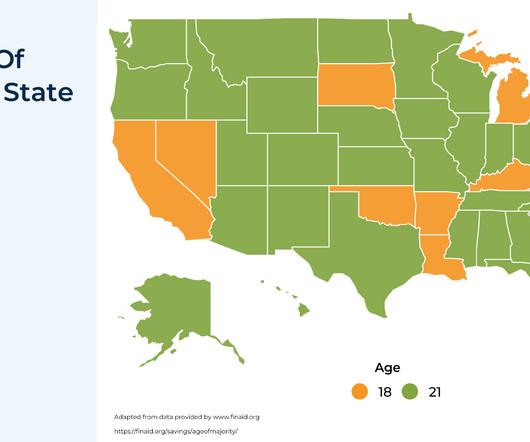

The role of estateplanning is most commonly considered to be about transferring assets from one generation to the next in the most efficient manner possible (e.g., how to minimize the burden of estatetaxes and avoid the public spectacle of the probate process). at age 21 or 30) or stagger distributions at multiple ages.

The role of estateplanning is most commonly considered to be about transferring assets from one generation to the next in the most efficient manner possible (e.g., how to minimize the burden of estatetaxes and avoid the public spectacle of the probate process). at age 21 or 30) or stagger distributions at multiple ages.

Estateplanning can be difficult to think about, let alone plan for. Maybe you’ve avoided putting together a concrete plan because you don’t want to think too far into the future when it’s time to pass on what you have. Or maybe you don’t think an estateplan is necessary because you’re not rich enough to warrant one.

Understand the basics first, and then create an estateplan. Wills and trusts are both important estateplanning tools with important differences. A will ensures property is distributed after your passing, according to your wishes, while a trust goes into effect as soon as you create it. A Will vs. a Trust.

And so the conundrum of people with "too much" savings in their 529 plan – either because they overestimated how much they needed to save, or because they chose a different path entirely that didn't involve going to college – has been how to get funds out of the plan without sacrificing a large part of their value to taxes and penalties.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

The post Tax Strategies for High-Income Earners 2025 appeared first on Yardley Wealth Management, LLC. Tax Strategies for High-Income Earners in 2025. In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations.

Mistake #2: Not having an estateplan in place Estateplanning is essential for protecting what you’ve worked hard to build. A good estateplan ensures your assets go where you want them to. It can also help reduce taxes and make life easier for your family during difficult times. The result?

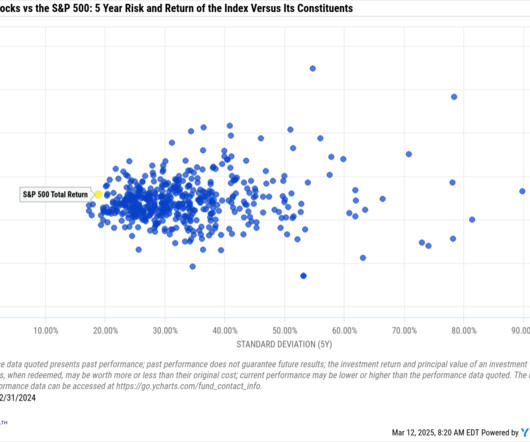

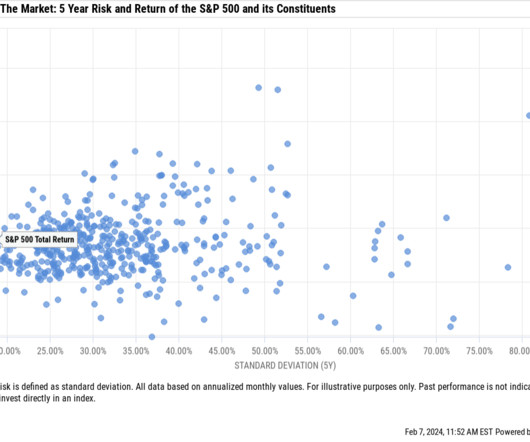

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median stock underperformance was almost -10%.(J.P. Charitable Contributions: Donating appreciated stock to charity while reducing capital gains tax. Gifting: Transferring stock to family members or trusts.

Fortunately, financial professionals have tools and wealth transfer strategies that can help couples be intentional about the use of their assets in an estateplan. Why Focus on EstatePlanning for Blended Families A thoughtful plan and good communication can go a long way in heading off conflict in large families.

The post Tax-Free Transfers from Your IRA to Charity: A Smart Financial Strategy appeared first on Yardley Wealth Management, LLC. Tax-Free Transfers from Your IRA to Charity: A Smart Financial Strategy At Yardley Wealth Management, we understand that many clients want to make a difference while also securing their financial future.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well. 4 key benefits.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

Start saving early by contributing to tax-advantaged accounts like 529 Plans or Coverdell Education Savings Accounts (ESAs). These accounts come with tax benefits that can alleviate future financial pressures when it’s time for your child to attend college.

For high-net-worth individuals, continuously refining your strategy over time is what keeps your plan efficient and aligned with evolving goals. This guide consolidates what we’ve learned to help you refine, update, or pressure-test your current retirement and estate strategy with confidence.

EstatesEstatePlanning in this Economic Climate Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. If you are in the middle of estateplanning , consider the following strategies to develop a sound plan amidst widespread economic challenges. . Create a Trust .

Provisions of the SECURE Act may require advisors to revisit estateplans for clients who aren't utilizing their RMDs or who have qualified assets intended for the next generation. Some clients may benefit from strategies for using life insurance to maximize the value of qualified assets while minimizing their tax burden.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. The absence of required minimum distributions during the owner’s lifetime.

Positioning Philanthropy as a Cornerstone of Legacy There are many reasons for giving during your lifetime, including supporting causes you care about, making a positive impact on the world, and accessing certain tax advantages. There are overall limits on charitable donation tax deductions, however.

The Imperative of EstatePlanning: Not Just for the Affluent Often, there’s a prevailing misconception that estateplanning is a luxury reserved for the wealthy elite. Real estateplanning is a crucial undertaking that every adult and family should prioritize.

While a financial plan focuses on managing your finances during your lifetime, an estateplan is essential for determining the fate of your assets after you pass away. Estateplanning involves the transfer of your assets to your heirs in the event of your passing.

A financial advisor can help with maximizing your retirement income through taxplanning After retirement, your income sources may become limited to pensions, Social Security benefits, and investment income. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income.

Only 26% of Americans have an estateplan. If you’re thinking, “But my clients are high-net-worth…many more have an estateplan.” These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions.

This can come from dividends, interest, rental income, and distributions from brokerage or retirement accounts. A helpful approach is to categorize expenses into: Fixed expenses: Mortgage, rent, property taxes, insurance, and loan repayments. Earn Earnings go beyond just a paycheck. Invest Investing can help savings grow over time.

Here is a great way to value those items if you are eligible to take a tax deduction. Property donations will need acknowledgment of receipt from the charity and items totaling over $500 will need a special form (IRS Form 8283) when filing your taxes. Items totaling over $5,000 will need an appraisal.

When those changes involve tax law, it is extremely important for clients to meet with their financial professional, tax advisor, and legal advisor to discuss any adjustments that may need to be made to their financial, retirement, or estateplan. My guests today are two members of the MassMutual team.

When those changes involve tax law, it is extremely important for clients to meet with their financial professional, tax advisor, and legal advisor to discuss any adjustments that may need to be made to their financial, retirement, or estateplan. My guests today are two members of the MassMutual team.

4] Leaving a Legacy for Future Generations To ensure the preservation of generational wealth, retirees must plan for the distribution of their assets after their passing. It can be a good idea to work with an estateplanning professional to develop a solid plan that includes wills, trusts, and other legalities.

Forces such as inflation and taxes can have a massive impact on long-term wealth, and it can be very important to educate other generations in your family about these issues. [5] 6] Trusts are useful because they can provide tax advantages and financial protections for your money. [7]

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median underperformance was almost -10%.³ A deep discussion of these strategies is outside the scope of this overview, and because every situation is so different, be sure to discuss your situation with your tax and financial advisor.

Bear in mind that IRA accounts do have income restrictions so it is important to work with your financial advisor or tax preparer to determine if you are eligible to contribute in 2022. Assuming you are eligible, these accounts can be quite tax advantageous for your overall financial situation. 529 College Savings Plans.

Depending on the nature of the windfall, planning opportunities and considerations will vary. For example, the tax laws and distribution terms for an inheritance is quite different to the tax and liquidity considerations during an IPO. In their situation, it meant they could sell all their shares tax free.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

Melissa Rodriguez June 11, 2025 5 Min Read As the most significant intergenerational wealth transfer in the history of the United States unfolds, women, particularly widows, are increasingly at the forefront of estate management and disputes.

No-one loves paying taxes. Did you know you can buy crypto through an IRA and receive the same tax benefits? Just like with other assets, if you buy crypto through an IRA, the tax will be paid at your income tax rate at retirement. You can see the crypto advisor tax webinar replay here. Manage your timing.

As a company founder, early startup employee, or small business owner, you may find yourself in a higher tax bracket as your business grows or you realize gains from equity compensation. But that doesn’t mean you simply have to accept a higher tax bill. Here are 20 tax-efficient actions to consider when filing your taxes in 2024.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content