This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s this unique vantage point, and depth of knowledge and empathy, plus a natural ability to “connect the dots” that have earned Jason the trust and respect of the industry’s most sophisticated financial advisors at one of the nation’s leading recruiting and consulting firms. Jason is a graduate of Emory University in Atlanta, Ga.

With more than 25 years of industry experience, he has set the strategic vision for the firm, which encompasses AssetMark’s platform of curated investments, technology solutions, business consulting, operations support, and acquisitions that serve the best interests of financial advisors and their investors.

According to a recent survey commissioned by Kestra Financial and Bluespring Wealth Partners, less than half (41%) of first-generation advisors have transferred equity to successors, and just 6% of those planning to retire within 10 years have a fully documented succession plan. When do they graduate into building an enterprise?

You can't do this in isolation, you need a team," said Terranova, senior managing director at Virtus Investment Partners, when asked by WealthManagement.com Executive Editor Diana Britton about who he uses as his advisor to handle tax and estateplanning and more. “I

Related: M&A Advisory Gladstone Launches $500 RIA Seller Connection Service NFP Buys Wealth and Retirement Firm Levine Group Aon-owned NFP has acquired a former Kestra Holdings-affiliated firm based in Brentwood, Tenn. Levine Group will join NFP, which does wealth management, retirementplan advice, insurance and benefits consulting.

Tony is an industry speaker, consultant, trusted advisor, and active investor that specializes in GTM strategies—with a heavy emphasis on marketing—for financial services firms, RIAs, and FinTech companies. Read more about: Wealth Management EDGE Tech for Growth About the Author Anthony M.

I took the chance to recharge a bit; I did some advisory, coaching, consulting work. Most recently, he was serving as head of the wealth management business and chief marketing officer. When I left the firm, after about 10 years, frankly, it was time to take a break. This opportunity with Choreo really stood apart.

Related: Montis Financial: Creating a Raving Fan Experience Also, the people and consultant ecosphere was smaller, and it was very challenging, either externally or internally, to find the experts that we needed in order to build as quickly as we wanted.

Louis Diamond , CEO, Diamond Consultants June 10, 2025 4 Min Read As summer approaches, it’s easy to drift into vacation mode. About the Author Louis Diamond CEO, Diamond Consultants Louis has guided many of the top teams in the industry as they’ve transitioned to other employee-model firms or launched RIA firms.

Each discussed how providing a more holistic approach to distribution-phase planning in their practices can amp up organic growth for advisory firms. I cannot say enough about how well received this last session was by advisors, several of whom came up later to say thanks.

At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations. This guide consolidates what we’ve learned to help you refine, update, or pressure-test your current retirement and estate strategy with confidence.

These professionals help you define clear financial objectives and create actionable plans to achieve them, whether you’re planning to buy a home, save for college, or prepare for retirement. RetirementPlanningRetirementplanning is one area where talking to a financial planner proves particularly worthwhile.

Maximize Your Retirement Contributions: Enhancing your retirement savings not only secures your future but also offers immediate tax benefits. For 2024, the IRS has increased contribution limits: – 401(k), 403(b), and most 457 plans: You can contribute up to $23,000.

For instance, I will contribute an additional $10,000 to my retirement fund this year or I will pay off my $15,000 credit card balance by December 2025. Outcome: Define Your Big Financial Goals Set a Clear Spending Plan Create a budget that prioritizes your values. A spending plan isnt about restrictionits about intentionality.

Checklist: Year-end Tax Planning Strategies Review the following tax strategies with your tax advisor and/or financial advisor before the end of the year. Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income. GET STARTED 1.

Life transitions such as marriage, divorce, the birth of a child or grandchild, career changes, retirement, an inheritance, or the purchase or sale of a home can all influence your broader financial picture. These events may affect your investment approach, tax planning strategies, insurance needs, and estateplanning documents.

But Here’s the Rub A comprehensive discussion along the lines suggested in the article I posted will require a lot of work by the agent, including all the data gathering, consultation with advanced planning attorneys, coordination with other advisors, presentation preparation, etc. Ratner Charles L. See more from Charles L.

Unexpected events can derail your progress toward your goals and even your financial security if you don’t have a plan for managing them. Financial planning should ideally involve every area of your financial life because they are all interrelated. Estateplanning. Plan for retirement. Create an estateplan.

Whether it’s investment planning, retirementplanning, tax strategy, estate management, insurance planning, or holistic money management, the CFP designation proves that you can deliver advice that is both competent and client-centric.

This can come from dividends, interest, rental income, and distributions from brokerage or retirement accounts. For example, if funds are invested in a brokerage or retirement account, they may generate dividends or interest, which contribute to total earnings. Save Saving involves setting aside money for future needs or goals.

There are so many products out there – 401(k)s, mutual funds, Individual Retirement Accounts (IRAs), Exchange-Traded Funds (ETFs), bonds, Real Estate Investment Trusts (REITs), etc. Many financial advisors offer one-time consultations or even subscription models for ongoing support. You also do not need to commit forever.

For audit-ready best practices, consider consulting with a tax professional in real-time, especially for mixed business and personal expenses. These variables can significantly impact the final deduction amount, necessitating strategic planning to optimize this benefit.

At any given moment, people are working towards multiple goals like saving for retirement, managing taxes, buying a home, protecting their family through insurance, or planning for healthcare needs. Most individuals do not have the time or energy to consult with multiple financial professionals across different firms.

If the total positive UBTI across all applicable investments in a retirement account equals $1,000 or more, the tax-exempt entity is required to file Form 990-T and pay tax on the UBTI. This is an important consideration for high-income individuals using tax-advantaged retirement accounts for alternative investments.

Additionally, you also need to consider domestic disputes and estateplanning issues related to property. Additionally, you must maintain appropriate business insurance and consult with wealth managers and legal experts to ensure ongoing protection. So, consult with a qualified tax professional before executing it.

Published: March 21st, 2025 Reading Time: 6 minutes Written by: The Zoe Team Managing wealth involves more than just investingit requires careful planning, strategic decision-making, and a long-term vision. EstatePlanning : Ensuring your wealth is passed on according to your wishes. Optimizing tax-efficient retirement income.

People usually arrive at this conclusion if they have changed jobs or just want better control over their retirement funds. A 401(k) rollover refers to transferring money from one retirement account, such as an old employer’s 401(k), into a new 401(k) or an Individual Retirement Account (IRA). Why consider a rollover?

Offer free consultations to bring in new clients. You can discuss retirementplanning, simple investing for beginners, or estateplanning. Hold workshops in the community to teach people about finances. Make online videos that explain money concepts simply. Keep up with financial news and trends to help clients.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. This flexibility becomes increasingly valuable as your retirement portfolio grows more complex.

Download a free guide to estateplanning and get the tools you need to protect your wealth, honor your values, and provide for your loved ones. Here’s a better structure you can try for an effective call to action for financial advisors: Your Guide to Protecting What Matters: Safeguard your legacy today.

However, you may want to consult with a financial professional on which one or which combination of them may make the most sense given your unique financial situation and goals. Once the child reaches the age of majority and is working full time, they can continue using the account for future retirement and would not have to open a new one.

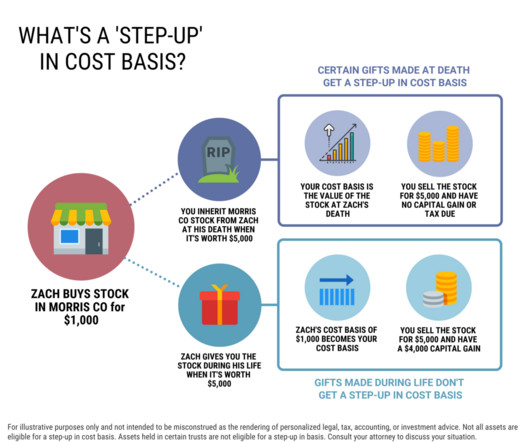

Non-retirement assets like stocks in a brokerage account, inherited home , antiques/art/collectables, or other real estate, are generally eligible for a step-up in cost basis. Retirement accounts and IRAs do not receive a stepped up basis. Though there can be exceptions (again consult a tax advisor and attorney!),

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

Step-Up in Basis (EstatePlanning for Alternative Investments): When heirs inherit alternative investments, the cost basis is ‘stepped up’ to the fair market value at the time of the original owner’s death, eliminating any unrealized capital gains. Can I hold alternative investments in my retirement accounts?

The post How Do You Turn Retirement Savings into a Reliable Income Strategy? How Do You Turn Retirement Savings into a Reliable Income Strategy? You’ve likely spent years building your retirement nest egg—saving diligently, investing wisely, and contributing to retirement accounts along the way.

When it comes to estateplanning, there are many pieces to ensure that your heirs and loved ones are taken care of and have a clear understanding of your wishes. Any estateplanning professional would tell you that the more you do while you are still living, the better. However, this is a very common misconception.

Fred Barstein , The Retirement Adviser University, June 9, 2025 6 Min Read Mihajlo Maricic/iStock/Getty Images Plus While the defined contribution market is finally capturing due attention from the financial services industry and mainstream media with $12.5 Convergence of wealth, retirement and benefits at the workplace 3.

In this guide, we’ll explore the key tax changes in effect for 2025, how theyll influence your filing status, retirement savings, investment, and estate planningand offer strategic advice to help high-income and high-net-worth individuals prepare more effectively for upcoming coming tax changes.

You know, I thought I was gonna take the high road and, and be a management consultant. Lisa Shalett : Yeah, so, you know, I, I did the consulting thing both before and after business school. That was one of the pieces of the consulting gig that appealed to me. So that’s what I did for the first job.

They can have a direct impact on the stock market, and by extension, on your retirement investments, including your 401(k). If you are unsure how this impacts your personal retirement strategy, you can also consult a financial advisor to understand the impact of tariffs on the stock market and how you can protect yourself.

Having the opportunity to tell your whole story is how you eliminate all objections, indoctrinate your audience, and move them to book consult calls. Unlock Your Retirement Potential Free Seminar) Keep the email short, focusing on benefits and a clear CTA. Appointment-booking CTAs: Encourage attendees to schedule a free consultation.

The post Strategic RetirementPlanning Guide for Single Women: Expert Financial Advice appeared first on Yardley Wealth Management, LLC. Without a partner to rely on for financial support, single women must take proactive steps to ensure a secure and comfortable retirement.

Important Consideration: Due to the complexity of the rules and nuances, it is crucial to discuss your specific situation with a financial advisor, estateplanning attorney, and tax professional. If you need the cash flow and there aren’t any other inherited assets, then this type of income tax planning may be moot.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content