This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

RIA Edge Podcast: Schwab’s Jalina Kerr on How Resilient RIAs Can Turn Market Volatility Into Growth RIA Edge Podcast: Schwab’s Jalina Kerr on How Resilient RIAs Can Turn Market Volatility Into Growth Jalina Kerr of Charles Schwab shares how the most adaptive firms are expanding beyond portfolio management, into areas like estate and taxplanning.

In our 103rd episode of Kitces & Carl, Michael Kitces and client communication expert Carl Richards discuss the challenges of finding an optimal balance between proactively providing value and the consistency of simply being available to respond to clients when they come to their advisor for assistance. and gaining their trust.

The ‘millionaires’ tax will also ensnare taxpayers who exceed the $1M limit after selling a home, business, stock options, or other types of one-time events. Article is a general communication only and should not be used as the basis for making any type of tax, financial, legal, or investment decision.

To protect yourself in the event of an audit, maintaining thorough documentation is essential. Some meal expenses can qualify for 100% deductibility under specific circumstances, such as company-wide events, or meals provided for the convenience of employees during overtime work, or staff meetings.

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

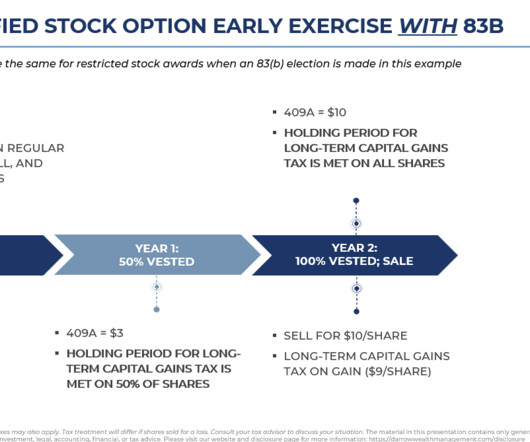

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. It can also preclude some taxplanning strategies down the road.

By Mike Valenti, CPA, CFP ® , Director, TaxPlanning Corporate executives often receive the brunt of the U.S. tax system. Typically, most or all of their income is W-2 income and subject to the higher ordinary tax rates as well as FICA taxes.

The 83(b) election has the potential to significantly reduce the overall tax liability, especially for startup founders and employees who receive stock-based compensation. It’s usually a key part of pre-IPO taxplanning and exit strategies. M&A implications. Cash requirements.

Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and taxplan. An endowment offers benefits that can extend beyond tax deductions and financial efficiency. Managing a Charitable Endowment Fund Once an endowment is established, it must be maintained.

SmartOffice — SmartOffice , the customer relationship managemen t s olution from Ebix, is a financial planning CRM that helps financial advisors tackle critical tasks like analysis, communication, and client services. . CRM systems make it easier to juggle tasks, opportunities, and communications.

When unforeseen events created challengeslike significant market downturns, sudden financial hardships, or changes affecting the ability to pay tax liabilitiesrecharacterization offered a way out. Liquidity concerns often prompted investors to reverse conversions when they discovered insufficient funds to cover the resulting tax bill.

Article is for informational purposes only and should not be misinterpreted as personalized advice of any kind or a recommendation for any specific financial or tax strategy. This is a general communication should not be used as the basis for making any type of tax, financial, legal, or investment decision.

From quarterly estimated taxplanning to equity compensation and crypto taxplanning, diversifying your service offerings can not only set you apart from the competition, it can also help you significantly grow your revenue and retain clients.

As a refresher, some of the most popular forms of marketing include: Events Webinars Social Media Email Marketing SEO/Website Traffic Podcasts Video/YouTube PPC Read on to see real-life examples of financial advisors using some of these marketing tactics and how they worked for them. Looking to start planningevents for your firm?

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. It can also preclude some taxplanning strategies down the road.

As a Harness Marketplace member, Klingman & Associates works with tax firms on the Harness platform to refer and serve clients dealing with equity compensation, liquidity events, and other high-net-worth planning needs. Q: How can tax advisors align with the work of wealth advisors? It’s often event-driven.

Aside from the tax bill, you’ll want to have enough cash or resources to live on to minimize your taxable income in the year of conversion. As you consider your cash runway and resources, remember to consult your financial and tax advisors to discuss taxes, penalties, and distribution rules.

This email address will be used for communication regarding the report. How Harness can help with BOI reporting In the event that BOI reporting requirements are reinstated, company owners are advised to seek professional advice. In any event, it’s important to stay informed about any updates from FinCEN.

Core components of CAS involve bookkeeping, payroll, taxplanning & compliance services customized for each client. TaxPlanning and Compliance With any of the above components, taxplanning and compliance will be a major area of need, particularly for newer businesses.

Expertise in TaxPlanning & Compliance: A CPA can help you identify tax-saving opportunities and help keep your clients in compliance with tax laws, reducing the risk of costly penalties and fees. This can allow you both to work together to come up with solutions before tax season.

Delivering accurate and timely compliance requires enough personnel with the necessary expertise, and the shortage is compromising this fundamental aspect of tax practice. Hosting strategic talent search events: Beyond online engagement, in-person and virtual events can also provide valuable opportunities to connect with potential talent.

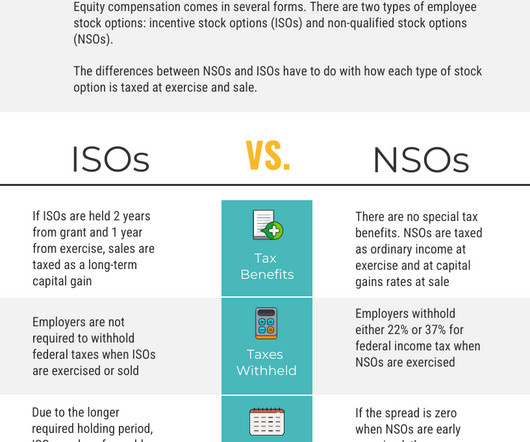

“Preferably someone holding stock options (ISOs or NSOs) with limited understanding of the tax implications of their holdings,” Kelley explains. Onboarding tax clients with ease “Client onboarding is pretty quick with Harness. His team consists of Gabe, from the Harness Concierge team , and Francis, a senior tax associate at Harness.

While many firms offer investment and financial planning, we go the extra mile by offering taxplanning and advice, as well as business consulting and insurance and estate planning, just to name a few. We had to quickly learn how to adapt to new ways of communicating with clients and with each other as a team.

Getting the right financial advisor: Financial planning for high-net-worth individuals can include taxplanning, managing philanthropic activities like charity, asset protection, estate and succession planning, and risk management, among several other things. also require a change in your primary financial plan.

Article is for informational purposes only and should not be misinterpreted as personalized advice of any kind or a recommendation for any specific financial or tax strategy. This is a general communication should not be used as the basis for making any type of tax, financial, legal, or investment decision.

TaxPlanning: Help clients learn smart tax strategies. Discuss estate planning and how financial decisions can impact taxes. You should plan your content before time. Think about holidays, financial news, and important events in your field. You could invite clients to events that show appreciation.

Financial Planning Needs: Retirement planning Education and family planning Obtaining appropriate insurance coverage Business and taxplanning Significant asset purchases Strategies for Serving Clients in This Stage: Clients at this stage are experiencing life events — both large and small — that will impact their financial planning needs.

Therefore, it is vital for couples to communicate and make decisions together on financial matters. If you get divorced or in the unfortunate event of your spouse’s demise, your personal financial wishes and goals should not be compromised. The salary is more, the comforts are higher, and there is better liquidity.

In case of any doubt or discrepancies, it is vital to communicate with your financial advisor openly. Communication is key in the evaluation of investment performance. Communication is key in the evaluation of investment performance. Transparent communication is paramount in risk management.

Our generation has lived through some of modern history’s most monumental economic and social events. Everyone has unique stressors, but the most common are saving money, managing debt, and planning for retirement. Generation Y has, for lack of a better term, “been through it.” The result? Stress, and for some, lots of it.

presidential election, we have grappled with the lack of clarity regarding the details of new tax legislation. The outcome of the tax reform debate is likely to impact how we advise clients on taxplanning, estate planning and a host of other topics. Since last year’s U.S. Those conditions do not exist today.

If you own a stake (or plan to invest) in a startup or small business, you need to know about an important taxplanning tool available to you. If you qualify, you may be able to avoid federal taxes on any and all capital gains you realize when you exit.

If you own a stake (or plan to invest) in a startup or small business, you need to know about an important taxplanning tool available to you. If you qualify, you may be able to avoid federal taxes on any and all capital gains you realize when you exit.

However, if ISOs are cancelled and paid out (typically in conjunction with an acquisition), payroll taxes are generally assessed on the spread in addition to ordinary income tax. Especially for founders and early employees, stock options can create a major liquidity event that transforms your financial life.

Take taxplanning, for example. Robo-advisors are designed to look for basic tax-saving opportunities, such as tax-loss harvesting. The original savings plan will no longer fit in with your life. Now, lets say you are an active-duty military member. Suddenly, your financial priorities change.

Retirement Planning : Offer tips on saving and managing retirement funds. TaxPlanning : Discuss effective ways to manage taxes and how your financial choices can affect them. You need to plan your material according to holidays, news, and events in your industry. Communicate with your followers regularly.

In cases like these, outside counsel can help you navigate money worries and major life events. A Certified Public Accountant (CPA) is best equipped to support all your tax needs. A CPA who is also passionate about financial planning will be able to touch on your bigger financial picture while homing in on your taxes.

In cases like these, outside counsel can help you navigate money worries and major life events. A Certified Public Accountant (CPA) is best equipped to support all your tax needs. A CPA who is also passionate about financial planning will be able to touch on your bigger financial picture while homing in on your taxes.

When you have the resources to make an impact, this type of planning helps you pinpoint what you want to accomplish for your family, community, and society. Steps to Setting Up a Philanthropy Fund Taking the proper steps in the beginning can give your charitable giving plan a solid foundation. Reputational risk. Governance risk.

Mike Valenti, CPA, CFP ® , Director of TaxPlanning Tom Fridrich, JD, CLU, ChFC ® , Senior Wealth Planner It’s January, so it’s officially tax season! One of the most common client questions heard by tax preparers is, “So, what do you need from me?” The short answer to that question is often, “Everything.”

Unfortunately, the Commonwealth also passed a ‘millionaire tax’, which adds a 4% surtax to taxable income over $1M , even for one-time sudden wealth events. To expand the tax benefits past the 10x/$10M limits, consider planning strategies such as gifting stock to family members. Form 8949 and Schedule D).

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. For average earners or those with modest-sized estates, doing so will not create a federal estate taxevent for their estate or inheritors.

For various reasons, making lifetime gifts may be more efficient from an estate and gift tax standpoint than transferring assets through a last will and testament. When clients have sufficient assets to warrant estate taxplanning, we often recommend transferring a considerable amount of their estate to trusts that benefit family members.

Paying tax now instead of later goes against the grain of conventional taxplanning. the owner plans to spend down the account in retirement), the benefits of converting may be minimal, as those benefits take a long time to accrue.a Some factors to consider: If the ultimate beneficiary is: the account owner (i.e.,

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content