This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, despite the large number of potential conflicts that exist for advisory firms, much of the financial media and the general public tend to focus specifically on the conflicts caused by commission-based fee models.

The two most common pricing models are fee-only financial planners (flat-fee or fixed-fee advisors) and AUM-based financial advisors (who charge a percentage of assets under management). While AUM advisors may seem appealing, they often come with high lifetime fees and potential conflicts of interest.

Consider this: you walk into a Bank of America branch and ask for the best type of savings account on the market. Only registered investment advisors have a full-time fiduciary duty to their clients. Most fiduciaries don’t sell products: Most fiduciary advisors are only paid by a percentage of assets they manage for clients.

Concept of digital social marketing. According to a recent survey commissioned by Kestra Financial and Bluespring Wealth Partners, less than half (41%) of first-generation advisors have transferred equity to successors, and just 6% of those planning to retire within 10 years have a fully documented succession plan.

At the time of taking over their portfolios under our advisory, we do a portfolio audit to understand their current portfolio structure and what changes need to be done to align the investments with their risk profile and market conditions. Usually, equity products offer higher commissions than debt which offer higher commissions than Gold.

It can be a learning experience: Self-investing can help you understand how markets work. You will need to research investments, monitor your portfolio regularly, stay updated on market changes, and do your taxes correctly. They adjust your asset allocation based on your needs and market movements. 6. No problem!

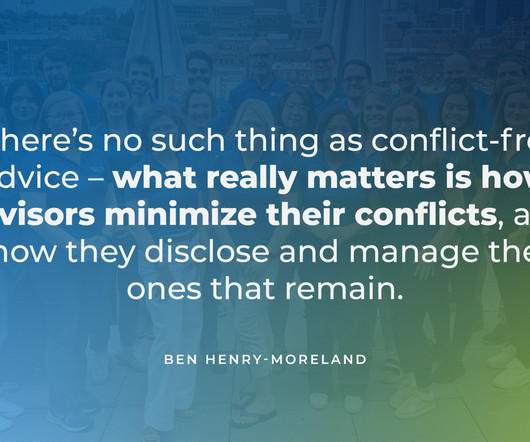

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the SEC this week fined 4 RIAs for violations of its marketing rule related to their claims that they offered 'conflict-free' financial advice.

From advisors who earn commissions from the sales of financial products to fee-only investment advisors who charge based on client assets under management, the value advisors provide to their clients has often been centered on investment management. Read More.

From advisors who earn commissions from the sales of financial products to fee-only investment advisors who charge based on client assets under management, the value advisors provide to their clients has often been centered on investment management. Read More.

In addition, related research suggests further opportunities for firms looking to acquire and retain talent, from providing a greater sense of autonomy to building effective service teams.

In this episode, we talk in-depth about how after working for years in the financial industry, Amy realized there was a missed opportunity in working with career-driven Gen X women like her and decided to focus on serving that type of clientele she knew so well, how the initial fear of launching a firm on her own initially led Amy to partner with another (..)

But it’s the data that drives how changing business strategies impact our understanding of market behavior. From “ The Relentless Bid ” comes the first explanation that resonates as to how and why the market’s character changed so much in the 2010s: “Morgan Stanley wealth management took in a massive $51.9

We met a prospective client a few days ago and enlightened him about our 0% commission, conflict-free advisory model. The bank (and many wealth management firms) earns commissions when investors buy its products. We explained how commissions create a conflict of interest.

I am an irreverent and fun marketing consultant for financial advisors. Fee-only advisor – This is an advisor that does not charge commissions and hence is believed to be more aligned with the client’s best interests. Fee-only advisors are bound to the fiduciary standard. So please subscribe!

Below are the different types of financial advisors you can choose from based on their fee model: 1. Fee-only financial advisors Average cost: $200 to $400 an hour/ $1,000 to $3,000 per plan/ 1.18% to 0.59% of AUM Fee-only financial advisors are professionals who do not receive commissions from selling financial products.

You get access to financial expertise and knowledge on investments and money management, a deeper understanding of how markets work, and how to create and deploy the right investment strategies to attain your goals. It may also be the case that the advisor pushes a particular investment in the hopes of earning a commission.

This is really none of my business, but I can’t help saying that I hate the new policy at the National Association of Personal Financial Advisors regarding trail commissions. We will have to cheapen the hard, strong language that we’re accustomed to using when we recommend working with a fee-only planner.

There are two types of Financial Advisors in India – Fee-Only Advisors and CommissionOnly Advisors. Fee-only advisors need to be registered with SEBI certified financial advisors (Securities and Exchange Board of India) as an RIA (Registered Investment Advisor). CFP ( Certified Financial Planner ).

This is because you have been failing to plan your funds because of less time, following the old ways, peer pressure, less understanding of the financial markets, and so on. They may charge for their services either on a commission basis or hourly rates. We know that financial advisors can work on a commission or fee basis.

They are paid a commission by their underlying broker/dealer or insurance company when a customer purchases a product, such as a mutual fund, annuity or life insurance policy. . The commission is not paid directly by the consumer. Financial advisors who only charge fees might categorize themselves as “fee-only.”

Brokers are paid by a commission on the investment products they sell. Fiduciary advisors are generally fee-only. In this structure, they charge a specific fee for the work they provide, untethered to any products or investment options they recommend. They must always put clients’ interests above their own. .

My client’s estate planning attorney said they should hire a fee-only advisor to manage their assets, and then they asked me if I charge fees or commissions. As a fiduciary, I charge 1% of your assets, and do not accept commissions.” That’s the only way they’ll know your shoe size.

I am a CFA® charterholder and financial advisor marketing consultant. I am an irreverent and fun marketing consultant for financial advisors. He asked for help and found a support community Right now Thomas is a fee-only fiduciary financial advisor. Own one channel and one form of marketing. And now onto the blog!

Generally, financial advisors charge a flat fee based on the services offered and the duration of the engagement, such as $xx for a month/ quarter/ year. They may also charge an hourly rate for every meeting you have or a commission for the financial instruments they recommend. Can you negotiate fees with your financial advisor?

Without periodic rebalancing, your investment mix will change as the market fluctuates, falling out of alignment with your target investment mix. If the stock market were to suffer a decline, the unbalanced portfolio would be exposed to much more risk than intended. Why does this matter? Both can add up and reduce returns.

Fee-only vs. fee-based. But… Fee for service (and onlyfee for service) is a haven where the sales agenda mimicry cannot follow. The industry is then tasked to create a financial advisor fee model that focuses on advice. Providing financial plans vs. canned financial plans with a sales agenda.

For millennials saving for retirement, time is on their side when it comes to making money with long-term investments in the stock market. Born in the early 80s through the mid-90s, this generation can weather market volatility better than investors closer to retirement. Sure, the U.S. The expense ratios are.09% 09% for ITOT and.03%

I said that brokers and sales agents are essentially predators, wolves in sheep’s clothing, where the sheep are fiduciary advisors, and the clothing is, well, you know what it is: ‘fee-based’ and ‘best interest’ (instead of fee-only and fiduciary).

I am a CFA® charterholder and financial advisor marketing consultant. I am an irreverent and fun marketing consultant for financial advisors. The word “fiduciary” is not a marketing term, not just something you throw out there to virtue signal. Commissions are opaque. This is where the confusion comes in.

Then came Reg BI, in 2019, where the Commission decided that adopting a separate rule restricting these terms was ‘unnecessary.’. 202(a)(11)(c) of the Advisers Act,” the petition says, “the Commission can increase investor protection by (re-)asserting a distinction between product sales and stand-alone investment advice.”.

According to the Federal Trade Commission (FTC), in 2021, American consumers lost over $5.8 Ask about the investment, returns, company backing, market experience, product features, specifications, and other details. You can check the company’s financial statement on the Securities Exchange Commission (SEC) EDGAR filing platform.

Instead, he got his first job at a feeonly RIA firm instead which worked out brilliantly for him! So stop thinking that a commissioned sales role is the only way you can become a financial advisor! For those of you who are new to my blog/podcast, my name is Sara. How to become a financial advisor.

The power of compounding invests your profits earned back into the market to earn a higher reward. You have a higher risk appetite: There are different types of investment options in the market. Financial advisors can be hired on fee-only or commission-based models.

The power of compounding invests your profits earned back into the market to earn a higher reward. You have a higher risk appetite: There are different types of investment options in the market. Financial advisors can be hired on fee-only or commission-based models.

Rostad is currently focused on what he sees as our best chance for meaningful reform: getting the Commission to revise the Form CRS disclosure so that it provides a clearer explanation of the different business models of broker-dealers/wirehouses, on the one hand, and fiduciary RIAs registered with the SEC on the other.

I am a CFA® charterholder and financial advisor marketing consultant. I am an irreverent and fun marketing consultant for financial advisors. ” As an hourly financial advisor he doesn’t make commissions for recommending products such as private REITs, structured products, etc. So please subscribe!

I am a CFA® charterholder and financial advisor marketing consultant. I am an irreverent and fun marketing consultant for financial advisors. Feeonly advisors can now purchase annuities for their clients without having to be licensed agents. Are commissions bad? So please subscribe!

I am a CFA® charterholder and financial advisor marketing consultant. I am an irreverent and fun marketing consultant for financial advisors. The invest it in call options to see if they can catch some market upside. If the market goes down, they don’t care – that’s on you. Remember the insurance policy has costs.

I am a CFA® charterholder and financial advisor marketing consultant. I am an irreverent and fun marketing consultant for financial advisors. He’s active, actively market himself as a CFP, has no discipline. For those of you who are new to my blog, my name is Sara. Get ready for a rumble, folks!

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content