This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Retirement has long been associated with leisure, relaxation, and winding down from a long career. In this guest post, Kathleen Rehl, a "ReFired" financial advisor and educator in legacy planning, shares a framework to help advisors guide clients through this transition using a more expansive "ReFirement" lens.

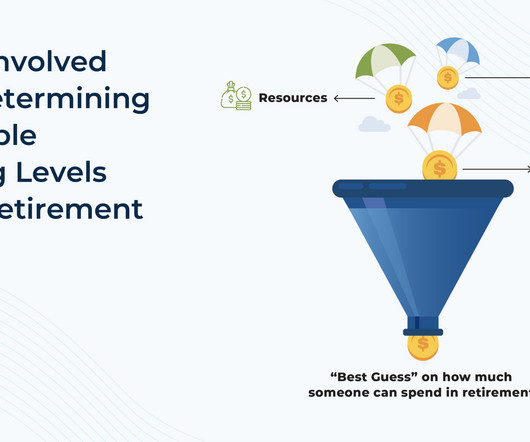

"How much can I spend in retirement?" is perhaps the most fundamental question a client brings to their advisor. Advisors want to help clients set a secure, reliable retirement plan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree.

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives.

These services may range from 'standard' offerings like retirement planning to less traditional areas like credit card consulting. In a firm's early years, there tends to be more room for experimentation, with advisors adding new services to provide value and attract clients.

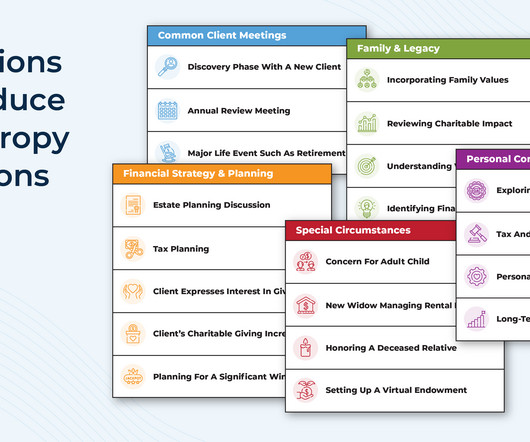

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it. while also setting the tone for a long-term planning relationship built on trust and deeper client engagement.

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it. while also setting the tone for a long-term planning relationship built on trust and deeper client engagement.

Yet, despite the important role that charitable giving can play, studies show that many advisors hesitate to bring up the topic with clients. Advisors may worry about overstepping boundaries or feel uncertain about a client's interest in philanthropy. These statements often stem from clients' life stories and core values.,

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risk tolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financial planning.

Travis is the founder of Student Loan Planner, an RIA and student loan consulting company based in Chapel Hill, North Carolina that serves nearly 1,400 households with ongoing financial planning (as well as consulting with over 15,000 clients on student loan debt).

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent report finds that the number of SEC-registered RIAs, the assets that they manage, and the number of clients they serve all increased between 2023 and 2024 and suggests the industry is robust across the size spectrum, (..)

Over the past decade, a growing number of advisors have expanded into offering comprehensive financial planning services, reflecting a shift that not only helps them stand out from (increasingly commoditized) portfolio management offerings but also supports clients' broader financial goals.

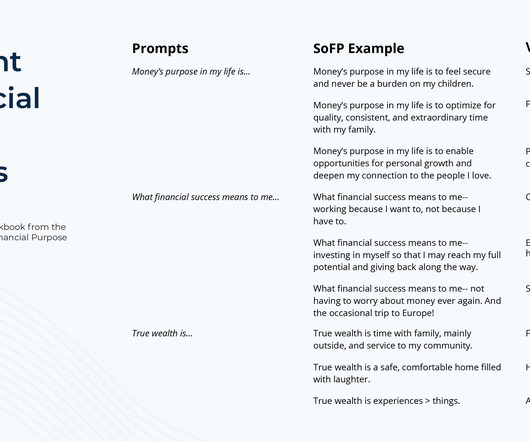

For many financial advisors, an early planning conversation often includes asking clients to identify financial goals. Which can leave both client and advisor feeling stuck: The client doesn't have the motivation to act, and the advisor struggles to guide the plan forward in a way that connects.

Which could prove to be a boon for the financial advice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?). Read More.

RIAs can create a potential client stream if they commit to a 401(k) channel that includes participant education and touchpoints, said panelists at Wealth Management EDGE last week.

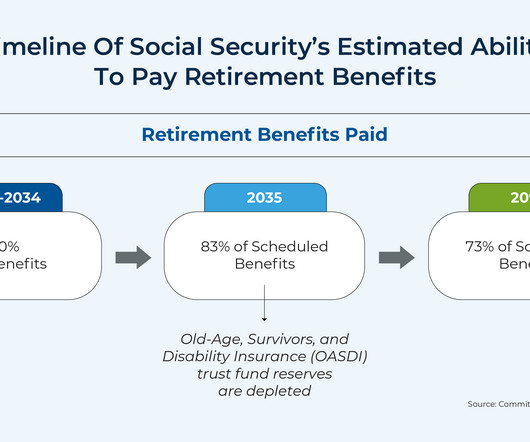

While it may take a while for the adjustments to take place, advisors can still help their clients plan for the effect of WEP and GPO's repeal by estimating how much the client will be receiving in Social Security benefits once the new law is implemented. will be top of mind for clients affected by the WEP and GPO. Read More.

artofmanliness.com) Ben Carlson talks about the state of the retirement savings market with Shawn O'Brien, Director of Retirement at Cerulli Associates. citywire.com) What's behind the surge in client churn at RIAs? advisorperspectives.com) Does risk tolerance change in retirement?

Further, amidst grumbling from some firms, incoming CEO Rick Wurster reiterated a pledge that Schwab (which offers its own direct wealth management services) will not seek to compete for clients with RIAs on its platform, seeing opportunities to pursue prospective clients currently unserved by either group.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that at a time when brokerage firms' cash sweep programs come under increased scrutiny (and as the Federal Reserve has cut interest rates), Charles Schwab (the largest RIA custodian) continues to slash sweep rates for client (..)

Some prospects approach an advisor with an immediate 'problem to be solved', such as a fast-approaching retirement date. I help clients in retirement by doing X, Y, and Z."). These situations often narrow the focus of the prospecting conversation, giving the advisor a clear opportunity to affirm their value (e.g., "I

Notably, the survey identified differences in workplace flexibility by role (with client-facing advisors working more days per week in the office) and by experience (with newer firm employees more likely to have more in-office days each week).

This lack of clarity made retirement planning significantly more challenging. As a result, it's important for advisors to first identify which clients are currently subject to WEP or GPO and ensure that those who may need to file for benefits do so as soon as possible. Read More.

In this environment, financial advisors have the opportunity to add value for their clients not only by giving a clear explanation about the current status of Social Security and the potential legislative changes that could improve its solvency, but also by modeling what (realistic) changes would mean for their clients' financial plans.

Which suggests that, amidst ongoing debate over fiduciary-related regulations, an advisor's status as a fiduciary could both lead to greater client trust (both in their individual advisor relationship and perhaps in the financial advice industry as a whole) and, ultimately, higher client retention rates.

These results largely match results from the recent Kitces Research Study on Advisor Productivity, which found that the typical fee schedule for firms charging on a graduated basis remains at 100 basis points (bps) for client assets up to $1 million, then declines to 90 bps at $2 million, 75 bps at $5 million, and 60 bps at $10 million in assets.

The report suggests this might be due in part to increased RIA valuations and the assumption of some firm founders that next-generation employees won't be financially able to buy out the firm from them, though additional data indicates that many firms don't have career paths in place that could help next-generation advisors envision their path to firm (..)

Over the past few decades, advicers have used Monte Carlo analysis tools to communicate to clients if their assets and planned level of spending were sufficient for them to realize their goals while (critically) not running out of money in retirement.

Accumulation-phase planning software won't cut it for solving your clients' complex retirement income puzzles, but there are dedicated applications that can.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with a recent survey indicating that a majority of advisors are viewing new client acquisition as their primary challenge in the current competitive environment for financial advice (followed by compliance and technology management) and suggests (..)

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirement planning.

Mann, MBA, CFP I find that so many of my clients, regardless of income, have no idea how much money they are saving. First, I would ask clients how much they were saving each year for retirement. Then I would present the plan to the client. Early in my career, this created quite the challenge in developing a proper plan.

Kevin is the CEO of Connecticut Wealth Management, an RIA based in Farmington, Connecticut, that oversees approximately $4 billion in assets under management for 1,100 client households.

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Also in industry news this week: While RIA M&A deal flow hit record levels in 2024 (both in terms of volume and the speed of completing them), firm valuations saw relatively modest gains In its latest annual regulatory oversight report, FINRA joined the SEC in flagging the potential risks to firm and client data from the use of third-party vendors (..)

Michelle is the Founding Principal of Paradigm Advisors, an RIA based in Dallas, Texas, that oversees approximately $110 million in assets under management for 80 client households.

Gideon is the CEO of Drucker Wealth, a hybrid advisory firm based in New York City, that oversees approximately $1 billion in assets under management for 800 client households.

Daniel is the CEO of WMGNA, a hybrid advisory firm based in Farmington, Connecticut, that oversees approximately $270 million in assets under management for 200 client households.

Jennifer is the CEO of The Mather Group, an RIA based in Chicago, Illinois, that oversees $15 billion in combined assets under management and advisement for approximately 4,400 client households. Read More.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content