This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While state and Federal regulations clearly outline recordkeeping requirements for areas like financials, advertisements, and trading records, there is a notable gap when it comes to documenting the delivery of services – especially financialplanning services – necessary to justify the fees charged for those services.

Just a few decades ago, giving financial advice was largely a manual process – printing lengthy financialplans, processing physical checks, and managing paper files. Many client concerns are deeply personal, requiring empathy, trust, and a nuanced understanding of complex emotional and financial situations.

Over the past decade, a growing number of advisors have expanded into offering comprehensive financialplanning services, reflecting a shift that not only helps them stand out from (increasingly commoditized) portfolio management offerings but also supports clients' broader financial goals.

Young advisors may feel – and face – an extra burden to prove their expertise to clients. After all, it can feel odd to create an estate plan that will impact a client’s grandchildren… when those grandchildren may be older than the advisor themselves!

Travis is the founder of Student Loan Planner, an RIA and student loan consulting company based in Chapel Hill, North Carolina that serves nearly 1,400 households with ongoing financialplanning (as well as consulting with over 15,000 clients on student loan debt).

Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning. They also suggest how advisors with unsustainably low fees can shift their mindset, embrace their value, and realign their pricing to reflect both the tangible and intangible value they actually provide to clients.

Mason received a 97-month prison sentence for defrauding clients of over $17 million. Mason, a former advisor who was barred from the industry, was sentenced to 97 months in prison and three years of supervised release for defrauding at least 13 advisory clients out of more than $17 million, according to the Department of Justice.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risk tolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financialplanning.

Anjali is the Founder of FIT Advisors, an RIA based in Torrance, California (but works virtually with clients nationwide) and oversees $65 million in assets under management for 45 client households.

Katie Greifeld July 2, 2025 2 Min Read Bloomberg photo (Bloomberg) -- Vanguard Group is planning its debut into an increasingly competitive corner of the $11.6 trillion US exchange-traded fund arena.

While many firms have historically relied on commission-based compensation methods – reflecting a sales-driven approach – financial advice has evolved with technological advancements and a greater focus on financialplanning, with the Assets Under Management (AUM) fee emerging as the primary compensation model.

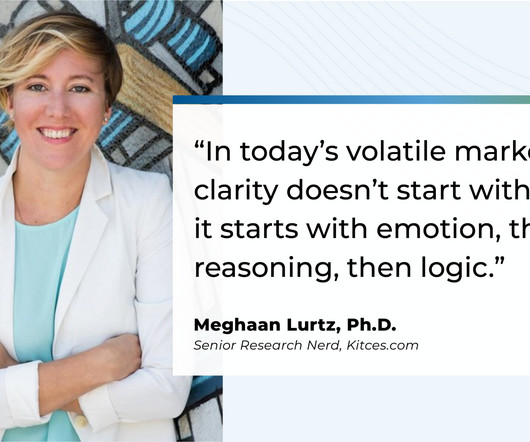

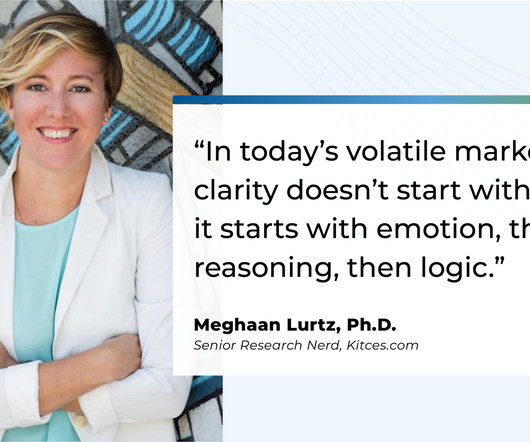

During periods of market volatility, it's common for financial advisors to receive calls from clients who are nervous about what a steep market decline might mean for their portfolio and long-term financial goals. But even when a client agrees with the reasoning in the moment, the anxiety often lingers.

During periods of market volatility, it's common for financial advisors to receive calls from clients who are nervous about what a steep market decline might mean for their portfolio and long-term financial goals. But even when a client agrees with the reasoning in the moment, the anxiety often lingers.

is perhaps the most fundamental question a client brings to their advisor. Advisors want to help clients set a secure, reliable retirement plan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree. "How much can I spend in retirement?"

Sebastian is the President of Guerra Wealth Advisors, a hybrid advisory firm based in Miami, Florida, with nearly $15M of revenue and almost 60 team members, supporting over 1,700 client households.

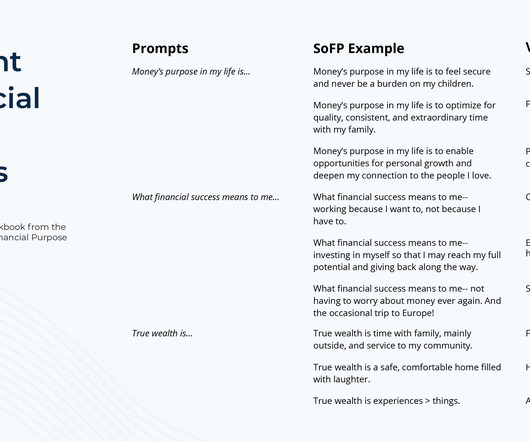

Yet, despite the important role that charitable giving can play, studies show that many advisors hesitate to bring up the topic with clients. Advisors may worry about overstepping boundaries or feel uncertain about a client's interest in philanthropy. These statements often stem from clients' life stories and core values.,

The former TDAI and Altruist executive has been in stealth mode building Wing, a digital financialplanning app meant to help next-gen clients build personalized, goals-based plans, and advisors capture money in motion.

There's an old joke in the financialplanning industry that the ideal client is "anyone with a pulse". However, as their firms mature, advisors often notice a divide manifesting between newer clients paying higher fees and 'legacy clients' from the early days paying discounted rates.

Seth is the founder of Heartwood FinancialPlanning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households. My guest on today's podcast is Seth Scott.

For many financial advisors, an early planning conversation often includes asking clients to identify financial goals. Which can leave both client and advisor feeling stuck: The client doesn't have the motivation to act, and the advisor struggles to guide the plan forward in a way that connects.

In these moments, the conversations that advisors have with their clients play a crucial role in helping clients maintain perspective, avoid emotional decisions, and stay committed to their long-term financialplans. Using mirroring language (e.g., Read More.

Michelle is the Founding Principal of Paradigm Advisors, an RIA based in Dallas, Texas, that oversees approximately $110 million in assets under management for 80 client households.

But as more individuals confront the emotional realities of this life transition, many find that the absence of structure, socialization, and identity once provided by work can create a gap that traditional retirement planning doesn't fully address. While the core elements of traditional retirement planning remain (e.g.,

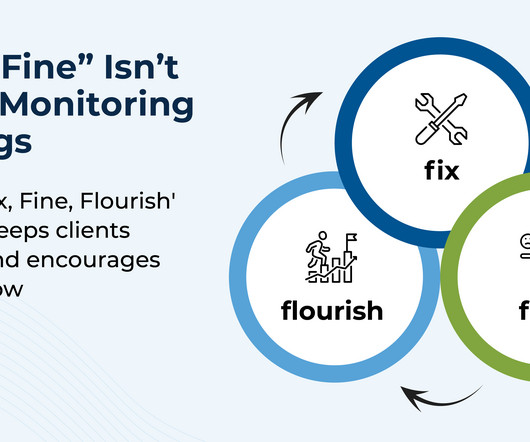

When a client first begins working with an advisor, the relationship is often marked with a flurry of onboarding tasks, immediate issues to resolve, and long-term planning goals to establish. And as clients come into monitoring meetings, they may increasingly describe their situation as "fine", with no pressing issues to address.

Nina is a partner of Stratos CA, a hybrid advisory firm affiliated with Stratos Wealth Partners and based in Los Angeles, California, that oversees approximately $500 million in assets under management for 300 client households.

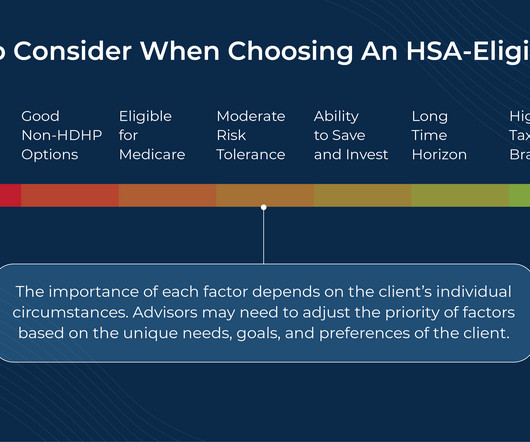

Health Savings Accounts (HSAs) have become an increasingly popular tool for financial advisors and their clients due in part to the 'triple tax savings' they offer: tax-deductible contributions, tax-free growth, and non-taxable distributions for qualifying expenses.

that generates $850,000 of annual, primarily retainer-based, revenue serving 155 client households. What's unique about Alvin, though, is how he has grown his firm by using project management software Monday.com as a central hub for financialplan presentations and efficient client task management.

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirement planning, estate and tax planning and mortgage refinancing. They also make up the second biggest client base for financial advisors after baby boomers. trillion annually.

I help clients in retirement by doing X, Y, and Z."). However, not all prospects have immediate financial concerns. While these individuals may genuinely be interested in financial advice, they might also feel ambivalent about the timing, relevance, or ultimate value of working with an advisor.

In the early days of financialplanning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirement planning.

Many financial advisory clients might work for 40 years or more, ideally seeing their income – and capacity to save for retirement – increase over time as they advance in their careers. Still others, including adherents of the Financial Independence Retire Early (FIRE) movement, may hope to retire even sooner.

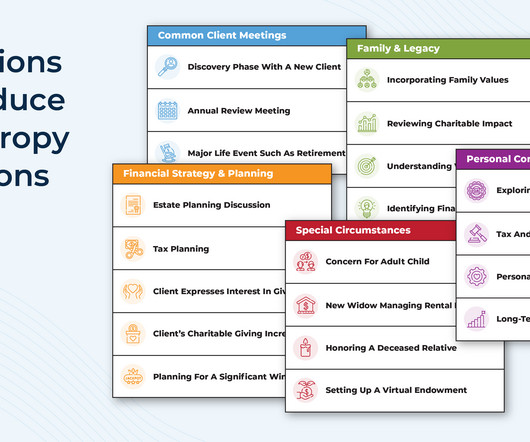

Financialplanning meetings often fall into categories like "Fix Meetings" (where there is an urgent problem that both the advisor and client want to address), 'Fine Meetings' (where everything is on track and the advisor provides reinforcement), or 'Flourish Meetings' (where clients are thriving and the focus is on expanding possibilities).

Cristina is the CEO of Mana Financial Life Design, an RIA based in Los Angeles, California (but works virtually with clients nationwide), that oversees approximately $70 million in assets under management for 119 client households.

RWM works with clients by constructing a long-term financialplan, marrying it to an appropriate level of risk in a broadly diversified portfolio built around a core index, and then applying the best technology we can find to generate net after-tax returns with modest risk and volatility.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that Congress has passed highly anticipated tax legislation, making 'permanent' (i.e.,

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent report finds that the number of SEC-registered RIAs, the assets that they manage, and the number of clients they serve all increased between 2023 and 2024 and suggests the industry is robust across the size spectrum, (..)

Advisors have a relatively brief window of time to communicate their value to prospective clients. Given how little time prospects spend evaluating their options, it's crucial to understand why people hire financial advisors and to communicate how their services address those drivers as clearly and effectively as possible. Read More.

In fact, they may be the missing piece in your clients’ portfolios—and AssetMark is betting big on that future. Michael joined AssetMark in 2010 and has held a number of leadership positions, including Head of National Sales and Consulting, Chief Client Officer, and President (2021–Present).

When a financial advisory firm owner first starts their business, much of their time is spent on finding clients that they can serve. But as they (hopefully) onboard more clients and get busier with servicing those clients, they will also find that they eventually start to run short on time.

(citywire.com) What's behind the surge in client churn at RIAs? riabiz.com) Risk tolerance Determining a client's risk tolerance is more complicated than having them fill out a questionnaire. advisorperspectives.com) Advisers A plan for onboarding client service associates. signaturefd-3437664.hs-sites.com)

billion in client assets to its independent advisor channel. group, led by Jak Cukaj, Neal Siena, Charles Camilleri and Brigitte Davison, join from Ameriprise Financial, and will establish three separate practices. They’re joined by advisors Adam Sloane and William Longing and client service managers Elissa Levy and Maura Fronio.

Eric is the Chief Financial Advisor and Co-Owner of Econologics Financial Advisors, an independent RIA based in Largo, Florida, that generates more than $4M of revenue while working with nearly 300 client households.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content