This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mason received a 97-month prison sentence for defrauding clients of over $17 million. Mason, a former advisor who was barred from the industry, was sentenced to 97 months in prison and three years of supervised release for defrauding at least 13 advisory clients out of more than $17 million, according to the Department of Justice.

Financial advisors should prioritize charitable giving discussions to meet growing client interest and strengthen relationships with younger generations.

In a firm's early years, there tends to be more room for experimentation, with advisors adding new services to provide value and attract clients. The best roadmap for focusing an advisory firm will reflect how to do more of what clients value and scale back on what they don't use or appreciate.

There's an old joke in the financial planning industry that the ideal client is "anyone with a pulse". However, as their firms mature, advisors often notice a divide manifesting between newer clients paying higher fees and 'legacy clients' from the early days paying discounted rates. take a physical and emotional toll.

Yet true efficiency is achieved by delivering real value to clients, not merely by upgraded systems. Without a clear approach, no level of automation can overcome the complexities of serving every client’s needs. 🌎 Understand your offering’s role in the client’s success, creating lasting value. Register now!

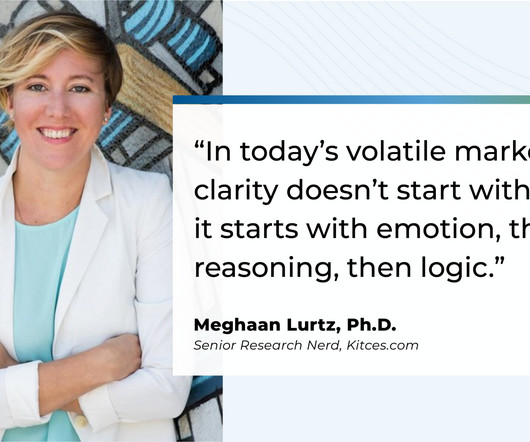

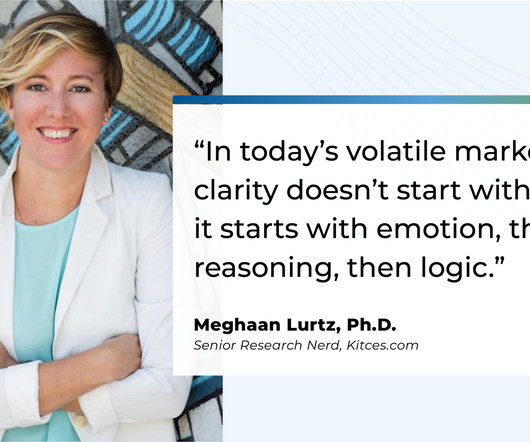

During periods of market volatility, it's common for financial advisors to receive calls from clients who are nervous about what a steep market decline might mean for their portfolio and long-term financial goals. But even when a client agrees with the reasoning in the moment, the anxiety often lingers.

During periods of market volatility, it's common for financial advisors to receive calls from clients who are nervous about what a steep market decline might mean for their portfolio and long-term financial goals. But even when a client agrees with the reasoning in the moment, the anxiety often lingers.

This fee confidence gap has large ramifications in the long term, as firms with higher revenues can reinvest in growth – with hiring, marketing, and process improvements – that enhance their value proposition and attracts more prospective clients. Have clients described the advice as "life-changing"? Read More.

When a financial advisor transitions from one firm to another, they're often offered incentives by the new firm based on how much client revenue they bring with them. The challenge, however, is that advisors generally don't have the legal authority to simply transfer clients to a new firm.

Lynnette Khalfani-Cox, The Money Coach®, will answer these questions and more – giving you insights into the consumer mindset along with proven strategies for nurturing trust and client- building in underserved markets. February 21, 2023 at 9:30 am PST, 12:30 pm EST, 5:30 pm GMT

Yet, despite the important role that charitable giving can play, studies show that many advisors hesitate to bring up the topic with clients. Advisors may worry about overstepping boundaries or feel uncertain about a client's interest in philanthropy. These statements often stem from clients' life stories and core values.,

Anjali is the Founder of FIT Advisors, an RIA based in Torrance, California (but works virtually with clients nationwide) and oversees $65 million in assets under management for 45 client households.

Early in a firm's life cycle, a founder might take on nearly any client (and their fees) just to generate enough revenue to 'keep the lights on'. However, as the firm grows, some of those early clients may no longer be profitable to serve – especially if they generate lower fees than newly onboarded clients.

Travis is the founder of Student Loan Planner, an RIA and student loan consulting company based in Chapel Hill, North Carolina that serves nearly 1,400 households with ongoing financial planning (as well as consulting with over 15,000 clients on student loan debt).

What if your role as a fractional CFO went beyond operational support to actively shaping the future of your clients’ businesses? Join Ashley Harlan, CFO and financial strategist, to learn: 📈 Proven methods to prepare clients for long-term financial leadership transitions. Ready to lead with impact? Register today!

Pete is the Director of Sustainable Investing of Earth Equity Advisors, an RIA based in Asheville, North Carolina, that oversees approximately $200 million in assets under management for 250 client households. Read More.

Nina is a partner of Stratos CA, a hybrid advisory firm affiliated with Stratos Wealth Partners and based in Los Angeles, California, that oversees approximately $500 million in assets under management for 300 client households.

In these moments, the conversations that advisors have with their clients play a crucial role in helping clients maintain perspective, avoid emotional decisions, and stay committed to their long-term financial plans. Instead, allowing them to fully voice their fears can build trust and help them feel understood. Read More.

Speaker: Rita Keller - President of Keller Advisors, LLC

You're known as the “go-to” person when a client is faced with tax and financial decisions. You've worked diligently and have built a glowing reputation grounded in your excellent skills in tax, accounting, and auditing. You have a very successful firm -- but that’s not enough.

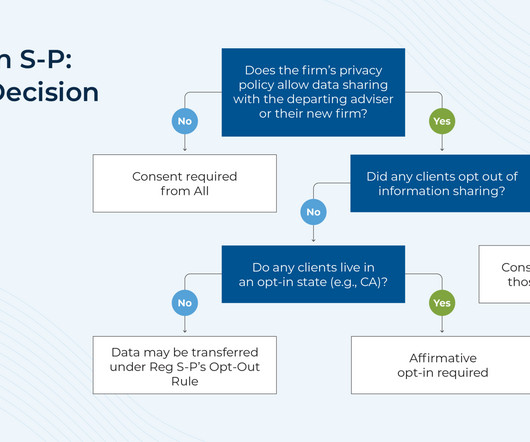

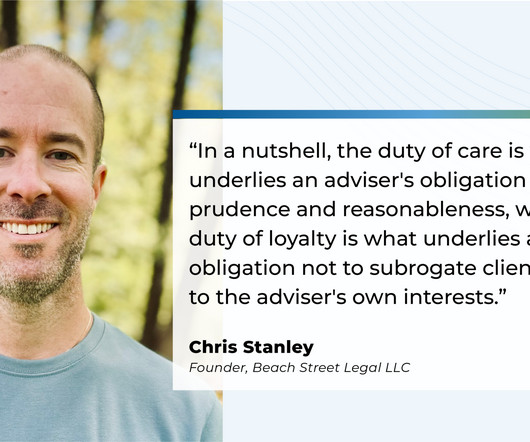

Investment advisers are fiduciaries that owe a duty of care and loyalty to their clients. One component of this duty of care is an obligation to seek best execution of client securities transactions. The SEC, in its interpretive release, sets an expectation of "periodic and systematic evaluation" (i.e.,

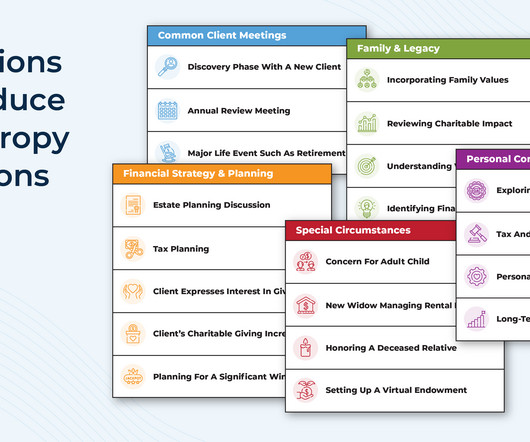

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risk tolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financial planning.

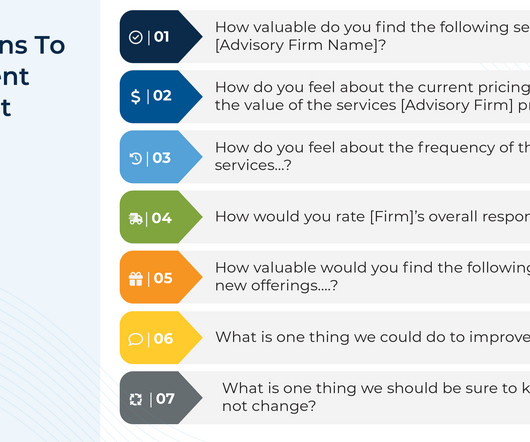

Whether you're refining your client acquisition strategy or scaling your practice, this report gives you the real-world data, benchmarks, and action steps to lead the way. Download your free copy today — and turn insights into your competitive edge.

New financial advisors often start with below-market fees – sometimes to build confidence that prospects will actually pay, other times to attract clients quickly and establish a base. And while new clients often come in at higher fees, early clients may still be paying well below the firm's current rates.

Fun conversation in Barron’s about Steering Clients Away From Bad Investing Mistakes. Source : How Next-Generation Advisors Steer Clients Away From Bad Investing Mistakes A key role of a financial advisor is to prevent clients from making rash decisions during volatile markets. billion in assets under management.

For many financial advisors, an early planning conversation often includes asking clients to identify financial goals. Which can leave both client and advisor feeling stuck: The client doesn't have the motivation to act, and the advisor struggles to guide the plan forward in a way that connects.

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives.

Speaker: Wayne Spivak, President and CFO of SBA * Consulting Ltd., Industry Writer, Public Speaker

And while this may sound like great news for you and your clients, it won’t be worthwhile unless you have the latest techniques to back up your ambitions! With the advancement of technology, the implementation of spend management best practices and concrete GAP analyses is more streamlined and accessible than ever before.

In recent years, financial advice has expanded beyond spreadsheets and technical strategies to consider the behavioral and emotional factors driving clients’ relationships with money. At the same time, advisors’ personal money stories may serve as a magnet for like-minded clients – and an asset to the relationship.

When a client first begins working with an advisor, the relationship is often marked with a flurry of onboarding tasks, immediate issues to resolve, and long-term planning goals to establish. And as clients come into monitoring meetings, they may increasingly describe their situation as "fine", with no pressing issues to address.

In this guest post, Kathleen Rehl, a "ReFired" financial advisor and educator in legacy planning, shares a framework to help advisors guide clients through this transition using a more expansive "ReFirement" lens. Yet even clients who are financially prepared may feel anxious or uncertain about what comes next. Read More.

As a result, when advisors are tasked with (re-)educating clients about the potential consequences of financial decisions, there may be a disconnect between potential risk and what a client actually experiences. So how can advisors help clients understand dangers they haven't personally encountered?

Many financial advisory clients might work for 40 years or more, ideally seeing their income – and capacity to save for retirement – increase over time as they advance in their careers. But not every client may want to leave the workforce early.

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it. while also setting the tone for a long-term planning relationship built on trust and deeper client engagement.

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it. while also setting the tone for a long-term planning relationship built on trust and deeper client engagement.

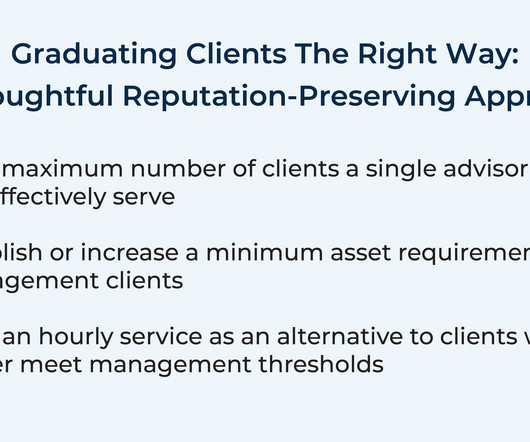

For the RIA industry to shed the “eat what you kill” label by the next generation, they must “break resistance” to passing on clients, according to panelists speaking at Wealth Management EDGE.

What's unique about Libby, though, is how she has created a system for onboarding clients (based on her experience as a coach and as a financial advisor herself) that demonstrates a firm's professionalism, reduces points of friction, and shows personal touches, that together can drive client referrals after just their first 100 days with the firm.

Advisors spend a lot of time crafting their financial advice recommendations – and how they deliver those recommendations – for their clients. These ultra-personalized suggestions are central to what makes financial advice valuable and can have a significant impact on a client's life. or "How can I be helpful here?"

But delivering those recommendations in a way that clients can understand and act on is a separate skill. Because when advice is clear and comprehensible, clients are more likely to act on it and gain peace of mind from knowing there's a well-considered strategy in place! Fortunately, advisors don't need to start from scratch.

billion in assets under management for 1,800 client households. David is the founder of The Bahnsen Group, an RIA based in Newport Beach, California, that oversees approximately $7.5

Sebastian is the President of Guerra Wealth Advisors, a hybrid advisory firm based in Miami, Florida, with nearly $15M of revenue and almost 60 team members, supporting over 1,700 client households.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content