This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Historically, this bracket has been dominated by the tech sector, but after years of outsized gains, big tech valuations are stretched. Small & Mid-Cap Region: SOFI Surges in a Changing Market The small and mid-cap asset class has long been overshadowed by large-cap dominance, with the past decade favoring mega-cap technology stocks.

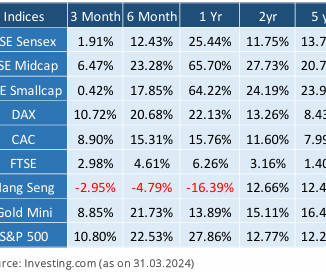

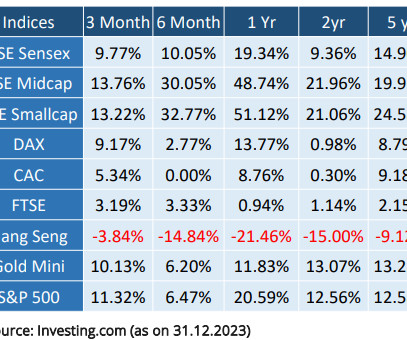

Indian equity benchmark BSE Sensex went up by only 2% due to already stretched equity valuations. Mid & small cap indices witnessed some correction after the SEBI expressed concerns regarding frothy valuations and nudged mutual funds to restrict inflows. European indices also saw decent returns.

You get a bachelor’s in economics from Colgate and then an MBA in finance from NYU Stern. I was an economics and English major. We learned everything, you know, across from accounting to auditing to, to tax and valuation. It seemed like the perfect match of asset and liabilities until real estate valuations bottomed out.

In the world of market valuation metrics, few have gained as much prominence as the Shiller P/E Ratio, also known as the Cyclically Adjusted P/E (CAPE) Ratio. Made famous during the late 1990s tech bubble, this metric continues to be a valuable tool for investors seeking to understand market valuations and potential future returns.

Several factors were common between the two markets: robust corporate earnings growth, expected cuts in interest rates and a shift in investor expectations from a valuation-led phase to an earnings-led phase. We continue to hold 7-10% exposure to Southeast Asian markets due to attractive valuations and improving growth prospects.

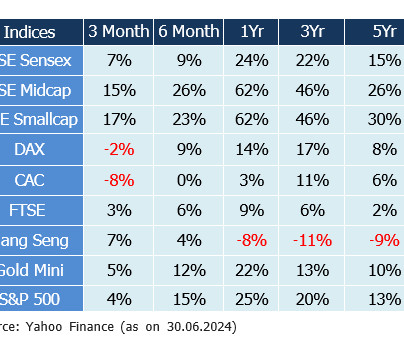

All the sectors went up with major sectoral growth seen in auto (up 22%), realty (up 33%), and consumer durables (up 13%) on the back of an improving economic outlook. The recent rally in the market has made the valuations more expensive compared to historical standards. Valuations across all sectors do not offer any margin of safety.

If we’re going to print money to protect the value of our currency then we should be strategically investing that money in endeavors that create real resources or are accretive to economic value in the future. No other country comes remotely close to competing with the US dominance in global market valuations.

The quantum of money printing jumped massively after Corona-led economic shutdowns. The liquidity support since 2008 and massive stimulus post March 2020 has inflated all the asset prices be it equity, debt, or real estate. US Fed increased its balance sheet size from ~$4-4.5 trillion to ~$8-8.5 trillion in a span of just 2 years.

September 2016 Insights on Markets and Investments achen Mon, 09/12/2016 - 01:00 In this issue: Investors Facing Rising Risks Need Solid Defense, Savvy Offense Increasing political and economic risk during the past year has widened the range of possible positive and negative scenarios for financial markets.

In this issue: Investors Facing Rising Risks Need Solid Defense, Savvy Offense Increasing political and economic risk during the past year has widened the range of possible positive and negative scenarios for financial markets. By Taylor Graff, Head of AssetAllocation Research and Ed Chadwyck-Healey, Head of International Private Clients ?

This has resulted in skyrocketing valuations of the stock markets. Nifty currently is trading at a multi-year’s high valuation. Whereas, the complete economic recovery is still far away and uncertain in terms of its timing and structure. Rising number of cases in Europe has been affecting the economic recovery.

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. Recent economic data has pointed to continued growth—giving rise to the “no landing” narrative.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks. Thu, 06/01/2017 - 02:47.

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. As we know from historical precedents, when the Fed aggressively raises rates, economic growth slows or outright contracts, which is the Fed’s goal.

Strong Defense: The Falling Opportunity Cost of Allocating to Bonds ajackson Tue, 07/24/2018 - 09:25 For years, “defense” in portfolios—i.e., allocations to cash and core fixed income holdings—has meant a willingness to accept extremely low returns. Robust Q1 2018 earnings growth improved the valuation picture for U.S.

allocations to cash and core fixed income holdings—has meant a willingness to accept extremely low returns. But after many years of economic recovery, we finally have reached a point where defensive allocations once again provide a reasonable yield. Robust Q1 2018 earnings growth improved the valuation picture for U.S.

Combined with India’s own economic strength and lower interest rates, asset prices—stocks, real estate, gold—could rise even further. The assumption that asset prices will keep rising can quickly be challenged by things like escalating geopolitical tensions, a U.S. What does this mean for India? But so will inflation!

Bad economic news turned out to be good news for stocks. This time around, good economic news meant bad news for stock prices, primarily because the Federal Reserve was slamming the brakes on the economy by increasing the Federal Funds interest rate target. The S&P 500 surged +16.3% (see chart below). What did the stock market do?

Inflation is currently at 40 year highs with increasing signs of slowing economic growth. We’re currently seeing one of the largest disparities in valuations between growth and value stocks which in our opinion presents a very appealing opportunity for dividend seeking investors.

While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Our assetallocation process accounts for a wide range of potential outcomes over the next 18–36 months.

Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains. Reassess assetallocation. Consider changes to portfolio construction. and Germany—have fueled volatility.

There’s also quantitative metrics that we look at Those have evolved, but always within that capa, that cluster of high returns on investment stability across the economic cycle are consistent and strong balance sheets. And actually Ben Inker is the head of our assetallocation group. 00:18:41 [Speaker Changed] Yep.

Contrary to the expectation of an economic slowdown in 2023, the year turned out to be full of surprises, mostly positive ones. Some of the fund managers continued discouraging flows in Mid & Small Cap stocks by either sounding cautious, dropping coverage, or stopping the inflows owing to frothy valuations in the space.

Increased equity exposure in tactical assetallocation from 62% to 65%. Reduced low duration core bond allocation and increased allocation to small cap equities. Although energy prices came down some, weakening economic data and the lack of a cease-fire in Ukraine offset the modest gas price relief.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. At the same time, the resilience of the U.S.

Economic activity does not stop like an airplane eventually does, but rather the economy will settle into a steady state where growth is consistent with factors such as population and productivity. Perhaps that was not the first time market watchers used the term, but the conversations at the Economic Club of New York were prescient.

Lessons learned: Economic forecasts The Fed’s bark was as bad as its bite! economy to avoid recession, and support above-average valuations. The hit to valuations in the form of about 4 P/E points (21 to 17) translates into a roughly 20% drop in the S&P 500 Index. Here are some of our lessons learned from 2022.

Later in the year, markets became anxious about other topics, such as a potential economic slowdown, a new level of dysfunction in Washington (including unusual executive challenges to the Fed's independence and an extended partial government shutdown), and escalating trade disputes between the U.S. equity exposure.

The economic expansion is weak and inflation is still below the central bank’s 2% target. equity market: A comparatively quick interest rate increase counteracts the benefit from stronger economic growth, impairing profitability and valuations. Concern about future economic growth undermines valuations.

Sentiment cycles move from one extreme of greed to another extreme of fear which takes valuations also to extremes from their long-term averages. At the extreme of fear sentiment (which coincides with dirt-cheap valuations), the risk-reward is highly favorable i.e., higher potential upside with lower potential downside risk.

Economic and corporate data support the initial strong reads on holiday retail sales despite the macro headwinds, reinforcing the idea that today’s consumer is in a better position than usual at this point in the business cycle. Any economic forecasts set forth may not develop as predicted and are subject to change.

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

due to expectations of slowing economic growth. The Strategic and Tactical AssetAllocation Committee (STAAC) made no changes to its recommended assetallocation for August. Any economic forecasts set forth may not develop as predicted and are subject to change. We could see a retest of 3.5%

The hangover from COVID has created significant supply chain disruptions and widespread economic shortages. Source: Trading Economics. The rising Baker Hughes drilling rig count below reflects the miracle of supply-demand economics operating in full force. Source: Trading Economics. Source: GasBuddy.com.

In good times i.e. when the market valuations are usually very high, everyone agrees to the logic of buying low and selling high. Not understanding the role & importance of tactical assetallocation (overweight debt in euphoric times and overweight equity in a time of acute pessimism) in creating superior returns over the long term.

Some recent softening in economic data, coupled with signals from the bond market, may be indicating that Fed policymakers’ concerted inflation fight may be closer to the end than the beginning. We should also have slowing corporate earnings growth and greater economic uncertainty to contend with, some formidable seas to navigate.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. From an economic perspective, growth in the U.S. In the U.S.,

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. From an economic perspective, growth in the U.S. Incremental Equity Risks.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

Second, if investors aren’t willing to assign the same valuation to stocks (due to higher interest rates and uncertainty), that also has a negative effect. I for one don’t think so and neither does Burton Malkiel, Princeton Economics professor and author of the classic finance book A Random Walk Down Wall Street.

That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change. Along with the statement, the Committee updated the Summary of Economic Projections (SEP), which is arguably more important than the brief monetary policy statement.

Market strategists and pundits make the relationship between recessions and the stock market seem binary, but each economic contraction is different and has different effects on earnings. First, keep in mind that stocks tend to look forward by four to six months and can provide warnings of changing economic conditions.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content