This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Podcasts & Videos CE Webinars Research Newsletters Subscribe Subscribe News Related Topics RIA IBD Wirehouse RPA Insights & Analysis Regulation & Compliance Career Moves Recent in News See all Marc Schechter RIA Q&A: What Was Behind Schechter’s Decision to Sell to Arax? Number 8860726.

Alex Ortolani , Senior Reporter June 10, 2025 1 Min Read SilverStar President and Lead Principal Tim Hudson Bluespring Wealth Partners, the registered investment advisor acquisition arm of Kestra Holdings , has acquired a former Kestra Advisory Services firm in the Houston metro area to merge with its LifeBridge Financial Group and create a $1.4

We took a pause in the last year to acknowledge that, since our formation in 2019 , we have tripled in size and integrated more than nine firms. Number 8860726. It has been an exciting time. We’ve just passed $30 billion in AUM. We have 375-plus employees and 26 offices as of today. formally launched Wealthspire 2.0 in summer 2024.

But some of those companies will become an IBM, GM, or Kodak perhaps still worthy of investment in the future, but not the dominant player it is today. Thats running at a solid 170,000 per month, versus an average of 166,000 in 2019. million in 2023 but well in the ballpark of what we saw in 2017-2019 (2.1 in 2018-2019.

In 2019, monthly job growth averaged 166,000 but we saw four months with 100,000 or fewer jobs created. The 2017-2019 pace was 3.1%.) Business investment was also strong in Q3, though half of that was from aircraft spending, and that is unlikely to repeat in the next quarter or two.

For reference, the 2019 average was 166,000. 6 million level we saw in 2018-2019. million level we saw in 2018-2019. The risk is that the Fed takes an extended pause, even as rates stay on the higher side and adversely impact cyclical areas of the economy like housing, manufacturing, and business investment.

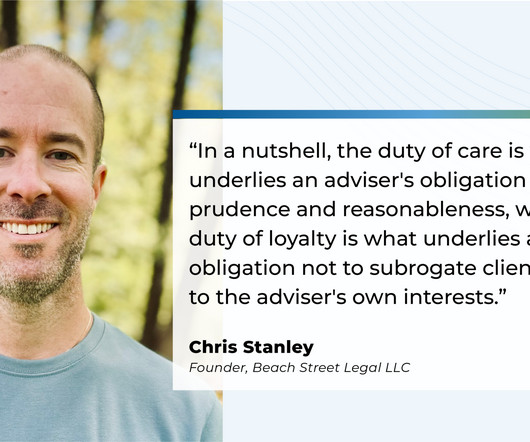

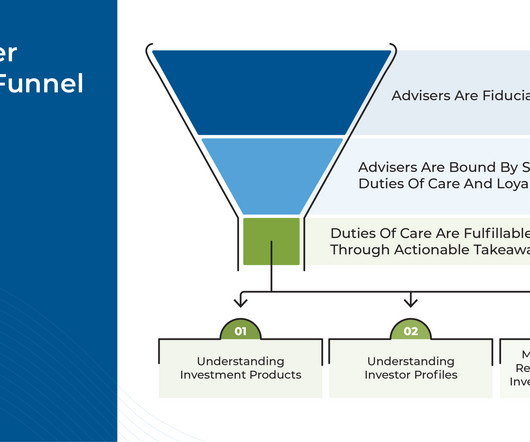

Investment advisers are fiduciaries that owe a duty of care and loyalty to their clients. the types of investment products or strategies that a custodial broker-dealer can handle in an accurate and timely fashion), and commission rates (which can include asset-based pricing, platform fees, account activity fees, and more), among others.

You should never blindly invest in seasonality, but just as February was ripe for potential trouble, be open to a nice Spring bounce. Hopefully because youve been reading this then you know that even the best years have scary headlines and volatility and that volatility is the toll we pay to invest. Panic Is in the Air How do you feel?

Congrats again to the Dow on an amazing run and to all the investors over the years who have benefited by sticking to their investment plans. That’s well below the 209,000 average we saw back in December, and even below the 2019 pace of 166,000. Refinancings are down 65% from average 2019 levels. Any bets on when it breaks 100k?

Still, lets focus on where excess inflation is coming from for CPI and compare the November data to December 2019 (when headline and core CPI were up 2.3% in December 2019. Thats adding 0.52%-points to excess headline CPI relative to December 2019, and 0.65%-points to excess core CPI. y/y versus the 2018-2019 average of 3.7%.

But inventory is still low relative to history—it’s down 12% from average 2019 levels. Housing, or residential investment, makes up just 4% of GDP, but it’s amongst the most cyclical parts of GDP and can drive changes in GDP growth (up or down). It was 101% at the end of 2019, and 137% just before the financial crisis in 2007.

The Carson Investment Research Team put their heads together and chose some of the charts we thought best tell the story of 2024. But when we did, we frequently reinforced that investing based on ones political beliefs tends to be a fundamental mistake when it comes to markets. Here are some of our favorites.

Lets focus on where excess inflation is coming from for CPI and compare the 2024 data to 2019 (when headline and core CPI were up 2.3% in December 2019. Thats adding 0.50-%-points to excess headline CPI relative to December 2019, and 0.62%-points to excess core CPI. y/y versus the 2018-2019 average of 3.6%. Its now up 4.9%

Old investing maxim This is our last market commentary of 2024, and it may be the most important. The foundation of long-term investing success is understanding how markets behave in the long run. Rather than making investing decisions based on valuations, you are better off investing in days that end in y if you ask me.

But these are also times when its easy to make costly investing mistakes. President Trump himself touted the USMCA as a great deal back in 2019 (the USMCA replaced NAFTA). That uncertainty is going to reduce capital investment here in the US. All indices are unmanaged and may not be invested into directly.

No, no one should ever invest purely on the calendar, but March has had some nice lows over the years and as we show below, the past two decades it has been perfectly normal to see late February to early March weakness, but then a nice bounce. As uncomfortable as this recent volatility feels, know that it is the toll we must pay to invest.

This is why we invest for the long run and use the scary times as an opportunity, not a time to panic. For perspective, here are the numbers for 2019: Overall household debt grew by 4.4% of disposable income right now, below the 19802019 average of 12% and even below the 2019 average of 11.7%. Disposable income grew by 2.7%

Back in 2018–2019, payrolls grew at an annualized pace of 1.4%. All said and done, if net immigration pulls back to 500,000, which would be much lower than the 2017–2019 pace (averaging about a million per year then), the economy likely has to create just 60,000–80,000 to keep up with population growth. year over year, down from 1.3%

At the same time, hiring is clearly weak, with the hire rate running close to 2013 levelsby no means terrible, but much lower than it was in 2018-2019 or even 2022-2024. All indices are unmanaged and may not be invested into directly. The good news is that the unemployment rate remains low because layoffs are low.

Trusts Created Martin Griffin died on July 9, 2019, survived by his spouse, Maria Creel. Number 8860726. 2025-47, a Tax Court denied the estate of a Kentucky decedent a marital deduction for a bequest, finding that it wasn’t qualified terminable interest property (QTIP) because a QTIP election wasn’t made.

All else equal, deficit-financed spending will boost profits (as they did in 2016-2019, 2020-2021, and even 2023-2024). All indices are unmanaged and may not be invested into directly. Investors cannot invest directly in indexes. How Big Will the Tax Bill Be?

There is a general understanding that investment advisers have a fiduciary relationship with their clients – in other words, that they are required to act in the client's best interests. These 3 components in practice make up a core part of the adviser's fiduciary duty to their clients.

after adjusting for inflation, matching the average annual pace between 2010 and 2019. Compare that to the 2018-2019 pace of 1.7% The last two months have exceeded the monthly average of $6 billion from 2019. All indices are unmanaged and may not be invested into directly. Through June 2023, the economy grew 2.4%

In 2019, average monthly job growth was 166,000. That’s only slightly below the high from last summer, and above anything we saw between 2001 and 2019 (when it peaked at 80.4%). As a percent of the labor force, this measure is now at 2.6% — matching its level in February 2020 and a tick below the 2019 average of 2.7%.

For perspective, job growth averaged 163,000 a month in 2019. All indices are unmanaged and may not be invested into directly. Compliance Case # 02018534_121123_C The post Market Commentary: Things You Don’t See in a Recession appeared first on Carson Wealth. million this year.

From the end of 2019 through 2024 Q2, real GDP growth was revised up from 9.4% over the entire 2010-2019 era, and even over the relatively stronger 2017-2019 period, it grew only 2.8%. That’s lower than the 2019 average of 7.3%, but not that much lower. annualized pace from 2005-2019). points: Germany grew just 0.3%

What a ride it has been, but investors were once again rewarded for sticking to their investment plans. Productivity gains help create a virtuous cycle in which real wages grow without adding pressure to inflation, helping to keep interest rates low, which in turn spurs further investment. So, what now?

In fact, the average annual number of jobs gained from 2010-2019 was 2.2 In fact, monthly job creation averaged 163,000 in 2019, which was a year of solid economic growth. It indicates layoffs remain low, which is why initial claims for unemployment benefits match the low levels seen in 2022 and even 2018-2019. million, or 2.6

Instead, this is what happened: The economy accelerated in 2023, with GDP growth rising 3.1%, well above the 2010-2019 trend of 2.4% and 2017-2019 pace of 2.8%. This time is different” are the four most dangerous words in the investment business, but I think the current situation warrants it. In nominal terms, the U.S.

It’s clear how inflation broadened out in June 2022 relative to December 2019. The picture for March 2024 looks closer to what it did in December 2019, rather than June 2022. As the chart shows: In December 2019, just 10% of categories had inflation rates above 4% year over year. annual pace between 2005 and 2019.

The current number remains consistent with the 2018-2019 average, despite a larger labor force now. The insured unemployment rate also hasn’t deviated meaningfully from what we’ve seen the past couple of years or the 2018-2019 average. All indices are unmanaged and may not be invested into directly.

That is the best ‘worst day of the month’ since November 2019 and second best since February 2017! That number has been trending down since earlier this year, but it’s at a healthy 177,000 right now, above the 166,000 average pace in 2019. million, which matches the 2019 average. That’s below the 2019 average of 3.9%

Year Total Revenue (Rs in Crores) Profit after tax (Rs in Crores) 2019 514.02 Year Operating Profit Margin Net Profit Margin 2019 8.69% 2.55% 2020 7.93% 4.87% 2021 4.83% -2.68% 2022 9.13% 6.81% 2023 11.41% 7.63% Return Ratios: RoCE and RoE The company’s performance appears to be positive based on its return ratios. 4 2020 0.33

But it is, perhaps, the end of the beginning.” — Winston Churchill The S&P 500 was up in both January and February for the first time since 2019. It’s only slightly elevated relative to the 2017-2019 average of 2.9%. across 2018-2019. All indices are unmanaged and may not be invested into directly.

Yes, this is just one signal and we would never suggest investing based on a single data point, but looked at in the context of all the bullish signals we continue to see, this further reinforces our overall bullish stance. That’s higher than anything we saw between 2001 and 2019 (when it peaked at 80.4%). in 2019, 5.9%

pace of growth between 2010 and 2019, but it also matches the pace of growth over the three years prior to the pandemic (2017-2019) when economic growth picked up. All indices are unmanaged and may not be invested into directly. If that is close to actual GDP growth, it would mean the economy grew 2.6% over the past year.

Buckle up, as the trigger points for one of the most well-known investment axioms, “sell in May and go away,” is nearly here. in the first quarter, well above the 2010-2019 average pace of 2.4%. In fact, government spending eased in the first quarter as federal nondefense spending fell and state/local government investment pulled back.

As Lee Corso would say, “Not so fast, my friends.” From the end of 2019 through March 15, 2024, the S&P 500 has gained 71%. Single-family housing activity makes up the bulk of residential investment within GDP, and that crashed in 2022 as the Fed raised rates. All indices are unmanaged and may not be invested into directly.

Consumer strength, especially a rebound in goods spending, supported the upside surprise, while transportation equipment and defense spending investment were also strong. almost broke the economy in 2019. There was a big jump in equipment investment, bolstered by transportation spending (most notably aircraft).

Incredibly, the economy has grown faster than the 2017-2019 pace of 2.8%. Government spending (17% of the economy) is also running strong on the back of federal government nondefense and defense spending and investment, as well as state and local government spending. Median net worth rose 37% between 2019 and 2022. That added 1.3

Our stance has long been that investing is not about timing the market, but time in the market. Instead, invest and use the long run to your advantage. It’s another reminder that when it comes to investing, patience is rewarded. That’s the slowest pace since August 2021 and not far above the 2018-2019 average of 3.6%.

But we think now is more like the normalization cuts we saw in 1984, 1995, and 2019, all of which saw continued gains a year later. It turns out they are and the last time we saw this was in 2019. All indices are unmanaged and may not be invested into directly. Are rate cuts near all-time highs normal?

Yet, longer-term investors have once again been rewarded for sticking to their investment plans. For perspective, monthly job growth in 2019 averaged 166,000. All indices are unmanaged and may not be invested into directly. Payroll gains for January and December were revised lower, but that’s why we rely on three-month averages.

million in 2019. In 2018-2019, financial stresses and a slowdown prompted an about-face and led the Fed to eventually cut rates. Business investment will also likely rise. All indices are unmanaged and may not be invested into directly. Between 1996 and 1999, the unemployment rate averaged 4.8%.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content