This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This is Masters in business with Barry Ritholtz on Bloomberg Radio 00:00:17 [Speaker Changed] This week on the podcast, Jeff Becker, chairman and CEO of Jenison Associates, they’re part of the PG Im family of Asset Managements. Jenison manages over $200 billion in assets. They, they trained them together.

billion in assets. Bernstein explains the four drivers of their models: Profits, Liquidity, Sentiment, and Valuation. We discuss the challenges of launching a Quantitative Macro focused firm right into the teeth of the Great Financial Crisis in 2009. We also reminisce about the good old days at Mother Merrill.

Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. But investors may still want to consider layering in various other asset classes to help protect from this unexpected risk in the future. With future stock returns higher than they were at the start of the year and the U.S

Notable Investments and Business Ventures Kusum Finserve: Shah’s 60% stake in this company is a significant asset, reflecting his focus on the financial sector. The valuation of his home is not published, but it reflects his status. Temple Enterprise: His directorship here adds to his business credibility and income streams.

Private Credit Outshines Many High-Valuation Stocks, Bonds. With interest rates at record lows and many publicly traded bonds and stocks approaching historically high valuations, private credit has become increasingly attractive to investors because of its total return prospects, steady income and role in diversification.

The ten-year period between 2000 and 2009 is often called a “lost decade” for U.S. From January 2000 through December 2009, the S&P 500 lost 0.72 IBM’s return was fueled by growing earnings, growing dividends, and buying back stock at cheap valuations. percent per annum, including dividends.

The funds did well in the Financial Crisis and they did well in 2022 but from 2009 onward, one of his two long standing funds has a negative annual growth rate and the one with a positive growth rate was less than 1/3 of a plain vanilla 60/40 portfolio. Gold was mostly in a downtrend from mid-2011 to early 2016.

assets the cold shoulder. Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% equities to an asset allocation. From 2000 to the end of 2009, the global allocation would have outperformed by nearly 8.8% Other reasons to consider international assets in your portfolio. Valuations.

So it’s, 00:09:11 [Speaker Changed] You’ve become an enterprise, it’s 10 x what it once was in terms of headcount, it’s much bigger in terms of assets. I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular.

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Investment Perspectives | Bubbles II. Wed, 04/01/2015 - 16:48.

You mentioned in the beginning of the book lower asset yields and richer asset prices have pulled forward future returns. ILMANEN: It’s always good to think of starting yields and valuation sort of two sides of the same coin. RITHOLTZ: Really quite interesting. Explain that. Bonds are the most expensive. Stocks are pricey.

The yield on the ten year Treasury note briefly passed 5% recently, the highest yield on the ten year note since before the financial crisis of 2007 – 2009. Stocks are a risky asset class, subject to periodic bouts of panic selling due to anything from recession-induced earnings fears or geopolitical uncertainty.

Smart investors are very careful about market valuations (prices) and investor behaviour. The chart below illustrates that the smart money enters when valuations are low and the majority of the investors aren’t looking at that asset class or security. How are they prepared for that? They use the principle of margin of safety.

With the length of this current run (however you measure it), and more importantly, with rich valuations, it's hard to go a few hours without seeing a headline that a "rug pull" is imminent. Remember all the black swan funds that were launched in 2009? On the early side, for example, are those who have argued that U.S.

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/31/2009 4.9% 12/31/2009 29.6% And with intangible assets rising in the economy, standard earnings calculations are becoming less and less accurate. By Jack Forehand, CFA, CFP® ( @practicalquant ) —.

Investor enthusiasm, coupled with high valuations, has preceded all major market bubbles. He writes: The one reality that you can never change is that a higher-priced asset will produce a lower return than a lower-priced asset. stocks are based on traditional valuation metrics, via Michael Cembalest.

This range is determined by a number of factors, including but not limited to the business cycle, valuations, interest rates, inflation, and the collective mood of millions of investors. They're not wrong, since the bottom in 2009, stocks have outperformed risk free bills by 17.5% a year, the largest spread over a 7.5

1 Also, from fiscal year 2009 until fiscal year 2016, federal agencies cut annual grants to private and public organizations by 3.4% Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of asset allocation— the single biggest driver of long-term gains.

Good Preparation Leads to a Good Audit Experience: What to Expect from Your Investment Advisor mhannan Wed, 04/20/2022 - 06:03 After an extended period of strong returns that began in 2009, many not-for-profit (NFP) organizations find themselves increasingly challenged to earn the traditional target of an inflation-adjusted 5% annual spending rate.

And before that, Morgan Stanley, doing technology and operations planning for the wealth and asset management group. What percentage of the assets are in ETFs relative to mutual funds? So fast forward to where we are today, we have over $40 billion in assets under management. BERRUGA: You know, great question. BERRUGA: Exactly.

We are recommending that clients consider high-yield bonds and other asset classes that can offer the prospect of solid gains that diverge from the path of traditional stocks and bonds. No matter the investment environment, we size up an asset class by focusing on a comparison of potential gains with downside risk. 31, 2009, until Nov.

So far, this year hasn’t seen a full-blown crisis like 2008–2009 or 2020, but the ride has been very bumpy. Lower inflation tends to bring higher valuations (Fig.1). can eke out some economic growth in the second half as inflation falls and recession fears subside, we would expect valuations to get a nice lift by year-end.

In the multiyear bull market we’ve experienced since 2009, shareholders perceive these situations as persistently mediocre. Recent Spinoffs: Mix of Good and Bad Results (Valuations expressed in $ billions). . It should not be assumed that investments in such securities or asset classes have been or will be profitable.

The yield on the ten year Treasury note briefly passed 5% recently, the highest yield on the ten year note since before the financial crisis of 2007 – 2009. Stocks are a risky asset class, subject to periodic bouts of panic selling due to anything from recession-induced earnings fears or geopolitical uncertainty.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical asset allocation perspective. At the same time, the resilience of the U.S.

We work with clients to create—either in writing or verbally—a “mission statement” detailing how they want their assets to serve their well-being in coming decades. This helps to meet your immediate needs and instill discipline in a longterm context, averting excessive spending when valuations are rising.

Jerome Powell, the Fed Chair, has been a very effective clean-up hitter for the stock market, not only leading the stock market team to victories, but also appreciation in almost all global-risk asset classes. PRICES: Valuations have come down significantly – Price/Earnings ratio of 15.9 (i.e., Elections / Capitol Insurrection.

A Moment of Zen: The Wisdom of Staying Invested achen Wed, 07/19/2017 - 15:28 When discussing the merits of cash as an investment, Warren Buffett doesn’t pull his punches, saying that those who hold cash or its equivalents “have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.”

When discussing the merits of cash as an investment, Warren Buffett doesn’t pull his punches, saying that those who hold cash or its equivalents “have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.”. Valuations of the U.S. But we can’t deny the existence of fear.

During the worst of the Financial Crisis (Q3 2008 through Q1 2009), more than 50% of S&P 500 companies hit their earnings targets each quarter. But overall, we would expect modest estimate cuts to be received positively by markets, supported by lower valuations and depressed investor sentiment. Quincy Krosby , Ph.D.

is dragged down by 2008-2009 when the index tumbled 37%. We maintain our preference for equities over fixed income and cash in our recommended tactical asset allocation. Stock valuations are higher but bond yields are still low enough to support valuations with the 10-year Treasury yield well under 3% despite the big jobs number.

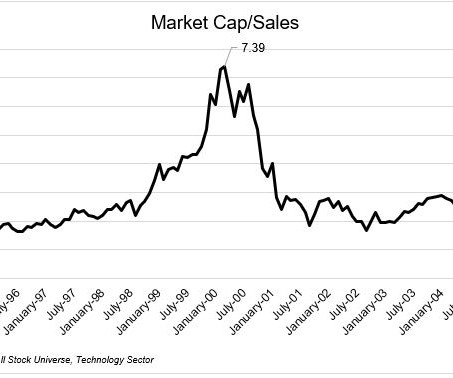

You don't understand how low interest rates make long-duration assets more valuable today. Stocks flooded the market, and valuations stretched into the stratosphere. I turned to my friends at O'Shaughnessy asset management for some tech data to see what happened to the sector as the bubble was inflating and after it burst.

The FSBF offers secured loans to micro-entrepreneurs and self-employed individuals for business purposes, asset creation (home renovation or improvement), or meeting expenses for significant economic events such as marriage, healthcare, and education. Vinay Sanghi has headed the organization since its inception in 2009.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

Memories of 2008-2009 are still vivid even though global banks, overall, are in much healthier shape due to stringent regulations put in place following the crisis. In addition, a major structural re-organization is in the planning stages that will involve sales of assets and spinning off parts of the international business.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term asset allocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions. A Matter of Time.

Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e.,

Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e., Less Efficient Asset Classes.

Below is the price chart of HUL from Jan 2000 to Jan 2009. If you do not have requisite skill-set or don’t have time, then you should hire an investment adviser who has the expertise to evaluate fair investment valuation and has the experience, temperament and skill-set to alter asset allocation with changing market dynamics and cycles.

When does crowd psychology take hope for economic return beyond what valuation can support? And why do markets irregularly detach fundamentals from valuation to their own detriment? as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition.” In his book “What is Time?

As head of asset allocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Valuations are elevated but nowhere near the bubble levels of the late 1990s. Source: Bloomberg.

As head of asset allocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Some observers are comforted that recessions since the 1970s have been preceded by oil price spikes or asset bubbles—conditions that do not exist today.

What is behind this sudden surge in the unicorn population, and are some of these valuations “spiraling” out of control? To a certain extent, the Federal Reserve’s zero-rate monetary policy has fueled the flow of money into higher-risk asset classes, since “safe” assets have been priced to yield only meager returns.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content