Tata Technologies IPO Review – GMP, Details & Much More

Trade Brains

NOVEMBER 18, 2023

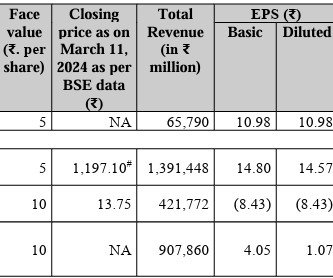

Their last offer being from Tata Consultancy Services in 2004. When we look closely at its Balance Sheet we realise that Trade Receivables are its biggest Asset constituting 21.27% of the total Balance Sheet. The Company has Contract Assets worth Rs. 718 Cr which become the 3rd largest group of assets of the Company.

Let's personalize your content