This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

But today, you know, a lot of brokers, you know, whether they’re with the big full service brokerage firms now have advisory accounts that they flog to clients where they can buy ETFs. I did it in 2000, 2002. And one of the common conversations is, I have a client, he’s got millions of dollars invested.

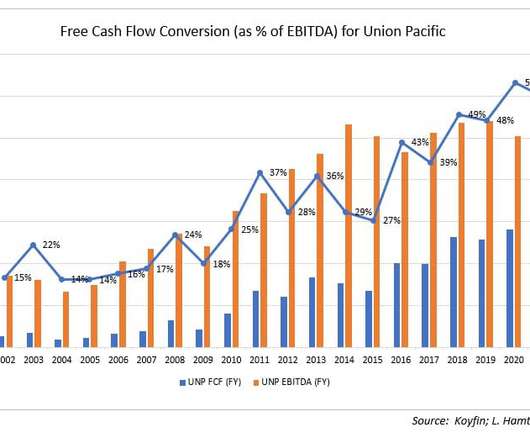

Since 2002, overall carloads on Union Pacific’s network have declined by a bit less than 1% per year, but Union Pacific’s revenues per car have increased 4% per year. Note: Clients of Fortune Financial Advisors, LLC own shares of Union Pacific, CSX, and NSC.

Strategic Planning in Volatile Markets ajackson Wed, 04/01/2020 - 09:31 Our conversations with clients usually cover topics that range beyond investment and financial affairs.

Our conversations with clients usually cover topics that range beyond investment and financial affairs. These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. Wed, 04/01/2020 - 09:31.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations.

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. And so, that didn’t happen until 2002. I mean, you know, this is probably 2002. Valuations go up and you saw it, of course, in the late ‘90s, in the tech sector.

Over the last 25 years, we have seen four bear markets (1999-2002, 2008-2009, 2020, 2022) and numerous market corrections (10% losses). Explain it to me in a way a financial advisor might explain it to a client. And yet a $100,000 investment in the S&P would be worth just shy of $700,000 today.

Our standard valuation framework looks out over a 10-year cash flow forecast ending with zero % real growth in the terminal cashflow (technically we use 3% nominal terminal growth). By this valuation method, the portfolio cashflow duration is in the 16 to 17-years range. GAAP in 2002 7.

For plans with amortization periods exceeding 30 years during three consecutive annual actuarial valuations, the plan and sponsoring groups must form an FSRP. Texas Legislature offered several benefit increases in the 1980s and 90s when the debt was lower, but no increases have occurred since 2002. RELATED BLOG POSTS.

Or are the steel tariffs of 2002 a better indicator of what we should expect—an orderly, low-impact process resolved by the WTO in fairly short order? Should we brace for the impact of the infamous 1930 Smoot-Hawley Tariff Act, which led to a contraction in global trade and exacerbated the Great Depression?

Or are the steel tariffs of 2002 a better indicator of what we should expect—an orderly, low-impact process resolved by the WTO in fairly short order? Should we brace for the impact of the infamous 1930 Smoot-Hawley Tariff Act, which led to a contraction in global trade and exacerbated the Great Depression?

And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. I got an internship at a investment fund in Baltimore, and this was 2002 at the time. With no further ado my conversation with Woodline partners, Mike Rockefeller.

Our job was basically to give sort of strategic advice to Lazard clients, which would generate capital-raising mergers and debt financing. I remember once, one of my colleagues says that a friend, one of the French Lazard Frerers partners was asked by a sort of junior, “How much should we tell our client to bid?” CHANCELLOR: Yes.

But that valuation, to be able to come up with the valuation, to be then able to work in a restructuring process, bankruptcy process, and say, Hey, I think at the end of this, we are buying debt at 50 cents. ’cause you have to sell that product to clients. How many, you had two clients, it sounds like.

But saving tax is not the only objective— clients also need to know that their financial security is assured and that the long-term stewardship of family assets will be wise. Explaining the technicalities is often only a modest help to clients. As previously mentioned, gifts of interests in FLPs are a timely example.

But saving tax is not the only objective— clients also need to know that their financial security is assured and that the long-term stewardship of family assets will be wise. Explaining the technicalities is often only a modest help to clients. As previously mentioned, gifts of interests in FLPs are a timely example.

00:44:11 [Speaker Changed] Kathy would may have her own valuation, so, but I can’t replicate it myself. A value investor can feel like I have to deal with all the clients who say, why are you losing me all this money because the stock has gone from 80 to 40, but I feel cheerier because it’s from $40 to a $90 value.

The transcript from this week’s, MiB: Aswath Damodaran: Valuations, Narratives & Academia , is below. You’re known as the dean of valuation. He said, oh, dean of valuation, it’s easier to say. So let’s start with the question, what led you to focus on valuation? RITHOLTZ: Right. And I said, why?

And then in ‘94 and ’98, you know, all had a different stream to 2002. Much of how BlackRock evolved is, you know, trying to be pressured about what is the next evolution of what clients are looking for. I mean, I said this to clients all the time, we could make the wrong decision on markets. RIEDER: A 100 percent.

I graduated Columbia 2002, and I’m the only person I know who stayed in the same job for the last 23 00:08:35 [Speaker Changed] Years. But no, but I think that where I get my best ideas is from talking to super smart people like you, like our financial advisors, like our hedge fund clients, our, our long only investor clients pensions.

00:06:39 [Speaker Changed] So clients, the LPs who come to Oak, were they just giving them cash to be allocated across all these different sectors? So pharma is a client, employers, payer employer market as a client and payers our clients beyond our customers of our companies, beyond just hospital systems.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content