This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? Note the Solo 401(k) is also referred to as an Individual 401(k).

Advisor Today Guest Column January of 2025 is the 50th anniversary to one of the most important pieces of legislation in the retirementplanning arena ever put into law by Congress. What Im referring to is the enactment of ERISA, the Employee Retirement Income Security Act.

Many of us are covered by one or more types of defined contribution retirementplans, such as a 401(k), 403(b), 457, or any of a number of other plans. What many of these plans have in common is that they are referred to as Cash Or Deferred Arrangements (CODA), as designated by the IRS. How, you might ask?

a ski chalet), assessing whether it will lead to greater overall wellbeing, or, alternatively, more stress, is more challenging Enjoy the 'light' reading! a ski chalet), assessing whether it will lead to greater overall wellbeing, or, alternatively, more stress, is more challenging Enjoy the 'light' reading!

Also in industry news this week: The latest update on the status of the Department of Labor's proposed regulation related to fiduciary advice on retirement accounts and why the agency is referring to it as a "retirement security rule" rather than a "fiduciary rule" A report suggests that RIA M&A surged in the 3rd quarter, as large acquirers resumed (..)

The post Investing for Retirement: Strategies for Long-Term Success appeared first on Yardley Wealth Management, LLC. Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. What lifestyle do you envision?

When you enter retirement, your first action may likely be to take advantage of the ability to do nothing. In retirement, this assumption is flipped on its head. Work” in retirement isn’t something you have to do; it’s something you actually want to do. In retirement, you should aim to turn your hobbies into full-time projects.

Your retirement income plan may be sending up bubbles, too, whether around Social Security, retirement account distributions, taxes or somewhere else – and these holes need to be patched up right away. So, to help your retirementplan be more airtight, let’s look at a few of the common leaks.

Saving for retirement is a long-term endeavor. It requires a different perspective on your wealth and income that accounts for your needs in different stages of your life, from the beginning of your working years through your retirement. Therefore, a strategy that is risk-balanced helps you achieve your retirement goals.

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

A few things from the last couple of days all with the theme of retirementplanning mistakes to avoid. The 4% rule of course refers to the percentage that can be safely withdrawn from portfolio assets for a sustainable retirement (not running out of money). Lastly is a list of retirement mistakes from Brett Arends.

Unusual Whales (very worth following) Tweeted that "51% of Gen-Xers and 40% of Boomers have said they are 'significantly behind' their retirement, per CNBC." We Aren't Saving Nearly Enough For Retirement. 600,000-$800,000 are workable numbers for long term retirementplanning. Barron's pegs Gen-X' perceived need at $1.1

AI engines also analyze context ensure your website content clearly defines your services, location, and specializations (e.g., “retirementplanning for small business owners” or “estate planning in New York”). Use niche-specific keywords like retirementplanning for physicians.

While grappling with various aspects of retirementplanning, it is imperative to acknowledge a critical factor that often does not receive its due attention – longevity risk. Longevity risk refers to the risk that people are living longer lifespans than previous generations.

Is retiring with a mortgage a good idea? Retiring with a mortgage doesn’t typically pose a financial risk, and at times it’s the best financial decision. But paying off a mortgage before retirement has upsides also. Here’s when it may – and may not – make sense to pay off a mortgage before retiring.

As you would expect from an outstanding organization like Microsoft, it offers a very robust 401(k) to help employees save for retirement. This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! )

This scenario is becoming increasingly common, and you can be well-equipped to guide your farmer clients through the complex process of retiring without direct heirs. Develop a succession plan Based on the financial assessment and the client’s goals, develop a detailed succession plan.

The concept of retirementplanning is simple. Despite changes in the economy or in life itself, the concept of planning your retirement has remained unchanged. We work, save, retire, and repeat for generations over. 2] This, however, does not mean that the retirement of your dreams is out of reach.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Either plan is an excellent choice, particularly if you’re not covered by an employer-sponsored retirementplan. Not exactly.

Instead, your general practitioner may have referred you to that cardiologist to diagnose a specific heart problem. We want our clients, our prospects and those who refer us to understand what we’re great at and that we’re specialists in that field, much like cardiologists are specialists in their field.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. This flexibility becomes increasingly valuable as your retirement portfolio grows more complex.

Additionally, we have news that FinCEN has announced an extension of the BOI reporting deadline and a temporary halt in enforcement, an analysis on the implications of wealth taxes in Europe, and a refresher on how the new ‘Savers Match’ program aimed at enhancing the retirement savings of millennials and Gen Z functions.

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. While a Mega Backdoor Roth IRA rolls these contributions into a Roth IRA, a Mega Backdoor Roth 401(k) converts them directly into a Roth 401k within the employer’s plan.

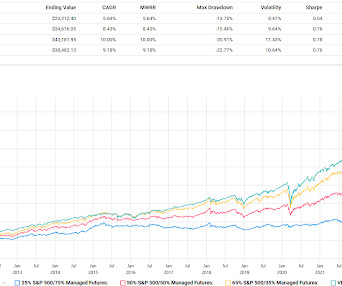

While an investor’s timeline affects their risk tolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be. For reference, a correlation of 1.0 The chart below shows how cumulative US stocks versus bond returns can impact a portfolio over time.

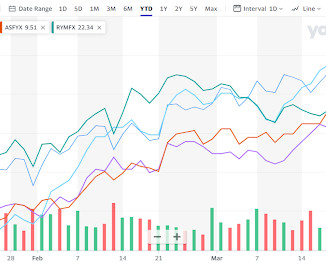

Over the last couple of months or so, we've been talking about how the crazy high yielding, single stock, covered call ETFs are not proxies for their underlying or reference securities. Instead, they are products that sell the volatility of their underlying or reference securities. Big difference.

The IRS website has this helpful Tax Withholding Estimator you can use as a reference if you are unsure how much to withhold. Explore Tax-Advantaged Accounts: One way to lower your tax burden is to take advantage of your employer’s retirementplan if they have one by contributing pre-tax dollars into your 401(k) or 403(b).

Add keywords your audience might use, like Financial Advisor | RetirementPlanning or “Wealth Management | Tax Planning.” Include Keywords for Discoverability People search Instagram like they do Google, so include keywords like retirementplanning, wealth advisor, or student loan help to boost discoverability.

Preparing for retirement is a significant life transition that demands a clear understanding of your financial situation. This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age.

The biggest benefit of maxing out your 401k is the chance to save more money for retirement. Articles related to 401k accounts and retirement savings Decide if you should max out your 401k to increase your retirement savings! 4 Reasons you should A 401k is one of the most common types of employer-sponsored retirementplans.

Leveraging retirementplans for tax advantages Tech entrepreneurs can create substantial tax advantages through Solo 401(k) plans, which allow contributions up to $69,000 in January 1, 2024 for those under 50. For growing tech startups, establishing company retirementplans serves multiple purposes beyond tax benefits.

There was also a reference to the term on an episode of The Simpsons. If an investor has $1 million for retirement and is expecting $40,000/yr and the tontine kicks out 8%, something like $100,000 into the tontine provides 20% of expected income with only 10% of assets, it presents an opportunity for capital efficiency. Stay tuned.

Let’s take a deep look at both plans, and particularly at where each stands out. It’s one of the best strategies to supercharge your retirement savings, especially for early retirement. There's no time like the present to begin preparing for your retirement. This is what’s referred to as the IRS pro rata rules.

Healthcare Costs After Retirement — Securing Your Parents’ Future Retirement is a long-awaited phase of life where individuals can enjoy the fruits of their labor and enjoy well-deserved rest. With medical expenses on the rise, planning for healthcare during retirement becomes crucial to ensure a secure future.

Healthcare Costs After Retirement — Securing Your Parents’ Future Retirement is a long-awaited phase of life where individuals can enjoy the fruits of their labor and enjoy well-deserved rest. With medical expenses on the rise, planning for healthcare during retirement becomes crucial to ensure a secure future.

Real returns” refer to the returns on their investments after you take inflation into account. This means that with qualified assets sitting in cash, retirement savings are at risk of being outpaced by inflation. For example, if the return for a bond mutual fund is 2% but inflation is 7%, the investor sustained a real return of -5%.

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older. For the majority of people, however, April 15th will remain the deadline.

Introduction to GIFT City and Its Legal-Economic Status The Gujarat International Finance Tech-City, commonly referred to as GIFT City, is a landmark initiative by the Government of India aimed at creating a world-class financial centre within the country.

The Wall Street Journal took what might be a sympathetic approach to 401k investors who might be feeling disillusioned by generally poor performance with the focus being on target date funds which have of course become a major staple of 401k plans. First, it's your retirement, how do you not care enough to engage just a little?

Legacy planning also represents an important opportunity for financial professionals. This refers to the client’s intentions to continue working with you, invest additional assets with you, and refer you to friends and family. Legacy planning gives you an opportunity to demonstrate your empathy.

Advisors offer insights on retirement, long-term care, or market trends over lunch at a local café or conference room. One advisor noted that these events draw not only current clients but also curious prospects who are actively exploring retirementplanning options. How do I promote an advisor event effectively?

How To Grow Your RetirementPlan Business In The 2020 Economic Crisis. We’ll review: – How has the retirement landscape been affected by COVID-19? – How can advisors grow their retirement business in the current crisis? I’m super excited to welcome the team at Retirement Learning Center.

He referred to the non-managed futures alts at "diversified alpha" but never specified what strategies to include with managed futures. Picture retiring in 2010 versus 2020. This has sort of been my positioning. Fun note, the 1878 banking crisis was mentioned in an episode of Deadwood. This is in the neighborhood of sequence of return.

Price Action Lab had a blog post that amusingly referred to managed futures as being a long term commitment. That led to an older post that tried to figure out the optimal allocation to managed futures.

The literature refers to it being like a structured product. Speaking of things that are worth learning about even if you never use them, Calamos just launched an Autocallable Income ETF (CAIE). It appears that it is somewhere in the defined outcome/buffer/derivative income fund realm.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content