This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

riabiz.com) Risktolerance Determining a client's risktolerance is more complicated than having them fill out a questionnaire. advisorperspectives.com) Does risktolerance change in retirement? morningstar.com) Risktolerance questionnaires are conversation starters. signaturefd-3437664.hs-sites.com)

Measuring a client's risktolerance is both an art and a science. Beyond assessing how a client feels in the moment, advisors must evaluate a client's long-term behavioral tendencies, actual risk capacity, and financial goals – all of which require considerable time and skill.

What's unique about Nina, though, is how she has developed a "money personality" assessment that allows her to both better understand how her clients' money behaviors might affect the financial planning process and to ensure consistent client service among the advisors at her firm.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risktolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financial planning. Read More.

Also in industry news this week: In the continued absence of formal SEC guidance on advisory firm use of Artificial Intelligence (AI), many firms are taking a curious, but cautious, approach toward adopting AI-powered tools A recent report identifies the growing total wealth controlled by women in the U.S.

Also in industry news this week: 43% of wealth management firms are frustrated with the effectiveness of their CRM software, spurred on by challenges with integrations and workflows, according to a recent survey The Social Security Administration this week announced a 2.5%

We also talk about why Pete views his investing style as a core holding in client portfolios (rather than a thematic addition) in part because he still seeks to at least roughly track the sector composition of broader market indices with investments that meet his sustainability criteria, why Pete uses a combination of individual stocks, ETFs, and mutual (..)

Which, according to Kitces Research on Advisor Productivity, can lead to higher productivity for advisor teams (but can require an investment in staffing and higher-end planning services to meet their complex planning needs).

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For some clients, “risk” maybe something exciting or daring that they enjoy and not something they generally avert from.

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns. Read More.

This month's edition kicks off with the news that Riskalyze has completed its previously-announced rebranding, and will now be known as “Nitrogen”, a ”growth platform” for advisory firms – which represents less of a shift in the platform’s core function (given that Riskalyze’s risktolerance tool was always (..)

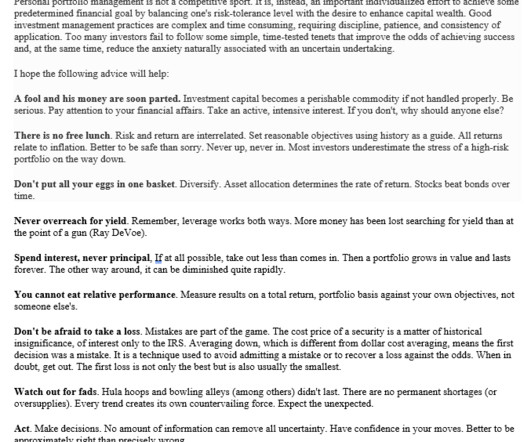

It is, instead, an important individualized effort to achieve some predetermined financial goal by balancing ones risk-tolerance level with the desire to enhance capital wealth. Stick to your plan. No amount of information can remove all uncertainty. Have confidence in your moves. Take the long view.

This month's edition kicks off with the news that 'startup' custodian Altruist has completed a $169 million fundraising round as it continues to rebuild the RIA custodial tech stack layer-by-layer while positioning itself as the biggest RIA custodian built from scratch and solely for advisors – which, while making it the clear #3 custodian behind (..)

Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. High deductible health insurance plans . These types of plans are becoming more common with employers and are available privately as well. How the HSA works . Click To Tweet.

Over the years, 2 types of measurement tools have emerged as the standards for assessing risktolerance: 1) psychometric tests, which feature a series of questions (such as, "What amount of risk do you feel you have taken with past financial decisions?") Read More.

morningstar.com) Ryan Detrick and Sonu Varghese talk with Phil Pearlman about the connection between health and wealth planning. thinkadvisor.com) Being able to move unused 529 plan funds into an IRA is a neat trick. mikemelissinos.substack.com) On the difference between risktolerance and risk perception.

Also in industry news this week: How Goldman Sachs’ RIA custodial platform is leveraging the resources of its parent company as it seeks to build momentum amidst a highly competitive environment among custodians How NASAA has changed the substance and/or scoring of the Series 63, 65, and 66 exams From there, we have several articles on college (..)

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns. Read More.

The financial planning industry is constantly undergoing change. This article will discuss some of the most pivotal financial planning industry trends to watch out for this year. They would also want to plan how and when to withdraw funds since different accounts come with different tax implications.

Monte Carlo simulations have become a central method of conducting financial planning analyses for clients and are a feature of most comprehensive financial planning software programs. a client who really wanted to guard against downward-spending-adjustment-risk might forgo income increases entirely). Read More.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

His next step was to systematize his planning process to help him work more efficiently as a solo firm owner. He also built redundancies into his planning process (e.g., And because nuclear power is a process-driven industry, the use of standard workflows was familiar ground for many of his prospective clients. Read More.

Enter bucketing, a powerful strategy that helps simplify your financial planning by categorizing your assets into three time-based buckets: today, tomorrow, and the future. By dividing your investments into these three buckets, you help create a clear plan for how and when your money will be used. What Is Bucketing?

Exploring the Benefits of Financial Planning appeared first on Yardley Wealth Management, LLC. Goal Setting and Planning Many people discover that talking to a financial planner is worth it simply for the structured approach to goal setting. The post Is Talking to a Financial Planner Worth It?

Which means that when an advisor recommends a certain investment strategy for a client, their standards of care should dictate that they first make sure that the strategy is within the client's tolerance for risk.

It is essential to choose investments that match your risk appetite to avoid unnecessary stress and surprises later. A financial advisor can help you understand your investment risktolerance. This article will focus on the risks of investing, how they impact you, and what you can do to determine your risk appetite.

Which means that longer-term projects, such as creating a succession plan to have in place for the firm when the owner retires, may tend to get put on the back burner.

Knowledge and Personalized Planning Financial advisors can bring a wealth of knowledge from extensive education and experience, helping enable them to craft tailored strategies that align with your unique financial goals. This personalized approach can help you make financial decisions that are well-informed and strategically sound.

The post Staying Disciplined: How to Stick to Your Financial Plan Despite Market Volatility appeared first on Yardley Wealth Management, LLC. Staying Disciplined: How to Stick to Your Financial Plan Despite Market Volatility Introduction: Market volatility is a fact of life for investors.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Do nothing. Look for bargains.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

For more years than I’d care to name, I’ve been trying to put my finger on exactly why I have a such a huge problem with the traditional (Think: Riskalyze, now Nitrogen) risktolerance assessments in the financial planning profession. You can actually test various bear markets and adjust accordingly.)

Many of us are covered by one or more types of defined contribution retirement plans, such as a 401(k), 403(b), 457, or any of a number of other plans. What many of these plans have in common is that they are referred to as Cash Or Deferred Arrangements (CODA), as designated by the IRS. So, what should you do about this?

In this article, we will explore three popular savings and investment options: 529 Plans, Roth IRAs, and Real Estate. Each has unique benefits and drawbacks, and understanding these can help you decide which fits best with your financial situation, risktolerance, and goals.

Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. Do you plan to travel extensively, pursue hobbies, or volunteer? Learn more about retirement plan options here. What lifestyle do you envision?

For investors, this may be a time to revisit your financial plan, not to panic. Consider speaking with a financial advisor about risktolerance and strategies like tax loss harvesting. Stay tuned for next week. Andres Disclosure: This material provided by Zoe Financial is for informational purposes only.

During recent conversations, I’ve come across several people unfamiliar with the concept of fee-only financial planning, let alone considering it as a feasible choice. To shed light on this, I want to articulate the distinctive approach we use at MainStreet Financial Planning.

Having an experienced financial advisor by your side can help you stay grounded in your plan, even when markets feel anything but steady. Your financial plan is designed for the long term. This may be a good time to revisit it and ensure it still reflects your needs, risktolerance, and goals.

Exercise strategy: Timing: Consider the tax implications of exercising vested options before or after the IPO, timing of sales, and tax planning opportunities. Sales and trading plan: Taking profits: Once the lockup period ends, consider diversifying your holdings to reduce risk.

Riskalyze signals an intent to rebrand itself away from ‘just’ risktolerance assessments to a broader focus on helping advisors grow clients and assets. Hearsay Systems rolls out a new small-to-mid-sized RIA platform for social media compliance and website design.

We’ll also explore the role of income tiers, provide real-world case studies, and highlight key considerations when implementing this strategy in your financial plan. Key benefits include: Ensuring essential financial obligations are met first – Taxes, estate planning, and retirement savings take precedence.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content