This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirementplanning process involves simulating whether the client's assets will last through retirement. Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives.

This approach typically provides greater benefits to those who have significant assets and high taxable income in retirement. Consider your next steps carefully and find a strategy that is consistent with your retirementplanning goals and wealth management objectives.

That number is from a Bankrate article I found on a Google search. I'd be curious to hear if anyone else does the same search and finds a different number of lost coins. First, is the math right based on my numbers? That roughly two million Bitcoin is actually more than 10% because approximately 3.8

Quarterly statements will be required to include numbers on lifetime income. Having an income plan is key for your retirementplanning. Is an annuity something you should consider as a part of your retirementplan and a way to protect what you have? Look at the math to understand and believe it.

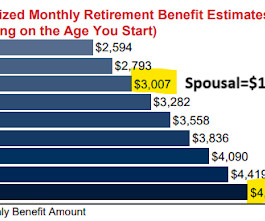

I've said many times that I plan to wait until 70 and that I think my wife should take hers at the same time which would be 64 and 2 months. My 64 and 2 month number is $3049 which is where I get the $1524.50 number for her. This whole exercise was bottom up and based on very simple questions.

But here’s the thing: whether you retire at 50 or 67, it isn’t just about leaving work, but being ready for what comes after. Start planning early. It takes strategic foresight, hard numbers, and smart decisions that begin well before your final day at work. Yet far too many professionals delay the planning process.

My process here for the notional values was that the multiplier is 100 so a put struck at 4100 would hedge $410,000 worth of stock, so then I just multiplied the dollar amount by the number of puts. Why wouldn't the fund have already blown up earlier this year when the S&P 500 was up more?

3] So, it’s easy math: the less you work, the less you’ll earn. Next, try to hold off on filing for Social Security benefits until you reach full retirement age. Lastly, it is crucial that individuals planning to earn Social Security monitor their earnings and check for mistakes once enrolled.

Matt Kory, Vice President, Retirement Programs As a retirement income vehicle, the 401(k) is second in popularity only to Social Security – and as CNBC reported in 2019 the number of 401(k) millionaires is at an all-time high. But is a million dollars even enough for your retirement needs? Just think of the numbers.

I haven't seen too many scenarios where Roth conversions were optimal as most people don't earn more after they retire. Do the math on your particulars like what your various sources of earned income will likely be, how much your RMDs will likely be and so on. With more normal scenarios, really crunch the numbers with your accountant.

The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. That just isn't the reality. The diversification benefits of intermediate and longer term bonds is not what it used to be. Taking volatility out of a fixed income portfolio is fairly simple.

Generally they all plan to work to 70 or beyond out of necessity. There was an odd and I believe inaccurate emphasis on workplace retirementplans pivoting from defined benefit plans (pensions) to defined contribution plans (401k) starting around the turn of the century. That is Rooster. Rooster loves duck toys.

They aren’t likely to get rid of the person who knows the numbers. If you’re good with math, then turning to financial planning or accounting or opening up a similar company could be one of the best recession proof businesses to start! You dont have to be managing million-dollar portfolios either.

Do the bottom up work, it won't take long, to figure out some real numbers. Someone who is 50, who stands to collect $3000 from SS, expecting to spend $5500/mo all in when they retire but who only has $200,000 has some work to do. Simple math is that this person needs to save $23/yr to come up with that additional $350,000.

A harsh reality is that $50,000 is not a retirement fund but it is a pretty robust emergency fund. We've gone over the math before that starting as late as 55 can catch a lot of the way up if they can afford to save a very high percentage of their income.

That is difficult to pull off but if you do the math on that it shows long term outperformance. He makes a good point about not relying solely on math to assess markets and portfolio construction, that the psychology of markets is important too. 75/50 seeks to capture 75% of the upside with only 50% of the downside.

Calculation Breakdown Let’s break down the math to find out how much you could earn annually with a $30 hourly wage: Consider an average workweek of 40 hours and an average year consisting of 52 weeks. Then $27,750 is the magic number. Let’s do math again! What Does $30 an Hour Translate to in Terms of Paycheck?

Generally speaking, pensions are less viable than they used to be, the math doesn't work as well. About 40 years ago employers started to pivot away from pensions to 401k, they started to pivot away from defined benefit plans to defined contribution plans. So that's quite a bit to chew on even if it isn't a new idea.

and that is the number I will assume. The math shows the NTSX/ARBIX/BTAL combo would be down 14.7% ARBIX could be replaced by any number of other funds targeting different strategies toward the same type of result. First I will say that somethin ain't right with that VBAIX result. or 110 basis points more than VBAIX.

Part of the math that determines options premiums is the risk free rate of return from T-bills. Building a plan based on assuming an 11% payout forever is really going to hurt this guy if that is what he is saying. Covered call funds have many favorable attributes. Keeping up with the broad stock market is not one of them.

Kurtosis is a very fancy word where the higher the number, the greater the risk of an outlier result like 2022. A lower number is a mathematical representation of smoothing out the ride via fewer/smaller outlier results. The math is only off by a shade using leverage via UST and a little bit of SSO, remember RPAR is leveraged.

The way my new firm is set up, I could outsource everything, for a fee, and the way this was positioned, I think there might be a decent number of advisors who do just that. So using simple math, the total return is 34% versus 72% for the common. They talked about how outsourcing model construction can save advisors a lot of time.

They spend hours writing articles and finally hit that “Submit” button… only to not get anywhere near the number of leads that they thought they would. RetirementPlanning. Retirementplanning is a very precise process, and one that is unique to the individual. Beneficiary RMD Calculator.

For the 5 year bull market you could simplistically add 10% per year or 50% total in dividends and for this year 7 or 8% (six months worth) back in which changes the numbers considerably. Yahoo doesn't show total return. Is QYLD any sort of proxy for the NASDAQ 100? That long term chart really is something for how flat it is has been.

A 20% drop in managed futures that is leveraged to a 40% weight would have added another 800 basis points to the decline (simple math). I'd put an asterisk by the volatility number because of how little of the original capital was exposed to risk. In 2008, VBAIX was down 23%. The risk/reward in this example doesn't seem worth it to me.

It has to be such a different set, the retirementplanning is different, the safety net is different. And I did the math, and I think at that point in time, roughly speaking, assets in ETS were roughly just 10 percent, 12 percent of assets in mutual funds and I was pretty convinced that that number was to increase significantly.

Suddenly, you find yourself entering a world where numbers come alive, swirling and dancing to the beat of hourly wages and annual salaries. Calculate the total number of working hours in a year by multiplying the weekly hours (40) by the weeks in a year (52), which equals 2,080 hours. Sounds amazing, doesn’t it?

Here are some other numbers compared to the S&P 500 and VBAIX which is a proxy for a 60/40 portfolio. The way the math works, a 67% allocation to NTSX replicates 100% into a 60/40 portfolio which leaves 33% left over to do something. Not exactly. Obviously it was down almost 30% last year versus down almost 20% for the S&P 500.

We dove in on the math at my old URL (sad story, no longer exists) and the math checks out. We played around with some numbers earlier in the week on the impact that a 20% allocation to a couple of different diversifiers. A long time ago I wrote about a portfolio concept derived by John Serrapere called 75/50.

Once you know your weekly or monthly income, you can do the simple math of calculating how much 70% would be. Once you’ve set up your emergency fund and a few sinking funds, get to work on retirement. Retirement is a huge goal to prepare for, but the sooner you can start learning tips for retirementplanning , the better off you’ll be.

The term “turnkey” means the numbers have been crunched, the home may have been rehabbed, and may already include tenants! The math when paying down debt is simple – if your loan is currently at 7% and you refinance at 3%, that’s equivalent to a 4% return on your money! All you, as the investor, have to do is put up the cash.

This article is a deep dive into healthcare costs in retirement. If you’re planning smartly for the long haul, this is where your attention should be focused. The overlooked cost of retirement: Healthcare expenses Let’s start with a number most people underestimate, by a lot. That’s why ongoing planning matters.

This article obviously favors more stocks but an interesting thing not said was at what number would it make sense to just flip from individual holdings to mutual funds and ETFs. In my opinion the diversification benefit hits diminishing returns pretty close to 40 individual holdings based on math if nothing else.

The term personal finance ratios might give you flashbacks to math class, learning various formulas, equations, and ratios. In mathematical terms, a ratio is essentially a way to compare two numbers. Since finance is all about numbers, that can come in handy in many ways especially when making financial calculations!

Run Your Numbers You need to get a handle on your various sources of income and where they are housed — as in, how easily you can access them when you need them. After you’ve done this math, you might be wondering if you have “enough,” and certainly that’s hard to assess when there are so many unknowns.

It is generally accepted that the various ideas around extending the retirement age and increasing taxes would solve much of the problem. The last sentence is about the math involved not about the right and wrong of any of it which we'll get to. Now comes the grim numbers about how much we have collectively saved for retirement.

As a matter of math, it cannot repeat the run from 8.5% It's not that 60/40, or some other combination of numbers is bad or dead, more like how we build the 40 or other number maybe needs to be different. when the chart starts, down to 1.09% per Yahoo, after bottoming out in the neighborhood of 0.50%. in November.

Quick math: If you have $1.828 million in the bank. And , you have to do the math by hand. To What If Analysis, what if I pay… So I’m doing my cash flow planning in my retirementplan, and I say, You know, I don’t wanna have to pay for in as a retirement. Here’s another example.

If the math is not clear on the 80/20 looking like 60% equities, the allocation is 80% plain vanilla equity and then subtract the 20% in the inverse fund which gets to a 60% net equity exposure. I'm not sure how much fixed income that has equity beta should be in a portfolio but I don't think it's a high number.

Not only has she been named to a number of hundred most influential women in finance, I don’t know many people who have seen as much of this industry on the front lines as she has for as long as she has, and is now in a position to very much drive change within the industry as CEO. Natalie Wolfson is CEO of Orion.

Lastly, one of the Bloomberg pre-market emails talked briefly about people being unable, financially, to retire, that continuing to work is their Plan A. Coincidentally, I got my annual email from the Social Security Admin with my updated numbers. An important point to reiterate is they want us to know what our numbers are.

That is inline with one way we've expressed inflation math before, that with average 3% price inflation, expenses would increase by 50% in 15 years. I suspect the real number is in the middle. As people get close to and then into retirement, hopefully the mortgage payment goes away. Unusual Whales Tweeted out the following.

These numbers are so incomprehensibly large that they lack any meaning. In a recent Axios article, Being 30 then and now , the author wrote "In 1975, only a quarter of 25 to 34-year-old men made less than $30K per year, but that number rose to 41% in 2016." workers participate in an employer-sponsored retirementplan. (

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content