This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

riabiz.com) Risktolerance Determining a client's risktolerance is more complicated than having them fill out a questionnaire. advisorperspectives.com) Does risktolerance change in retirement? morningstar.com) Risktolerance questionnaires are conversation starters. signaturefd-3437664.hs-sites.com)

Measuring a client's risktolerance is both an art and a science. Beyond assessing how a client feels in the moment, advisors must evaluate a client's long-term behavioral tendencies, actual risk capacity, and financial goals – all of which require considerable time and skill.

Nina is a partner of Stratos CA, a hybrid advisory firm affiliated with Stratos Wealth Partners and based in Los Angeles, California, that oversees approximately $500 million in assets under management for 300 client households.

Pete is the Director of Sustainable Investing of Earth Equity Advisors, an RIA based in Asheville, North Carolina, that oversees approximately $200 million in assets under management for 250 client households.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Which, according to Kitces Research on Advisor Productivity, can lead to higher productivity for advisor teams (but can require an investment in staffing and higher-end planning services to meet their complex planning needs).

Also in industry news this week: 43% of wealth management firms are frustrated with the effectiveness of their CRM software, spurred on by challenges with integrations and workflows, according to a recent survey The Social Security Administration this week announced a 2.5%

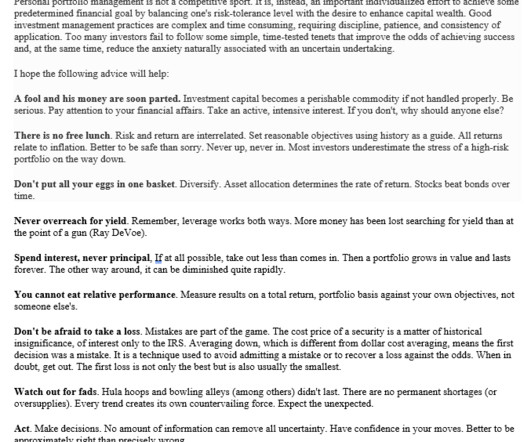

He eventually became president of Merrill Lynch Asset Management, leading the division with a value-oriented approach and a focus on long-term fundamentals. He co-authored Investment Analysis and Portfolio Management , now in its fifth edition. Stick to your plan. and served as Chairman of the Board. Take the long view.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For some clients, “risk” maybe something exciting or daring that they enjoy and not something they generally avert from.

Podcasts Michael Kitces talks setting boundaries with Emily Rassam who is the Senior Financial Planner for Archer Investment Management. morningstar.com) Ryan Detrick and Sonu Varghese talk with Phil Pearlman about the connection between health and wealth planning. open.spotify.com) Cameron Passmore and Benjamin Felix talk with Prof.

The post Waterfall Wealth Management: A Strategic Approach appeared first on Yardley Wealth Management, LLC. We’ll also explore the role of income tiers, provide real-world case studies, and highlight key considerations when implementing this strategy in your financial plan.

Without proper planning, healthcare expenses can quickly consume a significant portion of retirement savings. Below are key areas where financial advisors add value in managing healthcare expenses: 1. Financial advisors specializing in healthcare planning provide clarity and structure in this process.

Unfortunately, most executives and insiders have less flexibility to reduce risk on a concentrated position of company stock. The situational nature of planning to diversify one large position cannot be over-emphasized, so it’s important to work with a financial advisor who has experience in this area.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that a recent study found that advisory forms working with a younger client base tend to have relatively stronger growth in assets under management and revenue over time.

Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. High deductible health insurance plans . These types of plans are becoming more common with employers and are available privately as well. How the HSA works . Click To Tweet.

Exploring the Benefits of Financial Planning appeared first on Yardley Wealth Management, LLC. Goal Setting and Planning Many people discover that talking to a financial planner is worth it simply for the structured approach to goal setting. The team at Yardley Wealth Management is here to help.

While some individuals manage their finances independently or utilize automated platforms, the personalized guidance of a financial advisor may offer distinct advantages. One study found that an advisor-managed portfolio could produce an additional 3% value add annually over a self-managed (DIY) portfolio.

When it comes to managing your wealth and pursuing your financial goals, clarity can be key. Enter bucketing, a powerful strategy that helps simplify your financial planning by categorizing your assets into three time-based buckets: today, tomorrow, and the future. What Is Bucketing?

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

The financial planning industry is constantly undergoing change. This article will discuss some of the most pivotal financial planning industry trends to watch out for this year. They would also want to plan how and when to withdraw funds since different accounts come with different tax implications.

His next step was to systematize his planning process to help him work more efficiently as a solo firm owner. He also built redundancies into his planning process (e.g., And because nuclear power is a process-driven industry, the use of standard workflows was familiar ground for many of his prospective clients. Read More.

Which means that longer-term projects, such as creating a succession plan to have in place for the firm when the owner retires, may tend to get put on the back burner. Key components of this transition include client service oversight, sales oversight, strategy leadership, and financial management.

The post Staying Disciplined: How to Stick to Your Financial Plan Despite Market Volatility appeared first on Yardley Wealth Management, LLC. Staying Disciplined: How to Stick to Your Financial Plan Despite Market Volatility Introduction: Market volatility is a fact of life for investors.

Start planning early. Yet far too many professionals delay the planning process. Even if you don’t plan to retire unusually early, starting your retirement planning now can dramatically improve your options later. A bridge plan for health insurance (since Medicare only begins at 65). And the best way to do that?

While no investment is entirely devoid of risk, and there is always some degree of threat to your money when you put it in the market, you can managerisk and protect your investments with some strategies. It is essential to choose investments that match your risk appetite to avoid unnecessary stress and surprises later.

Financial planning can take your money game up a notch by bringing clarity, strategy, and intention to your financial life. A healthy financial plan gives you the tools to take control of your finances and start living your life with passion, purpose, and freedom. So what’s the value of a financial plan? Tax Planning.

In this article, we will explore three popular savings and investment options: 529 Plans, Roth IRAs, and Real Estate. Each has unique benefits and drawbacks, and understanding these can help you decide which fits best with your financial situation, risktolerance, and goals.

Exercise strategy: Timing: Consider the tax implications of exercising vested options before or after the IPO, timing of sales, and tax planning opportunities. Sales and trading plan: Taking profits: Once the lockup period ends, consider diversifying your holdings to reduce risk.

Category: Clients Risk. When it comes to their investment portfolios many tend to have a low-risktolerance and with the unsettling economic situation with the ongoing pandemic, the word “risk” has become even more of a fearsome word for clients. Related: How to Determine Your Client’s Risk Capacity!

The post Investing for Retirement: Strategies for Long-Term Success appeared first on Yardley Wealth Management, LLC. Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. Learn more about retirement plan options here.

Keeping it safe, growing it wisely, and using it to support your future takes careful planning. Wealth management isn’t only for the ultra-rich. Yet even the best financial plans can stumble. Mistake #2: Not having an estate plan in place Estate planning is essential for protecting what you’ve worked hard to build.

Your investing strategy is a personal approach based on your goals, life stage and risktolerance. Active investing involves a hands-on approach to managing your portfolio. Transaction fees, management fees, and capital gains taxes can eat into your returns. of professionally managed portfolios in the U.S.

You can choose something standard, have a standard portfolio tailored slightly to your needs, or have an investment advisor build a portfolio just for you based on your resources, needs, goals, timeline, risktolerance, current market conditions, and more. One basic and popular strategy for building a portfolio is the 60/40 model.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Take stock of where you are. Costs matter.

When it comes to money management, there are a lot of different schools of thought. Are you good with numbers, accounting, and financial planning? If yes, then DIY financial planning might be a good option for you. What is DIY financial planning? Chalk out a financial plan. Property planning.

Although money cannot buy you happiness, it can bring a sense of security if you know how to manage your money correctly. Without a handle on money management, you may always feel like your life is one step away from a financial cliff. Let’s dive into how to manage your money the right way. Make a plan for your money.

It’s really important from a financial well-being point of view for people to have their own individual authentic goals hopefully baked into some form of a financial plan. Brian Portnoy : Investing outside of a well-defined financial plan is speculation.

It is for information and planning purposes only. Whether youre new to investing or have years of experience, taking a step back to evaluate your strategy can help ensure that your portfolio remains aligned with your objectives, especially in times of market uncertainty and volatility.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirement plans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Here are some key points to use with clients as you help them assess their retirement plans.

High yields can be a sign of underlying issues with the company that puts principal at risk and endangers the dividend income if the company’s financials cannot support it. Before you can evaluate stocks or bonds to invest in, you’ll need to develop the metrics you plan to use in the analysis. versus 1.1%

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

For example, your plan might call for a 60% allocation to stocks but with the gains that stocks have experienced you might now be at 70% or more. This is great as long as the market continues to rise, but you are at increased risk should the market head down. Financial Planning is vital. Maybe they’re right. Click To Tweet.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content