This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. What is the Lifetime Gift Tax Exemption? million ($27.22

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on taxplanning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments.

Whether you are contemplating forming an LP or already operate one, gaining clarity on tax matters can optimize your financial outcomes and ensure compliance with state and federal regulations. LPs are governed by a partnership agreement that outlines the roles, responsibilities, profit distribution, and other operational details.

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

Instead, partners (investors) are taxed directly on their share of the fund’s income, gains, losses, and deductions, regardless of whether those amounts are actually distributed. Each partner receives a Schedule K-1, which reports their share of the fund’s tax items. FIRPTA planning using a U.S.

With proper planning, certain tax obligations can be legally deferred, reduced, or in some cases eliminated entirely. To maximize the value you ultimately receive from your exit, incorporating comprehensive taxplanning into your strategy is highly advantageous.

The Tax Cuts and Jobs Act of 2017 eliminated recharacterization, transforming Roth conversions into permanent decisions requiring thorough analysis before execution. Roth IRAs offer unique advantages including tax-free growth, no required minimum distributions during the owner’s lifetime, and potential tax benefits for heirs.

By exploring these nuances, you can better appreciate the tax advantages and responsibilities that come with running a Co-op. Understanding Co-op Taxes Key Tax Deductions and Credits Taxplanning tips for a Co-op Final Thoughts on Understanding Co-op Taxes Partner with Harness for Expert Tax Support What Is a Cooperative (Co-op)?

A financial advisor can help with maximizing your retirement income through taxplanning After retirement, your income sources may become limited to pensions, Social Security benefits, and investment income. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income.

Whether you are contemplating forming an LP or already operate one, gaining clarity on tax matters can optimize your financial outcomes and ensure compliance with state and federal regulations. LPs are governed by a partnership agreement that outlines the roles, responsibilities, profit distribution, and other operational details.

Backdoor Roth 401(k) $23,000 ($30,500 if 50+) Allows conversion of 401(k) funds to Roth, increasing tax diversification Required Minimum Distributions apply. It also requires an individuals 401(k) plan to allow after-tax contributions and in-service withdrawals. Complex setup process.

Whether you are starting a new business or evaluating your current structure, gaining a clear understanding of C Corp taxation will help you make informed decisions and optimize your tax strategy. Unlike other business structures such as sole proprietorships or partnerships, a C Corp is subject to corporate income tax on its profits.

Use a qualified charitable distribution (QCD) from your individual retirement account (IRA). If you are age 70 ½ or older, you can transfer money from your IRA to a charity as a qualified charitable distribution (QCD), which makes it tax-free up to $100,000 ($200,000 if you file jointly).

Additionally, partnerships are beneficial for family businesses or groups of investors who want to combine their efforts while maintaining a straightforward tax structure. The ability to customize the partnership agreement allows partners to define roles, responsibilities, and profit distribution in a way that best fits their needs.

Additionally, partnerships are beneficial for family businesses or groups of investors who want to combine their efforts while maintaining a straightforward tax structure. The ability to customize the partnership agreement allows partners to define roles, responsibilities, and profit distribution in a way that best fits their needs.

If you earn income from various sources throughout the year, such as equity windfalls, venture capital fund distributions, crypto investments, and sales, or small business income, you will need to pay estimated quarterly taxes. Failing to make these payments on time can result in penalties and interest charges.

Understanding LLC Taxes Key Tax Deductions and Credits Common Tax Deductions for an LLC TaxPlanning Tips for an LLC Final Thoughts on Understanding LLC Taxes Partner with Harness for Expert Tax Support What Is a Limited Liability Company (LLC)?

Understanding LLC Taxes Key Tax Deductions and Credits Common Tax Deductions for an LLC TaxPlanning Tips for an LLC Final Thoughts on Understanding LLC Taxes Partner with Harness for Expert Tax Support What Is a Limited Liability Company (LLC)?

These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions. And you’ll see in our Q&A below, that tax advisors can bring estate planning into the conversation early on in a client relationship.

So, the ability to provide a truly holistic offering all-under-one-roof – including not only investments but taxplanning, family office services, trusts, and the ability to advise on assets held away – is seen by clients as a real benefit.

Certified Public Accountant (CPA) CPAs specialize in taxplanning and accounting. While they may not be exclusively wealth managers, their expertise in tax matters can be invaluable in managing your taxes efficiently. TaxPlanning Effective taxplanning can significantly impact your overall financial well-being.

Certified Public Accountant (CPA) CPAs specialize in taxplanning and accounting. While they may not be exclusively wealth managers, their expertise in tax matters can be invaluable in managing your taxes efficiently. TaxPlanning Effective taxplanning can significantly impact your overall financial well-being.

If you’re a CPA who works with clients on more than just annual tax returns, you’re likely already providing accounting advisory services. This emerging discipline offers a wealth of opportunities for both clients and accounting firms, and focuses on providing strategic guidance and future-focused taxplanning throughout the year.

Failure to make this election in the first year and complete annual reporting, can trigger punitive treatment under IRC 1291, which is known as the excess distribution regime. Protect your investments by communicating with your investment provider and ensuring compliance with all necessary reporting requirements.

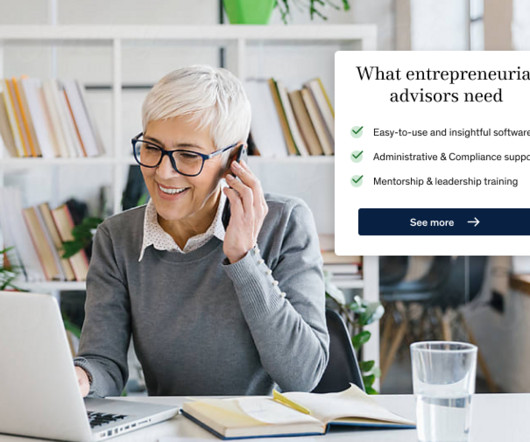

However, in the past three decades, the confluence of tech innovation, and the democratization of financial product distribution and private capital have led to a boom in the independent registered investment advisor (RIA) channel. What do entrepreneurial advisors need?

The second amendment to the revocable trust agreement directed the following distributions: • 2 million dollars to the trustee of the MCC Trust, to be held for Maria’s benefit. The MCC Trust agreement included terms about the distribution of trust assets: 3.2. Number 8860726. Administration of Trust Estate for Beneficiary.

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts. As a whole, these regulations introduce significantly more complexity to the process of taxplanning around retirement accounts, particularly after the death of the account's original owner.

These services often include recommendations on investments, financial planning, retirement, Social Security, Medicare, taxplanning, and other wealth-related topics. He also has considerably less of a compliance, operational, and administrative burden because he is not taking custody or discretion of his clients’ assets.

These include legal fees, administrative costs, audit expenses, compliance costs, and operational fees. A qualified tax advisor can help you: Navigate complex tax reporting requirements , including K-1 forms for private equity, hedge funds, and real estate partnerships. This article is a product of Harness Tax LLC.

With proper planning and professional advice, you can enjoy a secure and fulfilling retirement while effectively managing your healthcare costs and ensuring peace of mind for the future. Pillar 3: TaxplanningTaxplanning is indispensable for optimizing your retirement finances and safeguarding your wealth for the future.

With that said, detailed records, including receipts and mileage logs, are essential for substantiating all deductions and ensuring IRS compliance. Travel nursing and taxes Travel nurses face a specific tax challenge, primarily due to their pay structure and the concept of a “tax home.”

The impact is particularly pronounced for C corporations, where asset sales can trigger double taxationfirst at the corporate level when assets are sold and again when the proceeds are distributed to shareholders.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content