This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

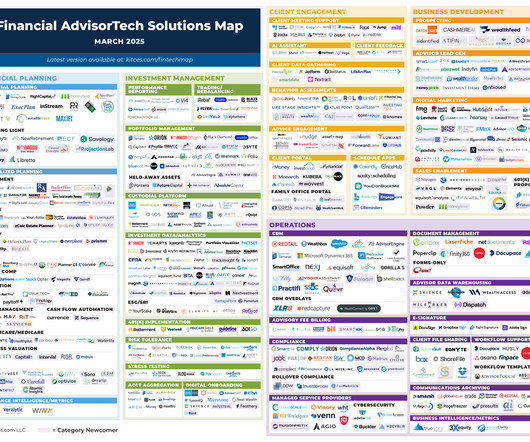

Welcome to the November 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

Just a few decades ago, giving financial advice was largely a manual process – printing lengthy financial plans, processing physical checks, and managing paper files. AI offers exciting possibilities as a brainstorming partner, editor, and copywriter.

After all, it can feel odd to create an estate plan that will impact a client’s grandchildren… when those grandchildren may be older than the advisor themselves! But walking through every page of a financial plan line by line could take up an entire afternoon and often isn’t necessary.

David Handler provides insights into the essential role financial advisors play in estate planning, why it's important to have an estate plan and the importance of communication and education within families about wealth management.

The penalty calculations were complex and difficult to estimate, and the provisions were poorly communicated to those affected. This lack of clarity made retirement planning significantly more challenging. Now that the WEP and GPO have been repealed, retirement planning will be significantly easier going forward. Read More.

To sustain firm growth, financial advisors often face a dilemma: to focus on what originally drew them to the profession – like financial planning – they often must first do an extensive amount of business development. Even those who do have an interest in marketing may find it challenging to dedicate the time to do it well.

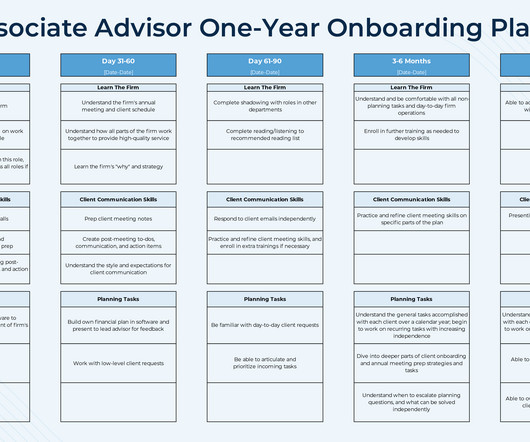

For smaller firms – especially those with little to no experience onboarding new advisors – creating a well-paced financial plan can feel daunting. However, a structured and flexible onboarding plan not only helps an associate advisor ramp up efficiently but also ensures a smooth transition into an autonomous and fulfilling role!

Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning. Pricing the impact of financial planning can be challenging, because many of its benefits – like peace of mind – are intangible, compelling in value but difficult to match with an exact price.

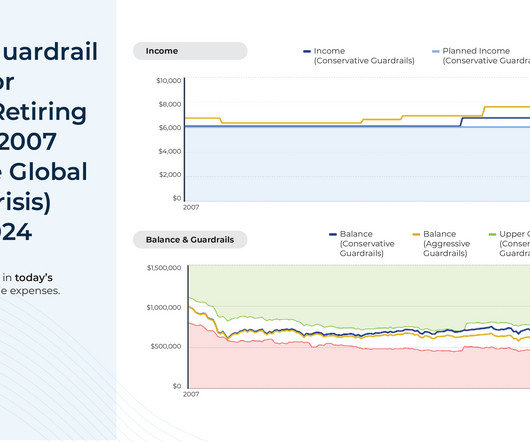

Monte Carlo simulations have become a central method of conducting financial planning analyses for clients and are a feature of most comprehensive financial planning software programs. However, the results of these simulations generally don't account for potential adjustments that could be made along the way (e.g., Read More.

Also in industry news this week: While many financial advisors are paying close attention to the potential extension of sunsetting measures within the Tax Cuts and Jobs Act (TCJA) in the coming year, legislation related to retirement savings could be on Congress' agenda as well Fidelity is planning to change the default for its existing RIA non-retirement (..)

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a report from Cerulli Associates found that, amidst an industry-wide trend towards comprehensive financial planning and away from pure transaction-based investment management, asset-based fees currently represent 72.4%

In this episode, we talk in-depth about how Kevin's firm's new hire training program ramps up through the first 6 months, starting with an initial 90-day stage that uses standardized case studies to teach the firm's financial planning process and how to review and input data into the firm's systems, followed by a second 90-day stage that builds new (..)

A better way to implement and communicate fee increases may be one that is centered around providing more value to the client in exchange for the higher fee. Read More.

Advisor-focused AI meeting note solution Jump has completed a $20 million funding round, which reinforces its status as the emerging market leader in the crowded AI meeting note category – a status that may only increase from here if AI meeting notes, like most established AdvisorTech categories, evolves into a "winner-take-all" market where (..)

Also in industry news this week: While RIA M&A deal flow hit record levels in 2024 (both in terms of volume and the speed of completing them), firm valuations saw relatively modest gains In its latest annual regulatory oversight report, FINRA joined the SEC in flagging the potential risks to firm and client data from the use of third-party vendors (..)

So, whether you're interested in learning about the difference between estate and legacy planning, how to engage in deep legacy planning conversations with clients, or using intimate client events to attract new prospects, then we hope you enjoy this episode of the Financial Advisor Success podcast, with Vanessa N. Read More.

While some of these programs still exist, the role of an associate advisor has evolved alongside the broader financial planning profession. Some programs emphasize technical expertise, while others focus on communication skills needed to engage effectively with clients.

Recession Concerns & Market Volatility: How Financial Advisors Should Communicate With Clients As financial advisors , youre well aware that so far the 2025 financial market has been more unpredictable than a toddler. Why Proactive Communication Matters If theres one thing more unpredictable than the markets, its human emotion.

Financial plans play an important role for both clients and advisors, as they not only help clients gain a clear perspective of their current financial position, but also provide advisors with a systematic way to organize their analyses and communicate their recommendations to the client.

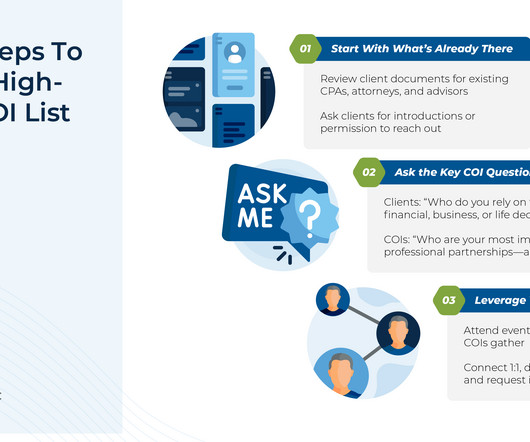

In this article, Tiffany Charles, Chief Growth Officer at Destiny Capital, and Kitces.com Senior Financial Planning Nerd Sydney Squires offer a thoughtful framework for approaching COI relationship development with greater intentionality. The first meeting is focused on building rapport and conducting an initial assessment.

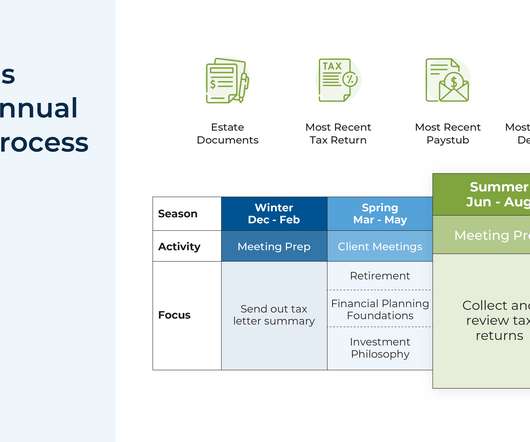

A common service model for many financial advisory firms is to schedule annual client meetings throughout the year where the advisor meets with each client in the month they started working with the firm, and conducts a comprehensive review of all planning topics for the client.

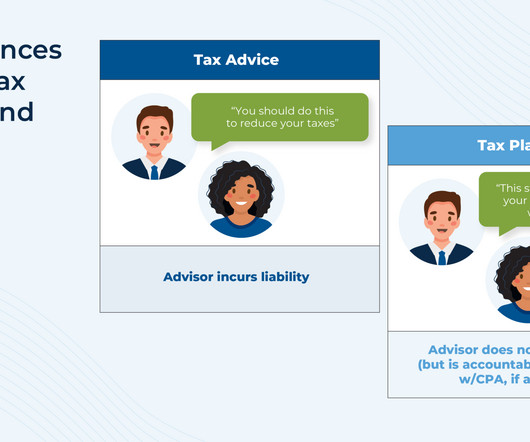

In recent years, financial advisors have increasingly embraced tax planning as a core element of delivering value to clients. But as the profession has evolved toward more holistic planning, tax considerations have likewise expanded into more areas of advice, including Roth conversions, charitable strategies, and small business structuring.

However, when these aspirations are delayed or blocked by senior advisory firm partners who choose to delay their retirement plans, it can leave younger advisors frustrated and in a place of uncertainty about their futures with their firm.

There's an old joke in the financial planning industry that the ideal client is "anyone with a pulse". In this 153rd episode of Kitces and Carl, Michael Kitces and client communication expert Carl Richards discuss how advisors can navigate the challenge of managing underpaying clients.

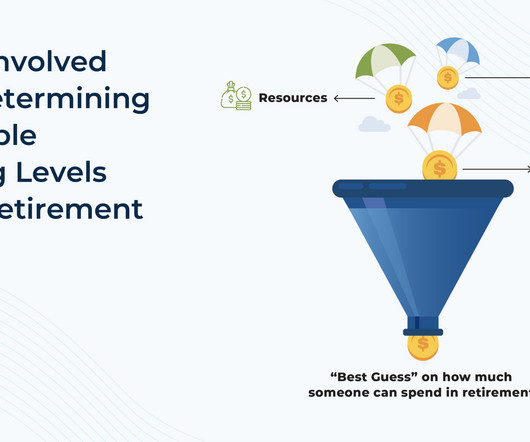

Over the past few decades, advicers have used Monte Carlo analysis tools to communicate to clients if their assets and planned level of spending were sufficient for them to realize their goals while (critically) not running out of money in retirement.

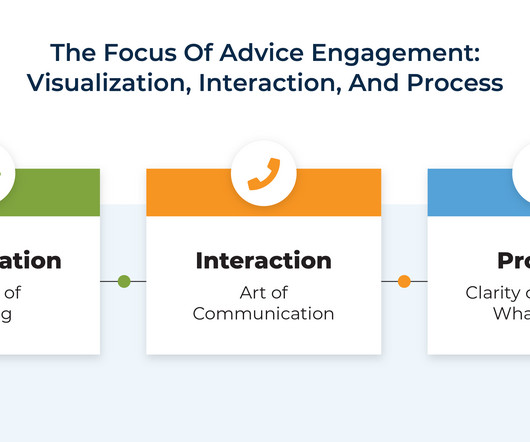

Whether planning for retirement, investing in volatile markets, or managing tax implications, clients are often presented with intricate information that can leave them overwhelmed, confused, and anxious, undermining their ability to make informed decisions.

The increasing popularity of financial planning has led to a growing awareness of how important managing finances and planning for the future can be. For most financial advisors today, a website is a critical tool that allows them to market their services and communicate their fees to potential clients.

The traditional way that most financial planning has been offered was for an advisor to create "The Plan": a comprehensive document outlining a client's financial strategy that was delivered either on a one-time basis or updated annually.

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirement planning.

Since the emergence of Artificial Intelligence (AI) in the mainstream technological landscape, conversations about which areas of the financial planning industry would be most likely impacted by AI have proliferated.

annual plan reviews) to their current clients, they will continue to prospect and onboard new clients as well. a client service associate to handle various administrative and client communication tasks, or a paraplanner or associate advisor to work on more planning-centric issues such as building out drafts of financial plans).

Financial planning is inherently complex, especially when it comes to data gathering, analysis, and crafting well-reasoned recommendations. investment strategies or tax planning) – can reduce cognitive overload for clients and keep meetings on track. The goal isn't simplicity for its own sake, but clarity.

Estate planning. Succession planning. In the race to stand out, many financial advisors have expanded their service offerings. Tax strategies. Insurance consulting. The thinking is simple: More services signal more value.

Also in industry news this week: In the continued absence of formal SEC guidance on advisory firm use of Artificial Intelligence (AI), many firms are taking a curious, but cautious, approach toward adopting AI-powered tools A recent report identifies the growing total wealth controlled by women in the U.S.

About a decade or so ago, one of the most pressing issues facing the financial advice industry was the threat of an imminent deluge of advisor retirements coupled with a paucity of succession plans to transition clients to the next generation.

What's unique about Eric, though, is how he leverages a custom-built financial planning assessment he calls their Financial Prosperity Index, which he gives to both prospective and ongoing current clients so that they can better understand their financial health, target the financial planning domains where clients need the most help, and even more (..)

In addition, Atkins' arrival could also mean the end of the pending RIA outsourcing and custody rules proposed under Gensler, a reduced focus on monitoring advisors' off-channel communications, and a new regulatory framework for digital assets.

Instead, acknowledging their ambivalence as a natural part of the decision-making process can help create space for them to discover the value of financial planning on their own. One effective way to facilitate this self-discovery is through self-persuasion questions.

He explains how they identified which clients were no longer profitable, developed an alternative service model to offer these clients, mentally prepared for the transition, and effectively communicated the changes. staff time, technology, and custodial fees) and indirect costs (e.g., rent, marketing, and training).

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content