This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Training programs for new financial advisors have traditionally followed a sales-focused, sink-or-swim approach that primarily paid on commission for product sales. While some of these programs still exist, the role of an associate advisor has evolved alongside the broader financial planning profession. Read More.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week’s edition kicks off with the news that the CFP Board of Standards launched its 1st ad campaign, dubbed "It’s Gotta Be A CFP", following its transition to a 501(c)(6) organization.

However, these agreements can also be unduly restrictive towards employees, limiting their ability to advance within their chosen industry, which is especially problematic in skilled professions that might have required years of education and training just to enter in the first place.

Importantly, we do not accept sales commissions or any compensation beyond what is directly agreed upon with our clients. No Minimums, Maximum Accessibility: Unlike traditional financial advisors, being a Garrett Advisor means that we have no income or investment account minimums for hourly engagements.

Fee-Only, Flat-Fee Financial Planners: Transparent, Unbiased, and Cost-Effective A fee-only financial planner charges a fixed fee for financial planning services, regardless of the size of your portfolio. Unlike AUM-based advisors, they do not earn commissions or take a percentage of your investments.

Effective content marketing focuses on education and value rather than overt selling, strengthening audience connections and increasing conversion potential. Creating Educational Webinars and Online Workshops In todays online world, giving good financialeducation is a great way to connect with potential clients.

The primary fee structures are: Fee-only : Advisors only receive payment from their clients for the services they provide, not receiving any commissions or other incentives from product providers. Fee-based : This structure is a blend of fees and commissions. Requirements include: Education: Completion of nine college-level courses.

The advisors can be differentiated based on the fee structure they use to charge fees such as fee-only, commission-only, hourly-fee, monthly fee, etc. Lastly, if you cannot stretch your budget to hire multiple financial advisors, it may be better to hire only a single financial advisor.

are paid through a commission. The individual or company is registered with either the Securities and Exchange Commission (SEC) or a state securities regulator. To find out if you are working with an actual investment adviser representative, go to the Securities Exchange Commission’s Investment Adviser Public Disclosure database.

They may charge for their services either on a commission basis or hourly rates. However, our advice is to trust financial planners who either take a flat annual fee or charge per hour for managing your portfolio instead of charging a commission on every stock they buy or sell. How to Compensate Financial Advisors?

These include – Education – Some self-trained Financial Advisors have spent years in the industry and gained insights into this trade and have done well for themselves. However, this isn’t what you are aiming for and to find your foot in the industry you will need the right kind of education.

Taking on good debt means using a strategic borrowing strategy to help pursue wealth-building opportunities, such as homebuying or higher education. Insurance brokers sometimes push whole life insurance policies heavily because of their large commissions and kickbacks. Bad debt includes credit card debt and personal loans.

These professionals work independently or under the umbrella of financial institutions and are specialized in guiding clients through the intricacies of financial planning and investments. Their compensation often comes from (1) commissions on transactions based on advice provided or (2) fees for financial plan construction.

Department of Veterans Affairs aimed at making education, healthcare, life insurance, mortgages, and retirement more accessible for those who have served. Not only will the lifestyle of military members differ from civilian clients, but there many financial benefits available to veterans from the U.S. Education Benefits.

Watch as all h&#@ breaks loose discussing the question of broker vs. financial advisor, commissions, fees, value, and more! The advisors made the point that the cost of insurance can’t be separated from the “cost of service” or the commission the agent makes. The commission is the commission. Doug Twiddy.

Necessary Qualifications and Skills It is critical to attain relevant education, experience, and certification for becoming a SEBI Registered Investment Advisor. Another pathway is obtaining a professional qualification by obtaining a CFA (Chartered Financial Analyst) Charter from the CFA Institute.

While there are various types of finance professionals who offer financialadvice and services falling under the general financial advisor category, it should be noted that they differ significantly. Securities and Exchange Commission (SEC) if they manage $100 million or more in assets.

So, when it comes to handling your finances, it’s natural to think that the information you hear repeatedly is the best advice to follow. After all, plenty of people are making a living sharing financialadvice online (we refer to them as “influencers”). Shouldn’t you listen to what they have to say? Well, no… not necessarily.

Sites like Facebook, LinkedIn, and Twitter allow advisors to share valuable content, engage with followers, and show their expertise in the financial industry. When financial advisors share helpful articles, blog posts, and videos on social media, they can show their knowledge and give good financialadvice.

The move to financial planning transparency is aflame! in all aspects of financialadvice, with a special focus on Advice Only, Flat Fee, and Hourly service models. Specific examples: Educatingfinancial advisors of all business models (AUM, fee only, commission, etc.) Client advocacy. Here are tips.

AI-powered chatbots are changing how clients access financial support. Chatbots offer 24/7 assistance and instant advice for multiple, complex queries. These chatbots can be accessed from smartphones, offering financialadvice on the go. Your emotional intelligence affects your financial choices. Heres why: 1.

But I gotta start with your education. But yeah, I was making commission at that point in time. So when I was a salesperson at Business week, I sold more ads than anybody, and I made $2 million commission when I was 29 years old. I think people should really, you know, be educated about money, think about their money.

Rostad is currently focused on what he sees as our best chance for meaningful reform: getting the Commission to revise the Form CRS disclosure so that it provides a clearer explanation of the different business models of broker-dealers/wirehouses, on the one hand, and fiduciary RIAs registered with the SEC on the other.

Betterment is great at reducing any taxes you have to pay on your investments, and they work with you to give you the best financialadvice through their algorithms. Most brokerages no longer charge trading commissions which is a huge saving for us! They then earn a commission on the products that they sell.

To see this term blurred with the top advisor definition, it makes me mad because it implies that advisors who are selected on the basis of production – and this gives me the sense that this ranking had a lot to do with precisely that – are the best financial advisors. Selling a product does not equal financialadvice.

And that’s why I’m writing this blog; because I feel that financialadvice rendered by the hour is a great thing for the American public (for the reasons we’re going to discuss below). What are the drawbacks of charging an hourly fee for financialadvice? I was managing their money in.

Crafting Your Personalized Financial Plan: A Step-by-Step Guide Now that we’ve covered how to think about financial planning, let’s go into step-by-step detail on how to create a personalized financial plan. Please note that the following is for informational purposes only and that this is not financialadvice.

Ever since the beginning of his 20+ year long career, Scott has pursued his mission of delivering high quality financialadvice in a low cost and unbiased way. Robert is also an Instructor of CFP® Coursework for the College of Financial Planning Online and on Campus at Kennesaw State University.

It comes down to financial literacy and investor education. Ever since the beginning of his 20+ year long career, Scott has pursued his mission of delivering high quality financialadvice in a low cost and unbiased way. It’s a problem and it seems like the SEC is just picking and choosing who to go after.

Are commissions bad? In Salaske’s view, education is the issue because annuities are sold products. Are commissions bad? Salaske said he wonders if the people who really need them are getting sold annuities that don’t produce a huge commission. Macchia says that agents would be happy to take even a small commission.

JR: Well, one of the things that Robert, you mentioned last week, and I totally agree with, is that a problem with financial planning being regulated as it is today by the SEC, is that there is no educational requirement to become a financial planner. Salaske: What is an investment advisor?

The CFP Board promotes a faux fiduciary standard that does not require its members to disclose potential conflicts of interest in writing and that does not require them disclose the percentage or amount of commission its members may receive from the sale of insurance products with opaque commissions.

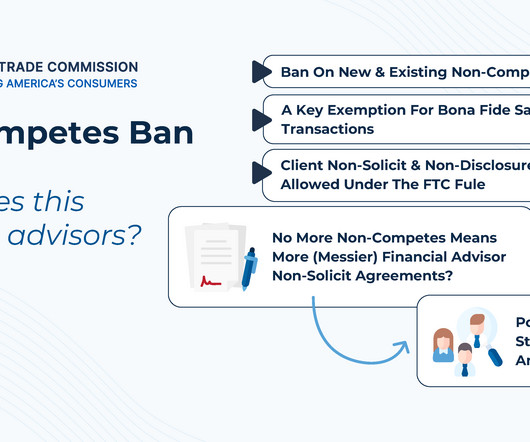

the Department of Labor's Retirement Security Rule and the Federal Trade Commission's ban on most non-compete agreements, both of which are currently blocked by courts) likely to be tabled under the new administration.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content