This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At The Money: The Right Way to Spend Your Money in Retirement (July 16, 2025) One of the biggest challenges of retirement is actually spending your money! She joins Barry Ritholtz to discuss what you need to know about planning for retirement. She is the Director of Personal Finance and RetirementPlanning at Morningstar.

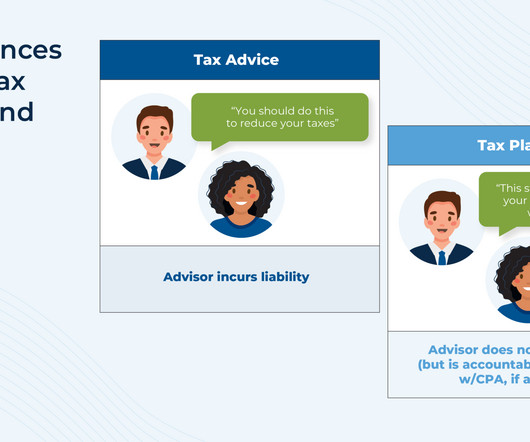

In recent years, financial advisors have increasingly embraced taxplanning as a core element of delivering value to clients. Despite this growing interest in tax conversations, most advisors are still quick to distinguish their services as "taxplanning", not "tax advice" – a distinction largely driven by liability concerns.

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Daniel is the CEO of WMGNA, a hybrid advisory firm based in Farmington, Connecticut, that oversees approximately $270 million in assets under management for 200 client households. My guest on today's podcast is Daniel Friedman.

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirementplanning, estate and taxplanning and mortgage refinancing. trillion annually over the next decade as part of the great wealth transfer, a new report finds. trillion annually.

The report suggests this might be due in part to increased RIA valuations and the assumption of some firm founders that next-generation employees won't be financially able to buy out the firm from them, though additional data indicates that many firms don't have career paths in place that could help next-generation advisors envision their path to firm (..)

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that SIFMA, which represents broker-dealers, investment banks, and asset managers, released a white paper that argues that CFP Board "increasingly functions as a de facto private regulator for CFP certificants" and proposes that CFP (..)

Podcasts Khe Hy talks with Christine Benz author of "How to Retire: 20 Lessons for a Happy, Successful and Wealthy Retirement." podcasts.apple.com) RetirementRetirement is a great time to do some creative taxplanning. humbledollar.com) Should you take advantage of super-catch-up retirement provisions?

podcasts.apple.com) Brendan Frazier talks with Tony Hixon author "Retirement Stepping Stone: Find Meaning, Live With Purpose, and Live a Legacy." trillion in assets. blogs.cfainstitute.org) Taxes When it comes to taxplanning, what you need to know about the BBB. thinkadvisor.com) Why succession plans matter.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. GET STARTED 1.

based accounting firm, is taking a page from large registered investment advisors by bringing together taxes and wealth management. Minopoli, who is also a partner in the new RIA, had previously been the chief investment officer of a team managing a $30 billion portfolio for the Knights of Columbus Asset Advisors.

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

RIA Edge Podcast: Schwab’s Jalina Kerr on How Resilient RIAs Can Turn Market Volatility Into Growth RIA Edge Podcast: Schwab’s Jalina Kerr on How Resilient RIAs Can Turn Market Volatility Into Growth Jalina Kerr of Charles Schwab shares how the most adaptive firms are expanding beyond portfolio management, into areas like estate and taxplanning.

Insurance and financial fee deductions Insurance represents a necessary expense for protecting your business assets and operations, with premiums for various types of coverage qualifying as fully deductible business expenses. To maximize tax benefits while maintaining healthy cash flow, businesses should thoroughly understand these options.

Consider tax-advantaged options , such as ESOPs, which allow for capital gains tax deferral when proceeds are reinvested, or stock sales that may qualify for preferential long-term capital gains treatment. The most common exit options include mergers and acquisitions, asset sales, stock sales, and employee ownership plans.

justincastelli.io) Taxes Some speculation on what is next for the TCJA. kitces.com) Taxplanning and wealth management go hand-in-hand. downtownjoshbrown.com) How tax deferment can backfire. advisorperspectives.com) 7 areas where advisers may be falling short with retired clients.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well.

At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations. This guide consolidates what we’ve learned to help you refine, update, or pressure-test your current retirement and estate strategy with confidence.

Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B is joining the trend toward combining wealth management and taxplanning by merging with Brookfield, Wis.-based Mergers and partnerships between RIAs and tax firms have moved beyond sharing client referrals to bringing the practices into one firm or relationship.

RetirementPlanning: Looking Beyond the Basics For 2025, it’s essential to think beyond the standard “maximize your 401(k)” advice. While that remains important, consider diversifying your retirement strategy. This can significantly impact your retirement savings trajectory.

Donor-advised funds (DAFs) have emerged as powerful tools that deliver this exact combination, providing immediate tax advantages while offering flexibility to recommend grants to qualified organizations over time. Table of Contents What Are Donor-Advised Funds, and How Do They Work?

Unexpected events can derail your progress toward your goals and even your financial security if you don’t have a plan for managing them. Financial planning should ideally involve every area of your financial life because they are all interrelated. Losses in one asset class may be balanced out by gains in another.

Tax Strategies for High-Income Earners in 2025. In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations. From maximizing deductions to managing capital gains, we’ll cover everything you need to know about smart taxplanning.

High-net-worth individuals are typically categorized as those with over $1 million in liquid assets. million or $750,000 in investable assets to meet certain regulatory definitions. are some high-value assets that can be vulnerable to theft and damage. These structures separate your personal assets from the business.

These professionals may charge a fixed fee or a percentage of your assets under management (AUM). You could be lying in bed at night and suddenly thinking about changing your asset allocation. Each comes with its own rules, returns, fees, lock-ins, and tax treatments. When you self-invest, you cut that middle person out.

Benefits of Waterfall Wealth Management Managing significant assets can be complex. Key benefits include: Ensuring essential financial obligations are met first – Taxes, estate planning, and retirement savings take precedence. Strategic long-term planning – Provides a roadmap for surplus wealth allocation.

In this article, well examine the most effective end-of-year tax strategies to help maximize your deductions and reduce your taxable income. These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. Available to taxpayers aged 70.5

What are tax-efficient alternative investment structures? Tax strategies for high-income filers How Harness can help FAQs What are alternative investments? Alternative investments encompass a broad range of assets beyond traditional stocks, bonds, and cash.

While most taxpayers dont need to worry about estate and gift taxes, having significant assets can make them a challenge. Also, like most UHNW individuals, you may have income from several sources like investments, real estate, and business interests that may require special taxplanning. And, if the U.S.

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. Start planning early. And the best way to do that?

Whether it’s investment planning, retirementplanning, tax strategy, estate management, insurance planning, or holistic money management, the CFP designation proves that you can deliver advice that is both competent and client-centric.

Tax-loss harvesting is especially useful during volatile market conditions, as price fluctuations can create opportunities to realize losses without significantly disrupting an investor’s overall portfolio strategy. The tax treatment of this loss will depend on how long the asset has been held.

Internal Revenue Code (IRC) allows businesses to deduct the full purchase price of certain depreciable assets, including vehicles, in the year of purchase rather than depreciating them over time. The key benefits Reduced tax liability: So long as youre paying reasonable wages to your child, you can lower overall tax liability.

A financial plan looks at your assets and liabilities, short-term and long-term needs, as well as your goals to structure your finances in a way that suits you. Want to retire early? TaxPlanning. A proactive taxplan can save you thousands of dollars every year. Emotional Investment Choices.

This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on taxplanning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments. Different types of income maintain their distinct tax treatment as they pass through to a partner.

Foreign accounts Failure to report foreign bank accounts, financial assets, or income can result in severe penalties and trigger an audit. The IRS has intensified its efforts to combat offshore tax evasion, and unreported foreign holdings are a major red flag, especially with increased information sharing between countries.

Related: Planning for Older Clients and Those with Disabilities Many GRATs include a so-called “swap” power in which the grantor is permitted to substitute assets of equivalent value with the GRAT. Prior case law in the Southern District of New York (Morales v. Quintiles Transnational Corp. 2d 369 (S.D. 1998) and Donoghue v.

A good rule of thumb is to set aside at least 30% of every payment you receive to cover your estimated tax obligationshowever, this percentage may need to be adjusted based on your individual tax bracket. On the whole, its advisable to consult a tax adviso r to develop a dependable taxplan.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. One of the Roth IRA’s most compelling features?

Whether clients support the policies with cash gifts or split-dollar, the discussion of options will necessarily involve a combination of insurance planning, taxplanning, income and gift tax-oriented wealth transfer planning and investment planning.

Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Many people end up paying taxes twice. To calculate the tax-free percentage: Your Total Basis (e.g. Yes and no.

And as 2024 draws to a close, we wanted to highlight 24 of the most popular and insightful articles that were featured throughout the year (that you might have missed!).

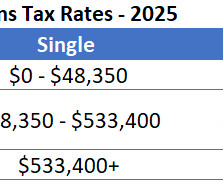

What is a capital gains tax? When you sell an asset like a stock or a home, your gain could be taxable. The tax rate will depend on several factors, such as your holding period, type of asset, and your taxable income for the year. What is a capital gains tax? Single and married filing jointly are the most common.

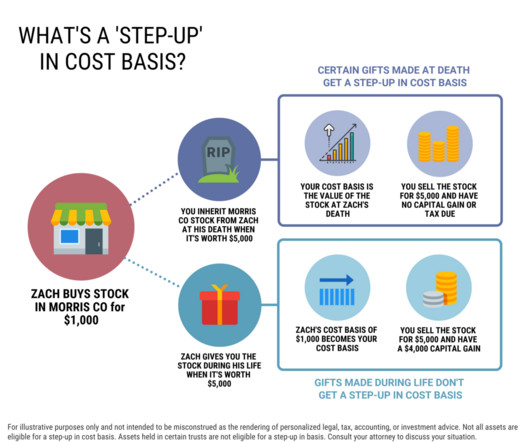

A step-up in basis is a tax advantage for individuals who inherit stocks or other assets, like a home. Heres how stepped up cost basis works on stock and other assets at death. Understanding step-up in basis at death If youve received an inheritance you may have questions about the tax treatment of certain assets.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content