This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Financial advisors have a wide range of strategies at their disposal to create financialplans for their clients. This strategy is valuable because it generally allows for higher initial withdrawal rates than more static approaches that don’t accommodate clients willing to adjust their spending in retirement.

Assuming that you have a financialplan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. Do nothing. Focus on risk. Look for bargains.

Interest rates remain a significant factor in financialplanning, affecting everything from mortgage rates to investment returns. The past few years have taught us valuable lessons about the importance of building resilient financial strategies that can weather various economic conditions.

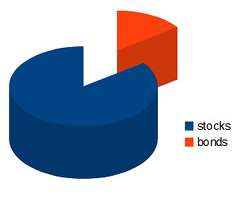

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Why stocks and bonds belong in a diversified portfolio Investors have different needs, risk tolerances, time horizons, and financial situations which should be considered in an assetallocation.

This is also what makes retirementplanning so difficult – you effectively lose an asset in your portfolio when your income stops or declines. And this is why I’ve become such a big advocate of defining our durations within our financialplans.

Generally, investors don’t increase their risk profile as they move through retirement. Allocation choices also shouldn’t be based on the notion that dipping into principal derails a financialplan. Assetallocation Generally, dividend stocks tend to be older, more mature companies.

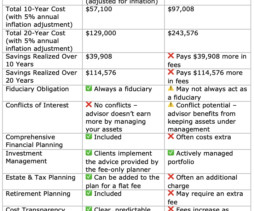

If youre searching for a fiduciary financial planner, flat-fee financialplanning, or the best alternative to AUM-based advisors, this article will help you decide which model is right for you. Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective.

FinancialPlanning is vital. If you don’t have a financialplan in place, or if the last one you’ve done is old and outdated, this is a great time to review your situation and to get an up-to-date plan in place. Do it yourself if you’re comfortable or hire a fee-only financial advisor to help you.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financialplan should be the basis of your strategy. Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. Take stock of where you are. Take stock of where you are. Costs matter. Photo credit: Flickr.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

We are thrilled to announce that our Wealth Advisors, Edzai Chimedza, CFP® and Franklin Gay , CFP®, EA will be leading two FinancialPlanning Seminars at Nova Southeastern University. Contact us today, and let’s discuss how we can assist with your specific financial situation. appeared first on www.tobiasfinancial.com.

What Does a Financial Advisor Do? A financial advisor provides personalized guidance to help manage and grow your wealth. Their role extends beyond investment managementthey can help with: RetirementPlanning : Structuring your assets to support your desired lifestyle. Optimizing tax-efficient retirement income.

The simple answer is that the short-term movements of the stock market should be irrelevant to your financialplan assuming you have a well constructed temporally diversified portfolio. Insurance is largely optional and plan dependent, but I think of the other 4 time horizons as essential. 2) Stock market gambling.

Take advantage of tax-advantaged retirement accounts such as 401(k)s, IRAs, and Roth IRAs to maximize your contributions and benefit from tax-deferred or tax-free growth. Learn more about retirementplan options here. Aim to contribute as much as you can afford to these accounts each year to accelerate your retirement savings.

Track income, expenses and build in budgeted items for future financial goals. Meeting with a qualified financialplanning professional can help you begin building positive and lasting behaviors.?? . Take Advantage of RetirementPlans and Matching Contributions. Consider the following example below:?? .

Earning the CFP designation requires a rigorous course of study covering investment planning, income taxation, retirementplanning and risk management. The Certified Financial Planner course is the perfect course to achieve all topics related to finance. For e.g. saving for a home, retirement, or Higher education.

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Unfortunately, headlines often leave investors wondering what the news means for their portfolio and financial outlook. A downturn before or just after retirement is especially damaging.

A point we've been making here for ages is that with an adequate savings rate, appropriate assetallocation and the ability to avoid succumbing to panic, an investor should be able to have retirementplan success as defined above. If you're 60, think you want to retire at 65 and need $1.4 I'd argue not much.

Understanding the importance of assetallocation is like building a strong financial foundation. It’s all about spreading your investments across different asset classes, like stocks, bonds, and real estate, to manage risk and maximize returns. This helps manage risk and maintain your desired balance of returns.

An investor needing something close to equity market returns for their financialplan to work needs something of a "normal" allocation to equities. Not that 20% is universally wrong, not everyone needs close to equity market returns for their financialplan to work. Maybe that's 50% or maybe 60% but it's not 20%.

You can also get information on your performance and assetallocation. This will help you to create an assetallocation that will get you where you need to go with your investments. It can be used to help you with your assetallocation, at least based on the investment options that your plan includes.

Intermediate and Short-Term Goals Begin by distinguishing between your long-term, intermediate-term and short-term financial goals. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Your risk tolerance will influence your investment strategy and assetallocation.

James and Pamela’s Big Dream Excerpt from The Smart Person’s Guide to FinancialPlanning & Investments: A Simple and Straightforward Approach to Understanding Your Personal Finances By Michael J. Their retirementplan is strong, their kids are independent, and they are debt-free.

Financialplanning and advice from a professional go hand in hand. If you have ever felt stuck while trying to make sound financial decisions, hiring an advisor can be helpful. Financialplanning can be cumbersome and take a lot of your time. Assetallocation requires constant monitoring.

These professionals meticulously assess your financial situation, income level, and retirement goals to tailor personalized strategies. For instance, they can guide you on leveraging employer-sponsored retirementplans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts.

Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages. Your investment strategy determines the target percentages for each asset, often based on your risk tolerance, investment goals, and time horizon. Click to compare vetted advisors now.

The Financial Education Certification Series XVIII course offered by NISM is a text-based self-study course that contains 12 modules. The topics covered in this course are key concepts in personal finance, financialplanning & budgeting, savings, investment in securities, insurance, pension, retirement, and borrowing.

Intermediate and Short-Term Goals Begin by distinguishing between your long-term, intermediate-term and short-term financial goals. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Your risk tolerance will influence your investment strategy and assetallocation.

The decision to go full All-Weather needs to be a financialplanning decision not a reactionary decision to a bear market. Reacting in the middle of 2022 after learning too much was allocated to risk assets? Reacting in the middle of 2022 after learning too much was allocated to risk assets?

FINANCIALPLANNING What is Portfolio Rebalancing? Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. For example, you can shift money between asset classes to reflect market changes and work with your financial adviser to create a diversified strategy. appeared first on Park Place Financial.

What Does a Financial Advisor Do? A financial advisor provides personalized guidance to help manage and grow your wealth. Their role extends beyond investment managementthey can help with: RetirementPlanning : Structuring your assets to support your desired lifestyle. Optimizing tax-efficient retirement income.

The following advisors are pure fiduciary financial advisors who serve small investors. Transform Retirement www.transformretirement.com Avg account size: Approx. TradeWinds, LLC www.tradewinds.global Avg account size: $270k Services: We offer digital assets for people who are interested and may already hold on their own.

While modeling can’t fully insulate an investor from the impact of short-term events (nothing can), a detailed analysis can help investors understand the probability of outcomes by stress testing a financialplan to better assess the likelihood of success over the long-term. Plans that don’t bend, break. Assetallocation.

Here is a 10-step financial checklist to spruce up your financialplan: Consolidate summer debt : First, if you are having trouble paying off credit card debt, refrain from using the card until you regain control. Then, develop a strategic repayment plan. Important Note.

Maintaining a balanced approach is critical in financialplanning. Overindulgence in information can lead to poor decisions, and excessive monitoring of your retirement account balance can result in stress. Checking your retirement account balance too often can have a psychological impact on you.

If you are over-tilted on one side of your financial boat, it could tip over. Risk Tolerance: What is your assetallocation? If you are close to retirement, and you have too much exposure to equities, a retrenchment in the stock market could delay your retirementplans by years.

The reality is that securing your financial stability for the golden years is a key objective that these challenges shouldn’t overshadow. The answer lies in smart and strategic retirementplanning. Gone are the days when retiring at 60 was a one-size-fits-all goal. So, how do we tackle this?

Here are 5 signs it might be time to hire a financial advisor. In today’s complex financial landscape, managing your money can be challenging. From retirementplanning to market volatility, equity compensation, family expenses, and major life transitions, it’s easy to feel overwhelmed with financial responsibilities.

Below are five benefits of working with a financial advisor and how they can help you retire with more wealth: 1. Deciding what types of investments to allocate your funds into and in what proportion can significantly impact the growth and security of your portfolio.

According to the interwebs, this is the All Weather assetallocation and the funds that capture the portfolio; Equities 30% VTI Long Term Treasuries 40% VGLT Intermediate Treasuries 15% VGIT Commodities 7.5% PDBC Gold 7.5%

When it comes to managing wealth and planning for a secure financial future, the services of financial professionals, such as financial advisors or wealth managers, are invaluable. Table of Contents What Services Does a Financial Advisor Provide? Are Robo-Advisors a Good Alternative?

While the future can be unpredictable, the five to ten years before retirement are a great time to get a realistic picture of your lifestyle costs. At that point, you likely have a clearer understanding of what it takes to maintain your current standard of living, and that can be the starting point for your retirementplanning.

Due to the complex and diverse range of their financialassets, these individuals also require specialized high-net-worth financial planners and personalized investment management tailored to meet their specific needs. 2023 may see several changes with respect to retirementplans, Social Security, etc.,

Opening a gold or silver Individual Retirement Account (IRA) is another way wealthy individuals invest in gold. This can be a tax-efficient vehicle for retirementplanning and wealth transfer. These strategies primarily involve assetallocation , tax planning, estate planning, and retirementplanning, among other things.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content