This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: In the continued absence of formal SEC guidance on advisory firm use of Artificial Intelligence (AI), many firms are taking a curious, but cautious, approach toward adopting AI-powered tools A recent report identifies the growing total wealth controlled by women in the U.S.

Also in industry news this week: 43% of wealth management firms are frustrated with the effectiveness of their CRM software, spurred on by challenges with integrations and workflows, according to a recent survey The Social Security Administration this week announced a 2.5% Read More.

Which, according to Kitces Research on Advisor Productivity, can lead to higher productivity for advisor teams (but can require an investment in staffing and higher-end planning services to meet their complex planning needs).

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For some clients, “risk” maybe something exciting or daring that they enjoy and not something they generally avert from.

Also in industry news this week: How Goldman Sachs’ RIA custodial platform is leveraging the resources of its parent company as it seeks to build momentum amidst a highly competitive environment among custodians How NASAA has changed the substance and/or scoring of the Series 63, 65, and 66 exams From there, we have several articles on college (..)

Start planning early. Yet far too many professionals delay the planning process. The goal of this article isn’t to scare you. Even if you don’t plan to retire unusually early, starting your retirement planning now can dramatically improve your options later. And the best way to do that? Doing it right?

The financial planning industry is constantly undergoing change. This article will discuss some of the most pivotal financial planning industry trends to watch out for this year. They would also want to plan how and when to withdraw funds since different accounts come with different tax implications.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

It is essential to choose investments that match your risk appetite to avoid unnecessary stress and surprises later. A financial advisor can help you understand your investment risktolerance. This article will focus on the risks of investing, how they impact you, and what you can do to determine your risk appetite.

In this article, we will explore three popular savings and investment options: 529 Plans, Roth IRAs, and Real Estate. Each has unique benefits and drawbacks, and understanding these can help you decide which fits best with your financial situation, risktolerance, and goals.

During recent conversations, I’ve come across several people unfamiliar with the concept of fee-only financial planning, let alone considering it as a feasible choice. To shed light on this, I want to articulate the distinctive approach we use at MainStreet Financial Planning.

In this article, we’ll break down the concept of waterfall wealth distribution, its benefits, and how it compares to traditional investment strategies. We’ll also explore the role of income tiers, provide real-world case studies, and highlight key considerations when implementing this strategy in your financial plan.

Here’s an outline of key considerations; the rest of this article discusses these items in detail. Exercise strategy: Timing: Consider the tax implications of exercising vested options before or after the IPO, timing of sales, and tax planning opportunities. This is also true for employees who have multiple types of equity.

Having an experienced financial advisor by your side can help you stay grounded in your plan, even when markets feel anything but steady. Your financial plan is designed for the long term. This may be a good time to revisit it and ensure it still reflects your needs, risktolerance, and goals.

Our Portfolio Manager, Chad NeSmith, CFA, CFP was recently quoted in an Associated Press article discussing how retirees are reacting to the market volatility spurred by the latest tariff announcements. The overall theme that were really getting at is you really have to be aware of your risktolerance and your financial plan, Chad shared.

Quoted in a Wall Street Journal article before the 2016 game, respected Wall Street analyst Robert Stoval said, “There is no intellectual backing for this sort of thing, except that it works.”. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Photo credit: Flickr.

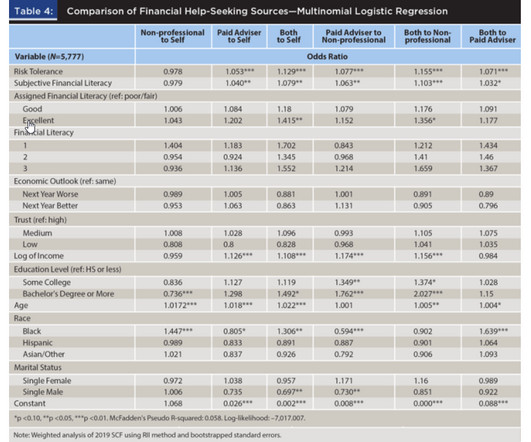

This article seeks to examine what research says about the interplay between risktolerance, financial literacy, and trust and their collective impact on the pursuit of financial advice by Black and Hispanic households. Do racial barriers prevent Black and Hispanic households from pursuing financial advice?

Keeping it safe, growing it wisely, and using it to support your future takes careful planning. Yet even the best financial plans can stumble. In this article, we’ll walk through some of the most common investment mistakes retirees make. A good estate plan ensures your assets go where you want them to.

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

Does it reflect your risktolerance and financial plan? Rather than reacting to short-term volatility, now is a great time to take a step back and review your investment portfolio. Is it still aligned with your long-term goals? Market movements like these serve as a reminder to check in and make adjustments if necessary.

It is for information and planning purposes only. Whether youre new to investing or have years of experience, taking a step back to evaluate your strategy can help ensure that your portfolio remains aligned with your objectives, especially in times of market uncertainty and volatility.

No one cares about your financial well-being more than you, so it's important to have a financial plan for yourself. Knowing how to make a financial plan will allow you to save money, afford the things you really want, and achieve long-term goals like saving for college and retirement. What is a financial plan?

High yields can be a sign of underlying issues with the company that puts principal at risk and endangers the dividend income if the company’s financials cannot support it. Before you can evaluate stocks or bonds to invest in, you’ll need to develop the metrics you plan to use in the analysis. versus 1.1%

Category: Clients Risk. When it comes to their investment portfolios many tend to have a low-risktolerance and with the unsettling economic situation with the ongoing pandemic, the word “risk” has become even more of a fearsome word for clients. How do you plan to approach such a client?

In this article, we will explore some strategies to help you choose the best investments for your IRA. 1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance.

One area that often gets overlooked in the midst of planning is reviewing your financial habits and goals, so I’ve put together a short list of 3 areas to review before January. If you are unsure if your portfolio aligns with your risktolerance, time horizon and goals, reach out to us at Mainstreet and we would be happy to help!

No one cares more about your financial well-being than you, so having a personal financial plan is important. Knowing how to make a financial plan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. Table of contents What is a financial plan?

In this article, you'll find out more about what this is and how to earn it. At the same time, you lower your exposure to the risks of each. Understand what risktolerance means for you Investing in securities like stocks and mutual funds is risky. Low-risktolerance means you’d rather play it safer when investing.

They can assess your financial situation, long-term goals, risktolerance, and investment preferences to create personalized strategies. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. But their support does not end there.

This article discusses the best way to invest 1000 dollars or a similarly small amount and covers some top tips on building wealth with patience and time. Experts recommend sticking to your investment plan, especially during market turbulence. The longer your money stays invested, the greater the exponential growth.

Unfortunately, most executives and insiders have less flexibility to reduce risk on a concentrated position of company stock. The situational nature of planning to diversify one large position cannot be over-emphasized, so it’s important to work with a financial advisor who has experience in this area.

There are many options, but your top priority should be choosing an investment that aligns well with your goals and risktolerance. Open a 529 College Savings Plan. Open a 529 College Savings Plan. You’ll need a few good ideas to develop a business plan that could work. Invest in ETFs. Hire a Robo-Advisor .

You may consult with a professional financial advisor to better understand your financial history and the ensuing impact your past choices may have on your future financial planning. They provide an opportunity to make necessary adjustments, whether it’s reallocating investments, revisiting saving rates, or redefining retirement plans.

In this article, well explore a step-by-step process to help you systematize client transitions, leveraging insights from experienced coaches Steve Sanduski and Amy Koenig. 02 Why a Well-Planned Transition Enhances Advisor Confidence? 02 Why a Well-Planned Transition Enhances Advisor Confidence?

There are many steps in building an investment portfolio, in this article, I’ll discuss how asset allocation and risktolerance are important considerations when investing. The appropriate mix or recipe in these various categories varies given your age, risktolerance, and timeline to retirement or spending.

If you’ve never engaged in financial planning and are unsure how to get started, this article is for you. A financial plan starts by evaluating your current financial situation and future expectations and can be created independently or with the help of a financial professional. Calculating current net worth and cash flow.

Traditional IRA: Best for Dedicated Retirement Planning. IRA plans are subject to Required Minimum Distributions (RMDs) beginning at age 72. Roth IRA: Best for Retirement Planning + Immediate Funds Access. Same procedure as with traditional IRAs, except you must specify the plan will be a Roth. How to invest.

The 401(k) Plan 2. The SEP-IRA (AKA Simplified Employee Pension) Expert tip: Understand your risktolerance How to save for retirement in your 20s when you’re just starting out How much should I contribute to my 401(k) in my 20s? Articles related to preparing for retirement Retirement planning in your 20s: Start saving now!

Retirement planning is not just about reaching a target savings number. Remember, effective retirement planning involves a balance of realistic expectations and prudent financial strategies, ensuring you can enjoy your retirement years with peace of mind and financial security.

This article will explore how often to rebalance your 401(k). Your investment strategy determines the target percentages for each asset, often based on your risktolerance, investment goals, and time horizon. This may lead to a higher or lower risk profile than initially intended. Need a financial advisor?

I also owned the name for a couple of more risktolerant clients. Very difficult to hold Jack Hough, writing for Barron's had a peculiarly thin article picking on managed futures. For a ten year run ending Jan 1, 2019 though it compounded at over 6% annually plus that dividend yield on top and a very low beta.

With medical inflation outpacing general inflation, ignoring healthcare in your retirement plan is a risk no one can afford. And if you are unsure where to begin, talking to a financial advisor can help you build a more personalized and realistic retirement plan. The second is to select a Medicare Advantage plan.

Articles related to investing for beginners These tips make how to start investing for beginners a breeze! In most cases, you plan for little ongoing involvement on your part once you’ve invested the money. Then you can choose the options that are best for you when you create your investment portfolio and financial plan.

Many choose to save through a 529 plan to make the process easier. But is a 529 plan worth it? Table of contents What is a 529 plan? What are the pros of a 529 plan? What are the cons of a 529 plan? Expert tip Is it possible to lose money in a 529 plan? We’ll also go over the pros and cons of 529 plans.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content