This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Health savings accounts (HSA) provide another vehicle to save for retirement. Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. HSA accounts can only be used in conjunction with a high-deductible health insurance plan. How the HSA works .

Which means that when an advisor recommends a certain investment strategy for a client, their standards of care should dictate that they first make sure that the strategy is within the client's tolerance for risk.

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

It is essential to choose investments that match your risk appetite to avoid unnecessary stress and surprises later. A financial advisor can help you understand your investment risktolerance. This article will focus on the risks of investing, how they impact you, and what you can do to determine your risk appetite.

But if you recently discovered that your risktolerance wasn't properly calibrated, now might be an okay time to get to a place that lets you sleep at night, especially with the S&P 500 just 6% off its all-time high.* There are two ways that risk can ruin you: by taking way too much of it or taking way too little.

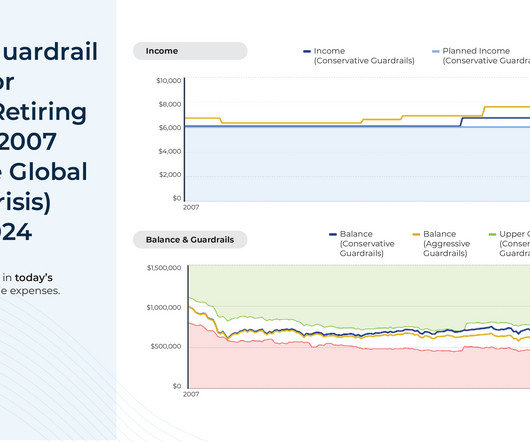

However, the results of these simulations generally don't account for potential adjustments that could be made along the way (e.g., This exercise can also give advisors and clients the opportunity to adjust the guardrail parameters depending on the client’s risktolerance (e.g.,

They consider your current financial situation, risktolerance, and future objectives to help develop a comprehensive plan. Accountability and Progress Tracking Regular consultations with a financial advisor can help provide accountability, helping you stay on track with your financial plan.

Take advantage of tax-advantaged retirement accounts such as 401(k)s, IRAs, and Roth IRAs to maximize your contributions and benefit from tax-deferred or tax-free growth. Aim to contribute as much as you can afford to these accounts each year to accelerate your retirement savings. Learn more about retirement plan options here.

Consider speaking with a financial advisor about risktolerance and strategies like tax loss harvesting. Zoe Financial is not an accounting firm- clients and prospective clients should consult with their tax professional regarding their specific tax situation. Stay tuned for next week.

As a result, advicers have more options than ever to add value for their clients by tailoring investment portfolios that are specific to their unique needs, goals, and risktolerance. size, industry, location) of early mutual funds. Specifically, 'high-quality' companies share several similar fundamental characteristics.

Available Accounts Individual taxable investment accounts only. Individual brokerage accounts, traditional and Roth IRAs, and custodial accounts. Individual and joint taxable investment accounts; traditional, Roth, rollover, and SEP IRAs. Individual and joint taxable accounts; traditional, Roth and rollover IRAs.

Portfolio income is the money you make from an investment account, and there are several ways to earn it. Portfolio income is income earned from investment accounts. Interest Interest-bearing accounts often show up on lists of ways to make passive income. For example, you have a savings account that earns interest.

Using Health Savings Accounts (HSAs) to manage healthcare costs in retirement A health savings account (HSA) is one of the most tax-efficient tools available for covering qualified medical expenses, both before and during retirement. Tax-free growth on interest and investment returns within the account.

Hypothetical simulation assumes $1M was invested on 12/31/2004, 50% in SPY and 50% in AGG, portfolio was never rebalanced, dividends not reinvested, and no other contributions/withdrawals in the account. Hypothetical simulation uses current yields and assumes 60% of the account is invested in SPY and 40% AGG. versus 1.1%

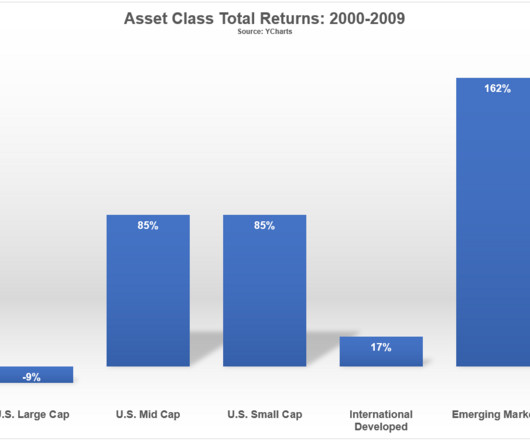

A reader asks: I am a 34-year-old with a high risktolerance. All of my investment accounts are 100% invested in stocks. The one thing I have a hard time finding a tried and true answer on when I do research is how to best allocate my stock investments among large-cap, mid-cap, international, emerging markets, etc.

They help you build and manage diversified portfolios aligned with your risktolerance and time horizon, potentially preventing costly mistakes that self-directed investors might make. Accountability and Support The accountability aspect alone can make talking to a financial planner worth the investment.

Today Bucket Time horizon: 02 years Purpose: Immediate needs, daily expenses, and short-term goals Investments: Cash accounts, savings accounts, short-term bonds This bucket is designed to help provide stability and gives you more access to funds for essential needs without worrying about market volatility. How Does Bucketing Work?

Here’s what to focus on: List your assets: Include properties, investments, savings, retirement accounts, insurance, and personal valuables. Name your beneficiaries: Especially for accounts like 401(k)s, IRAs, and insurance policies. Determine your goals, timeline, and risktolerance before you invest. The result?

Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. View all accounts as part of a total portfolio. This means IRAs, your 401(k) , taxable accounts, mutual funds , individual stocks and bonds, etc. Take stock of where you are.

Each has unique benefits and drawbacks, and understanding these can help you decide which fits best with your financial situation, risktolerance, and goals. 529 Plans 529 Plans are specialized savings accounts designed to help families save for future education costs.

Review risktolerance and current asset allocation strategy It’s important to ensure your clients’ portfolios align with their risktolerance because taking too much risk can negatively impact their ability to navigate market fluctuations. You can help them start the year right by conducting a retirement checkup.

If you are willing to take a few calculated risks and stay the course, small-cap stocks can be a powerful tool. Do not neglect the obvious choices – 401(k) and Individual Retirement Account (IRA) Sure, when you Google investment options, a 401(k) or an IRA might seem like the most basic answers out there.

As you defer money into your retirement account, each dollar that you defer could be worth as much as $1.65. Since you are not taxed on each dollar that has been deferred into the retirement account, your “take home” pay only reduces by the amount that is left over after taxation. Each dollar you defer is worth more than a dollar.

Through your 401(k), you’re able to contribute funds and invest them according to your risktolerance and retirement timeline. 1: Your 401(k) is Directly Connected to Your Employer The contributions you make to your 401(k) are 100% yours, but the account itself is technically sponsored by your employer.

Let’s explore how 529 plans compare to Coverdell Education Savings Accounts (ESAs), pre-paid tuition plans, custodial accounts, and taxable investment accounts. Custodial Accounts UGMA and UTMA accounts are custodial accounts that provide more flexibility in investment choices and usage.

Best 1,000-dollar investment instruments High-yield savings accounts or certificates of deposit (CDs) : High-yield savings accounts and CDs are excellent entry points for those who prioritize safety and stability. These options typically offer higher interest rates than traditional savings accounts and come with minimal risk.

Waterfall Wealth vs. Traditional Investment Strategies Traditional investment strategies focus on diversification, risktolerance, and asset allocation across stocks, bonds, and real estate. Tier 2: Allocates funds to retirement accounts and family support. While effective, they often lack a prioritization system.

There are many options, but your top priority should be choosing an investment that aligns well with your goals and risktolerance. High-Yield Savings Accounts . Open a Health Savings Account (HSA) . High-Yield Savings Accounts. Open a Health Savings Account (HSA). Open an Account. Open a Roth IRA.

Although your savings account might have the same balance ten years from now, that money will not have the same purchasing power that it has today. Begin investing money into employer-sponsored accounts. You may work for a company, where you likely have access to some employer-sponsored investment accounts.

Investing in an Individual Retirement Account (IRA) is an excellent way to save for retirement. 1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance. However, selecting the right investments for your IRA can be challenging.

They can assess your financial situation, long-term goals, risktolerance, and investment preferences to create personalized strategies. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. Tax planning is not solely about federal taxes.

It requires a different perspective on your wealth and income that accounts for your needs in different stages of your life, from the beginning of your working years through your retirement. This usually consists of cash held in checking accounts, savings accounts, or short-term Certificate Deposit accounts.

For example, you may hold some of your investments with a robo-advisor while maintaining an account with an investment brokerage firm for self-directed investing. Available accounts: Joint and individual accounts; traditional, Roth , rollover, SEP, and SIMPLE IRAs; Solo 401(k)’s ; trusts and custodial accounts.

The SEP-IRA (AKA Simplified Employee Pension) Expert tip: Understand your risktolerance How to save for retirement in your 20s when you’re just starting out How much should I contribute to my 401(k) in my 20s? First, of course, you need to pick the right account that aligns with your financial situation and goals.

During the financial crisis there were many stories about how our 401(k) accounts had become “201(k)s.” What it does mean is that you need to use your good common sense and keep your portfolio allocated in a fashion that is consistent with your retirement goals, your time horizon and your risktolerance. Review and rebalance .

Beef up your emergency fund – A good rule of thumb is to have between 3-6 months’ worth of expenses set aside in a high-yield savings account. The catch-up contribution (available for anyone over age 50) remains the same at $7500 for elective deferral account and $1k/year for Traditional and Roth IRAs.

Although your savings account might have the same balance ten years from now, that money will not have the same purchasing power that it has today. It depends on how much you make, when you want to retire, and how much you want in your accounts by then. However, your savings are diminished each day by the powers of inflation.

Even though the federal government has rescued SVB and guaranteed all deposits over the FDIC insurance limit of $250,000 per account, that doesn’t mean they will be doing it again for other banks. In the United States, any individual account with a balance of up to $250,000 at a bank is insured. and are not protected by SIPC.

Financial advisors should take these factors into account to ensure their clients receive the right experience. They want a financial strategy that takes every aspect of their life into account, such as their income situation, investment goals, debt, risk appetite, and more. They are looking for something much more cohesive.

Yet, you can also invest in stocks, bonds, index funds, and any other type of securities with the help of a brokerage account. Although brokerage accounts don’t offer any upfront tax advantages, you get the chance to invest in any number of stocks, ETFs, and more. You’ll just need to account for capital gains taxes when you do.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content