This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

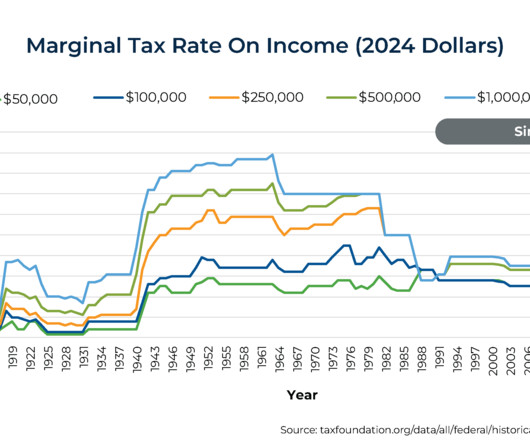

Over the last 60 years, the top Federal marginal tax bracket has steadily decreased from over 90% in the 1950s and 60s to 'just' 37% today. While it's true that the top marginal tax rate has decreased dramatically since the mid-20th century, the difference in the actual tax paid by most Americans has been far more modest.

As a freelancer, you juggle not only your craft but also your finances, taxes, and retirement planning. As a freelancer, youre your own boss, accountant, and financial planner all rolled into one. Create a realistic budget 2. Plan for taxes ahead of time 4. That’s where financial planning for freelancers comes in.

Create or Refresh Your Budget Think of your budget as the foundation of your financial house. Three to six months worth of expenses tucked away in a high-yield savings account. Optimize Tax Strategies Its not what you makeits what you keep. Heres your top 10 financial planning checklist for the new year. Submit a form.

Freezing your credit is an effective way to protect against identity theft and unauthorized access to your financial accounts. Verify that the information is accurate and that all your credit cards, store accounts, and loans are properly listed. For 2024, the maximum taxable earnings subject to Social Security tax is $168,600.

Interested in using Harness at your tax firm, or know a tax firm you’d like to refer to Harness? What does it really take to build a future-ready tax firm? Generally, most state individual and corporate income tax changes take effect on January 1, the beginning of the calendar year, for consistency through the tax year.

Love it or hate it, if you want to be financially successful, you need to budget your money and understand budget categories. Getting your finances in order and building wealth takes planning, and your budget can help you do just that. Determine which budgeting methods will work for you 2. Table of contents 1.

Like many, you might shudder at the word budget. But the 50-30-20 budget and the 50-30-20 budget template prove it doesn't have to be difficult. A budget plans out exactly how you'll use your money and this can be tailored to suit your specific lifestyle and situation. What is a 50-30-20 budget?

If you don’t feel like you truly have a strong handle on your finances, one possible cause for that is using a budgeting method that doesn’t work. While not everyone needs a to-the-penny balanced budget, some type of budgeting strategy or template is really important if you want to know where your money is going month after month.

Budgeting as a couple is critical in managing your household finances. Your budget not only allows you to plan and track where the money will be spent, but it enables you to direct the course of your finances together. Table of contents 5 Steps to get started budgeting as a couple Expert tip What is the best way to budget as a couple?

When you try to manage the accounting and bookkeeping for your business yourself, you may run into trouble. Here are some things to consider before you try DIY accounting for your business. You should be able to spend time on ways to grow your business, not accounting and bookkeeping. .

Love it or hate it, if you want to be financially successful, you need to budget your money and success with budgeting means understanding budget categories. So, let’s talk about the various categories that you might need, including a budget categories list! How many categories should I have for a budget?

Like many, you might shudder at the word budget, or perhaps it sounds too boring or challenging to figure out. But the 50-30-20 rule and the 50 30 20 budget template prove it doesn’t have to be difficult. If you’re looking to simplify your budgeting process or are new to budgeting, then this might be the perfect match!

Setting a budget might sound about as fun as doing your taxes, but trust me, it doesn’t have to be a drag! Whether you’re just starting out or need a little refresher, let’s break down the key factors you should consider when setting a budget! Adjust as your budget as needed 7. Table of contents 1.

Using Health Savings Accounts (HSAs) to manage healthcare costs in retirement A health savings account (HSA) is one of the most tax-efficient tools available for covering qualified medical expenses, both before and during retirement. Tax-free growth on interest and investment returns within the account.

You can reduce your stock exposure and increase investments in fixed income options, such as cash or bonds, within tax-advantaged accounts (like a 401(k), IRA, or Roth IRA). This adjustment lowers risk without triggering tax consequences, giving you more stability in uncertain markets.

The 60/30/10 budget turns the traditional rules of budgeting upside down. Instead of focusing on discretionary spending, this budgeting rule emphasizes sprinting toward our financial goals. And although the 60/30/10 rule budget won’t work for everyone, many could use it to take their finances to the next level.

Budgeting is one of the most important financial habits to develop. There are so many budgeting methods out there to choose from, but it’s not just creating a budget that will set you up for financial success. How do I plan for variable vs fixed expenses in my budget? What are average expenses for a household?

There are many different ways to come up with your perfect budgeting strategy. Alongside your monthly budget, you should also have a bare bones budget waiting in the wings. Table of contents What is a bare bones budget? Who needs a bare bones budget? It’s a budget that only covers the necessities.

A quick Google search of budgeting methods will show you that there’s no shortage of options out there. There is, however, one particular budgeting method that could work well if you are just getting started with budgeting and more so if you don’t like the idea of a monthly budget. What is a paycheck budget?

There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, tax planning, and more. These expenses may form a large part of your budget today but may not likely figure in the future. Additionally, you would also have to account for health insurance premiums.

This information is critical if you want to create a budget and manage your money correctly. I’ll also share some budgeting and side hustle tips so you can get the most out of the money you earn. Paid Time Off for Hourly Employees Earning $25 per Hour How Much Is $25 An Hour After Taxes? How Does $25 an Hour Compare?

In personal finance, where income, expenses, dreams, and aspirations converge, the budget emerges as a crucial tool. And when you have a family, creating a family budget becomes even more important. Table of contents What is a family budget? How does a typical family budget look? What is the average family monthly budget?

It can also help reduce taxes and make life easier for your family during difficult times. Here’s what to focus on: List your assets: Include properties, investments, savings, retirement accounts, insurance, and personal valuables. Name your beneficiaries: Especially for accounts like 401(k)s, IRAs, and insurance policies.

” A : Money is NOT a store of value to be useful, a dollar must maintain its value long enough for me to pay my rent or mortgage, buy food and energy, fund my entertainment and travel, pay my taxes, and get invested. Units of account seem inevitable once you go beyond barter and basic trade. It does that splendidly.

Here is what we are doing to efficiently manage investments after accounting for the budget changes. – Debt funds investment made before 31 Mar 2023 will qualify for LTCG after two years and be taxed at 12.5% Although the effective tax rate has gone up marginally, the holding period for LTCG has come down.

Key Takeaways: Even without new legislation, the prospect of higher taxes in the future is still looming. The impact of higher taxes on retirees could be substantial, so staying up to date on the current tax landscape is vital. But even without new legislation, the prospect of higher taxes in the future is still looming.

Most of us get paid by a direct deposit into our bank account. If they get a 7% increase in wages, they see a modest increase in their direct deposit of after FICA, federal and state withholding taxes, 401K, etc. and energy as a percentage of your household budget is less than it ever was.

Aim to set aside three to six months’ worth of living expenses in a liquid savings account. Start saving early by contributing to tax-advantaged accounts like 529 Plans or Coverdell Education Savings Accounts (ESAs). Plus, they can be used to cover various educational expenses, including tuition, room, and board.

Review Your Budget — And Your Spending Leaks Even high earners lose track of money. Ensure you’re earning a competitive rate on savings Rebalance between checking, savings, and investment accounts Consider a high-yield account for emergency reserves 4. Are your investment accounts aligned with your risk profile and goals?

Financial advisors should take these factors into account to ensure their clients receive the right experience. They want a financial strategy that takes every aspect of their life into account, such as their income situation, investment goals, debt, risk appetite, and more. They are looking for something much more cohesive.

These events may affect your investment approach, tax planning strategies, insurance needs, and estate planning documents. Monthly or quarterly reviews of bank statements, budgets, and investment accounts can help monitor your day-to-day financial health.

The truth is, only good things can come from looking at all your accounts, your spending, your savings, etc., Find some tax savings While your taxes are fresh on your mind, you can use this time to organize your paperwork, checking your withholdings and evaluating your tax-savings strategies.

If you’re having trouble balancing your budget (your income is less than your expenses) you’ll need to look at the “nice” expenses and determine what you can do without. As you know, there are many types of investment accounts, investment products, and the like, that you could use to increase your bottom line.

Tax planning. Utilizing tax-efficient investment strategies, such as municipal bonds and tax-managed ETFs, may help minimize tax liabilities. Charitable giving and philanthropic activities can also provide tax benefits while supporting causes you care about. Budget for emergencies. Tax planning is crucial.

Taxes One of the biggest financial considerations for Americans retiring abroad is understanding how taxes will work. is one of the few countries that taxes its citizens on worldwide income, regardless of where they reside. tax return every year. To avoid double taxation — paying taxes both in the U.S.

And a tax-efficient withdrawal strategy that won’t sabotage your nest egg early. Unless you’ve planned a dedicated healthcare bridge (or have access to employer-sponsored retiree coverage), this cost can derail even the most detailed budget. This approach involves: Building up taxable brokerage accounts or cash savings.

Even if you can’t contribute a significant amount each month, any savings will help strengthen your financial future, put you on track for a comfortable retirement, and take advantage of specific tax incentives. Create a Budget Creating a budget allows you to track your expenses and ensure you’re saving enough for retirement.

Draft a Retirement Budget. Even if you haven’t adhered to a strict budget during your working years, having a budget during the early months of retirement may be crucial—spending more than you’ve planned or failing to anticipate certain large expenses may impact your future retirement income.

As a freelancer, you juggle not only your craft but also your finances, taxes, and retirement planning. As a freelancer, youre your own boss, accountant, and financial planner all rolled into one. Create a realistic budget 2. Plan for taxes ahead of time 4. That’s where financial planning for freelancers comes in.

This can come from dividends, interest, rental income, and distributions from brokerage or retirement accounts. For example, if funds are invested in a brokerage or retirement account, they may generate dividends or interest, which contribute to total earnings. Spend Spending refers to the money leaving an account for expenses.

There are many different ways to come up with your perfect budgeting strategy. Alongside your monthly budget, you should also have a bare bones budget waiting in the wings. What is a bare bones budget? It's a budget that only covers the necessities. That's why this is not a sustainable long-term budget.

Accounting and tax software have made it possible for small businesses to get along without having an in-house accountant. However, as businesses grow, accounting issues get more complex, and tax filings become too cumbersome for owners to handle. Overview: What Does a Small Business Accountant Do?

The importance of understanding financial literacy basics Financial literacy covers several topics , including budgeting, banking, investing, handling debt, and planning for the future. And budgeting isn’t as tricky as it sounds. Open a bank account Bank accounts are a safe way to store your money.

Let’s talk about saving money for your child via custodial accounts and education plans. Different types of custodial accounts for minors can help you save for your child’s future. Table of contents What is a custodial account? Are custodial accounts a good idea? Can parents take money from custodial accounts?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content