This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Solo 401(k) plans are a popular retirement savings vehicle for self-employed business owners. By maximizing both the employee employer contributions, solo 401(k) plan owners can often save significantly more than is possible with other types of retirement plans available to self-employed workers, like SEPs and standard IRAs.

Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B In 2023, he launched his own firm, Park Hill Financial Planning and Investment Management. “I Resonant Capital Merges with Tax, Accounting Firm QBCo Brennan’s experience is indicative of many young advisors working in the RIA space. Concept of digital social marketing.

That means if your retirement plan underestimates medical costs, you risk serious shortfalls. at the start of 2022, given an average inflation rate of 7.5% over that period. If you planned to live on ₹1 lakh per month today, you might need ₹1.5 – ₹1.7 at the start of 2022, given an average inflation rate of 7.5%

Related: Planning for Older Clients and Those with Disabilities Many GRATs include a so-called “swap” power in which the grantor is permitted to substitute assets of equivalent value with the GRAT. Smith, 2022 U.S. April 26, 2022)) has held that exercising the swap power could be considered a purchase under the insider trading rules.

As dynamic as the secondary market may be, secondaries come with complex tax implications that can significantly impact returns if not properly managed. What are the tax implications of secondary transactions? What are the tax challenges in secondary transactions? What tax strategies optimize secondary investments?

Keeping it safe, growing it wisely, and using it to support your future takes careful planning. Yet even the best financial plans can stumble. Take the year 2022, for example. Mistake #2: Not having an estate plan in place Estate planning is essential for protecting what you’ve worked hard to build.

The rise of remote work and digital nomadism has made FEIE a common tax minimization strategy for Americans living abroad. What is the Foreign Tax Credit (FTC)? Financial and lifestyle considerations of living abroad The importance of professional tax advice for expats FAQs about the FEIE What is the Foreign Earned Income Exclusion?

Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B The Los Angeles-based firm has ramped up investments in sports, including taking stakes in the Miami Dolphins National Football League team, Inter Miami CF and Chelsea football club, and closed its first fund dedicated to the strategy in 2022 with $3.7

Transaction fees, management fees, and capital gains taxes can eat into your returns. For example, research from S&P Global found that over the 20-year period ending in 2022, only about 4.1% The markets are fickle, and prone to quick swings based on even seemingly minor events. of professionally managed portfolios in the U.S.

There’s also recency bias at play: The market downturns of 2022 and the COVID-19 shock in 2020 linger in memory, making us forget the equally compelling history of market recoveries and long-term growth. 15:10] Optimize cash flow through strategic sales while considering tax efficiency. [19:50] Cash is Comforting, but at What Cost?

Source: [link] As you can see, 66% of voters in 2022 fall in that category and would likely have a major influence on electing officials who support measures to fully fund Social Security. Many of the solutions offered back then are also applicable to todays projected funding shortage. especially for voters nearing or in retirement.

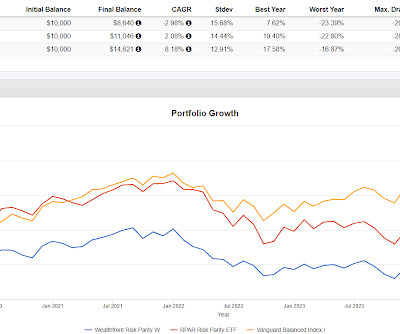

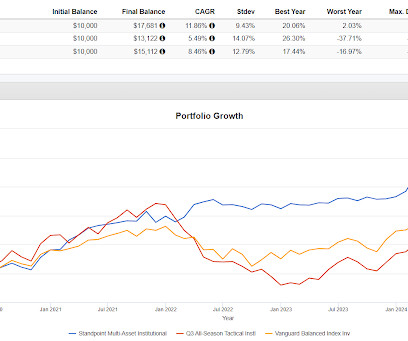

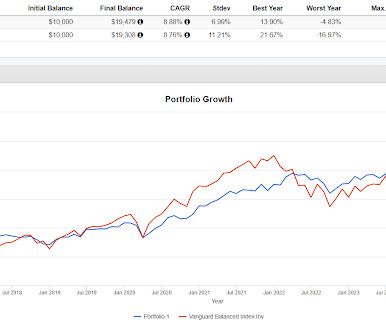

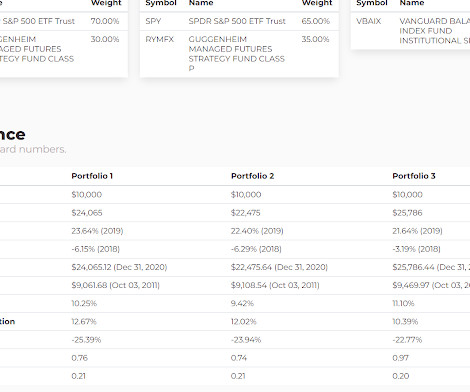

You can see on the backtest, RPAR fairing worse than VBAIX by almost 600 basis points in 2022 and then didn't really come back the way VBAIX did. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Risk parity is a good example of a great story.

Tariffs impact: Proposed increases could raise the effective tax rate on U.S. I ntra-year drop: Markets are down ~1819% this year high, but still within historical norms: 2022: 25% 2020 (COVID): 34% 2008 (financial crisis): 49% Volatility spike: VIX rose above 45 one of the highest on record. imports from 2.3%

There are several types of IRAs, such as Traditional, Roth, Simplified Employee Pension (SEP), and Savings Incentive Match Plan for Employees (SIMPLE). However, when it comes to taxes, the two main ones you need to know about are Traditional and Roth. The rules around withdrawals and tax treatment are very different for each.

The Growing Role of Philanthropy in Wealth Planning People today are more interested than ever in finding ways to align their long-term financial goals and their personal values. There are overall limits on charitable donation tax deductions, however. Values are among the most important things parents can pass on to their children.

In 2022, it was up 104 basis points (total return). but it was low in 2022 when it mattered. In 2022, when managed futures was having its heyday, there were all of a sudden a lot of calls about putting 20% or more in managed futures. The results were fascinating. We pounded the table here why that was probably a bad idea.

The Invenomic Fund (BIVIX) that we've looked at a few times is seriously skewed by two phenomenal years in 2021 and 2022 when it was up 61% and then 50%. If I had gotten a real answer I would have asked the same for 2022. In 2022, UPAR was down 30%. I asked three different AIs why it did so well in 2021.

Yes the dividend funds did better than SPY in 2022 but not 2020 and in the financial crisis, I believe DVY was the only one that was around and being heaviest in financials, it did very badly. Long terms gains get better tax treatment everything else being equal. Long terms gains get better tax treatment everything else being equal.

Data from the Federal Reserves 2022 Survey of Consumer Finances (SCF) (released in late 2023) offers the most recent comprehensive snapshot of American household wealth. Find Your Wealth Advisor at Harness How Net Worth Is Changing in America From 2016 to 2022, the median U.S. Whats on the Average American Balance Sheet?

What were the original career plans? So I arrived at Wellesley with the plan to do pre-med. Here is the plan, here’s how you should go about in this deal or in, in this new asset class. 00:36:59 [Speaker Changed] So, so I mentioned the 10 years, about four and a half percent today, go back before 2022.

If the idea is a smoother ride with 75/50 then we should be trying avoiding being overly vulnerable one one alternative hitting the skids in a year like 2022. has price inflation compounding at 4.31% but the TIP ETF has negatively compounded by a few basis points because it got crushed in 2022. Note that 2021 was a partial year.

All three were better than VBAIX in 2022 by 150-550 basis points. Somehow, it did worse than the S&P 500 by several hundred basis points in 2022. Based on the chart, I'm guessing that SPD was positioned in such a way as to miss the bounce that started in late 2022. The results are not skewed by one year.

QAISX outperformed VBAIX by a good bit in every year except 2022. Generically, if a fund creates the effect of an entire portfolio with just a 50% allocation, then of course it would go down more in nominal terms in a year like 2022 (expectations). The fund is the same age as BLNDX.

By now you've heard that Warren Buffett plans to step down at the end of the year. The purple line went through a nasty drop in 2022. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. The best performer has had several nasty declines.

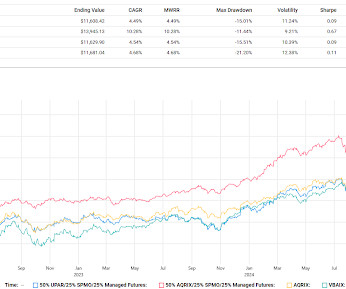

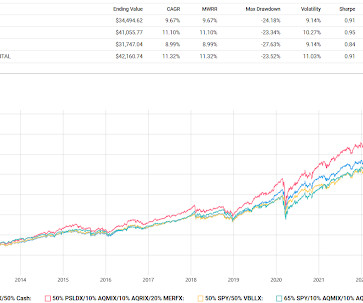

The max drawdowns of the backtested portfolios bottomed out in late 2022 as follows To the extent quadrant style might intersect with all-weather, you can decide for yourself whether any of them were all weather enough. There's no wrong conclusion to draw, do you think they are all-weather enough?

The example assumes no sort of serious medical or family calamity that altered your financial plan, life happens that way sometimes. There were a couple of instances of outperformance in the period studied including 2022 when it was up 46 basis points and it is slightly ahead this year too. Here's the thing, it lags almost every year.

The levered portfolio did slightly worse in 2022 but not catastrophically worse despite UPRO falling 56% and TYD falling 43%. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. BTAL and the Merger Fund are client and personal holdings.

The outperformance isn't solely because of 2022, VOO/BALT outperformed in partial year, 2021, 2023 and 2024. That big drop in SHRIX in late 2022 was from the threat of Hurricane Ian but it turned out there was no triggering event from that one. Using BALT instead of AGG has given a higher compounded return with less volatility.

Consumer discretionary is another one that pretty reliably outperforms for ten year periods, not the last couple though after getting whacked pretty hard in 2022 though. As you might expect, staples went down much less in the Financial Crisis as well as in 2022. Tech is a very good bet to regularly outperform the S&P 500.

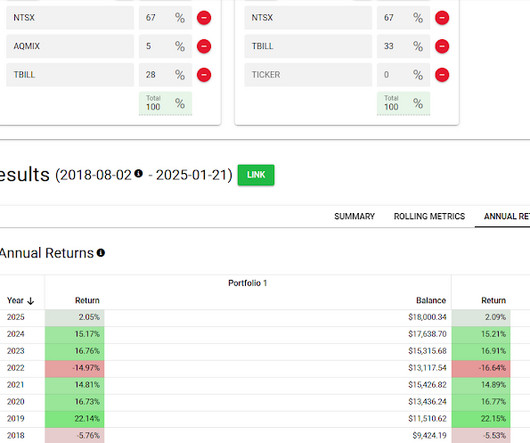

Portfolio 4 has middling stats compared to the others but in 2022 it was only down 8.23% versus 20% for Portfolio 1, 17% for Portfolio 2 and Portfolio 3 was down 22%. Also PSLDX is capable of some huge drawdowns, dropping 43% in 2022 and 33% in 2008. It also fell 37% in the 2020 Pandemic Crash but it took that back in just four months.

Generically, dividends are not tax efficient. They are taxed at ordinary income. SCHD has historically paid "qualified" dividends which are taxed more favorably as capital gains but this is something to continuously track. Derivative income funds that track indexes might be taxed 60/40, you have to check.

We talked at length in 2022 and into 2023 when managed futures was booming and people were coming out of the woodwork to suggest huge weightings to managed futures which I said was a bad idea back then and is a bad idea right now in terms of constructing a portfolio. In that light, 20% or 25% makes no sense to me.

Isolating the returns of the diversifiers in 2022, but taking out OSOL and AMPD because they weren't around the whole year, you can see that only Bitcoin had a rough time, several were flat (which is good for a year like 2022) and several were up a lot.

We spend a lot of time here on how to diversify to try to smooth out the ride and how to hold up better when markets have a year like 2022 or 2008. Early on, the MCW and Quality versions outperformed VBAIX slightly, probably just due to having a little more equity exposure and all three of them significantly outperformed in 2022.

Investors of course love dividends but share buybacks and debt reduction are more tax efficient than dividends which are taxed at ordinary income rates. In addition to what is shown above, in 2022 SYLD only dropped 6.12%. LBAY was up 22% in 2022 and I'm not sure if that is repeatable. versus 4.5% Now as a diversifier.

The 2022 tech selloff and subsequent recovery periods would have hit XLK particularly hard due to this concentration. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. There was a little more but the above gives you the general idea.

Portfolio 1 was way ahead in 2022, way behind in 2023 and 2024 but it was up nicely those years and this year it is way ahead. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. In 2021 it lagged the index by 12%.

We have a couple of different articles about private assets being available or otherwise worked into 401k plans. First is 401k provider Empower starting to rollout private equity, credit and real estate into plans they offer, ranging from 5-20% allocations. trillion market for 401(k)-type retirement plans as crucial to this growth. "

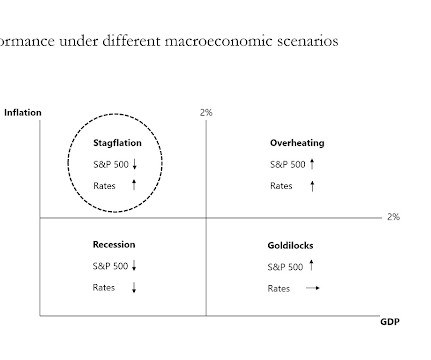

2022 gives a good test for stagflation as Slok sees it because rates went up and stocks went down. In 2022, that blend was down 89 basis points so some drag (PRPFX did worse than BLNDX that year) but not problematic. The Permanent Portfolio allocates 25% each to stocks, gold, long bonds and cash.

Obviously all four were much better in 2022 but not this year at the April lows. The max drawdown numbers all hit in August, 2022. MBB's max drawdown by itself came a little later in 2022 down 16.91%, the AGG max drawdown that year was 17.38% and iShares 10-20 Year Treasury ETF (TLH) bottomed out down 32%.

Both exchange portfolios held up much better in 2022. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. There are some interesting numbers in the Claude basket related to volatility and Sharpe Ratio. I'm not saying AI's role is nothing.

The three alts looked nothing like VBAIX in 2022 which was a good thing and they look nothing like VBAIX in the other years which is the challenge of having huge allocations to negatively correlated alts and why I talk all the time about small exposures to diversifiers. In 2022, the red bar was down 54 basis points.

It did decline about 5% in the 2020 Pandemic Crash and in 2022 it was up 1.36%. I put together the following that just looks at 2022, when investors needed the uncorrelated streams; There are 15 different return streams there in addition to VOO and VBAIX. The USAF backtest and RAAX don't really look too similar to me.

There will obviously be future bear markets and the extent to which they cause real damage to a financial plan depends on whether any steps are taken to mitigate the full brunt of a decline that. The 5% weighting to managed futures helped by 167 basis points in 2022. It's very simple.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content