This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

2017 Year-End Planning Letter. Mon, 12/04/2017 - 13:10. He notes that in the 1980s, there was a dire need to jumpstart a moribund economy, and the administration was able to mobilize bipartisan cooperation to enact reform. We are closing 2017 with nearly the same stance as last year. Since last year’s U.S.

distillate fuel oil inventories have been below the five-year low (2017–2021) since the start of 2022, primarily driven by less global refining capacity. Uncertainty across commodity markets can also be viewed through valuations, earnings, and profitability metrics. Energy Information Administration (EIA), U.S.

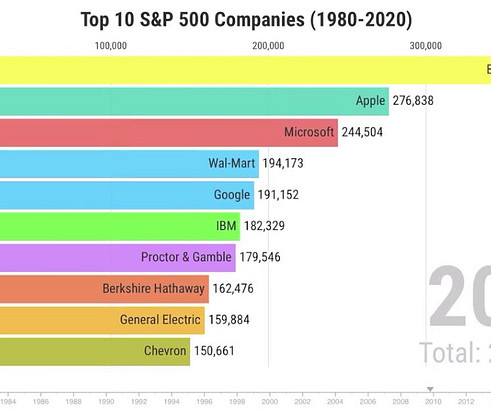

IBM’s return was fueled by growing earnings, growing dividends, and buying back stock at cheap valuations. Even Buffett, whose BKB made the list, was about to buy (he bought into IBM in 2011, although the trade didn’t turn out well; he was out in 2017, having earned about 5 percent per year, including dividends).

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Asset allocation—at least for us—is an exercise in nuance. Further, we see room for the European economy to grow. But it is a meaningful change worthy of discussion after a long period of time. is not particularly notable.

Thu, 06/01/2017 - 02:47. Throughout this period, we often saw windows in which we believed that European valuations were more attractive, but we were cautious due to Europe’s high debt levels and struggles to generate economic growth. Further, we see room for the European economy to grow. is not particularly notable.

For a broad view of our expectations for the economy, stocks, and bonds in 2024, download our 2024 Market Outlook. That bear eventually ended in October 2022, and since then stocks have defied many experts, who continually (and incorrectly) touted a weakening economy, tapped-out consumer, and many other reasons to doubt the new bull market.

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/29/2017 2.9% 12/29/2017 49.5% And with intangible assets rising in the economy, standard earnings calculations are becoming less and less accurate. By Jack Forehand, CFA, CFP® ( @practicalquant ) —.

After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy. The tariffs announced so far affect a very small slice of the global economy, but we could see an escalation into a broader set of trade barriers between China and the U.S.,

After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy. The tariffs announced so far affect a very small slice of the global economy, but we could see an escalation into a broader set of trade barriers between China and the U.S.,

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks. In non-U.S.

Balancing Act | Pulling the FANGs Apart achen Thu, 12/14/2017 - 11:34 The “FANG” companies—Facebook, Amazon, Netflix and Google—have been a dominant investment story in recent years. All of these companies have generated attractive returns in recent years, and in 2017 in particular. Through Nov.

Thu, 12/14/2017 - 11:34. All of these companies have generated attractive returns in recent years, and in 2017 in particular. Their fear is bolstered by historical precedent: In the 1960s and 1970s, the “Nifty Fifty” ran up to extremely high valuations, and many performed quite poorly during the 1970s bear market. Through Nov.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Using the 10-year U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Using the 10-year U.S.

Throughout 2017, our meetings and conversations with clients very frequently focused on the topic of risk. Economic growth and corporate earnings across the world improved notably throughout 2017, led by an acceleration in Europe, a rebound in emerging markets and improved sentiment in some U.S. Fri, 03/30/2018 - 11:57. company.

Balancing Act | A New Publication Series achen Tue, 11/28/2017 - 13:39 We believe that investing in equities should be a balancing act, not an exercise in placing bets on one side of the market. We believe that investing in equities should be a balancing act, not an exercise in placing bets on one side of the scale or the other.

Tue, 11/28/2017 - 13:39. At any given time, we need to weigh the risk and opportunity we see in the economy, in the stock market and in individual companies—all in an effort to balance the possible positive and negative outcomes of every investment we make. Balancing Act | A New Publication Series.

Given the country’s weak economy, due in large part to stringent zero-COVID-19 measures that have led to strict and prolonged lockdowns, coupled with a debt-laden property market, authorities in Beijing and throughout the Chinese provinces will need to focus on reviving the country’s economic underpinning. At the same time, U.S.

As the economy is likely downshifting, investors should take heed that the Federal Reserve’s (Fed) current stance is eerily similar to early 2007. During that time, the Fed held a tightening bias since they believed the housing market was stabilizing, the economy would continue to expand, and inflation risks remained.

The Company has over 6 years of experience in the execution of infrastructure projects since 2017. Under the Bharatmala Pariyojana plan, the Government approved Phase-I of the project in October 2017 with an aggregate length of 34,800 Km with an estimated outlay of Rs. The IRB InvIT was listed on the exchanges in June of 2017.

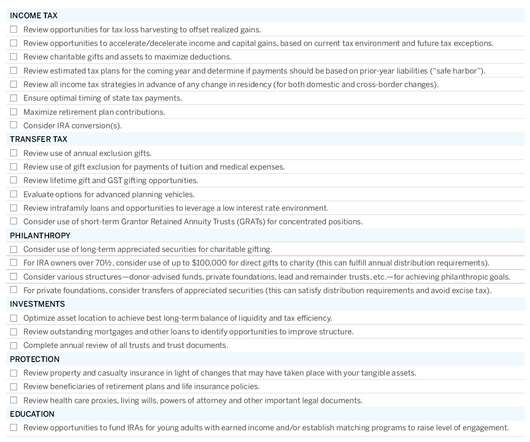

This year, two factors will be important considerations in our year-end planning work: 1) current market dynamics (specifically, ongoing market volatility, low interest rates and a flat yield curve), and 2) the 2017 tax overhaul and our ongoing integration of new tax rules into clients’ long-term plans. Non-Taxable Gifts.

Balancing Act | A Stroll Down Hindsight Lane achen Tue, 11/28/2017 - 14:27 Market downturns and recessions may seem easy to predict. Well, we believe that broader economic fundamentals are important for long-term stock valuations. It's the Economy In short, precise market timing is impossible, in our view.

Tue, 11/28/2017 - 14:27. Well, we believe that broader economic fundamentals are important for long-term stock valuations. It's the Economy. One factor that seems to be quite relevant is the health of the economy when a downturn occurs. Balancing Act | A Stroll Down Hindsight Lane. The Value of Active Management. ?As

A Moment of Zen: The Wisdom of Staying Invested achen Wed, 07/19/2017 - 15:28 When discussing the merits of cash as an investment, Warren Buffett doesn’t pull his punches, saying that those who hold cash or its equivalents “have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.”

Wed, 07/19/2017 - 15:28. Valuations of the U.S. and global economies have managed to eke out decent performance in recent years but have yet to re-establish their pre-crisis growth levels. Today, we hear the word “unprecedented” far too often, referencing everything from stock valuations, to the U.S. company.

Manager Q&A: Mick Dillon and Bertie Thomson, Global Leaders Strategy achen Fri, 08/25/2017 - 11:34 Indeed a host of macro-economic and political events have impacted global markets since Mick Dillon and Bertie Thomson launched the Brown Advisory Global Leaders strategy. In our view, this decline presented a great valuation opportunity.

Fri, 08/25/2017 - 11:34. as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition." Beyond that indicator, the managers look for companies with three other qualities: solid fundamentals, strong leadership and reasonable valuations. src="[link] />?. 6th Edition, 2015.

In Crores) Company 2017 2018 2019 2020 2021 2022 Revenue ? The company has managed a low PE compared to its peers in the industry promises a fair valuation despite the meteoric rise. India, being an emerging economy urbanization and industrialization hold key to the development. Economy of scales. Past performances. (In

There are some warning signs, to be sure, such as an inverted yield curve, tight labor markets, and a slowing housing market, but there are also other factors—such as modest household leverage, low corporate default rates and accommodating monetary policy—that suggest the economy may still have some room to run. Treasuries.

We know that equity valuations in the U.S. CURRENT VALUATION PREMIUMS, S&P 500 INDEX Metric Most Recent Long-Term Average Premium vs. Average Timeframe Trailing P/E 19.4 Any number of factors could cause valuations to quickly readjust or correlations to spike. 17% 3/31/1954- 9/30/2019 Price/Book Value 3.4 Further, U.S.

We know that equity valuations in the U.S. CURRENT VALUATION PREMIUMS, S&P 500 INDEX. In the years after the 2008-09 financial crisis, securities tended to trade in lockstep with each other as the market focused most of its attention on the big-picture health of the economy. Most Recent. Long-Term Average. Premium vs. Average.

For several years after the crisis, we consciously underweighted Europe; austerity as well as the economies of Greece and several other “peripheral” EU nations held back Europe’s recovery relative to the U.S. Equity valuations in Europe at the time were more attractive than those in the U.S.

For several years after the crisis, we consciously underweighted Europe; austerity as well as the economies of Greece and several other “peripheral” EU nations held back Europe’s recovery relative to the U.S. Equity valuations in Europe at the time were more attractive than those in the U.S.

Download it here > Dear Fellow Investors, If we had to sum up 2022 in one word it would be valuation. War, inflation, recession, deglobalisation, decoupling, strikes, crypto-crash and energy (crisis) all featured but for us the overriding focus for 2022 was valuation. There are many disturbing parallels in today’s global economy.

Further reading on this subject: Q1 2017 Investment Letter and Q1 2018 Investment Letter. BRI is a crucial lender to the informal economy in these rural regions and leads the Indonesian microfinance market. Managers often lose alpha when selling and so did we until we implemented this rule in January 2017. 6th Edition, 2015.

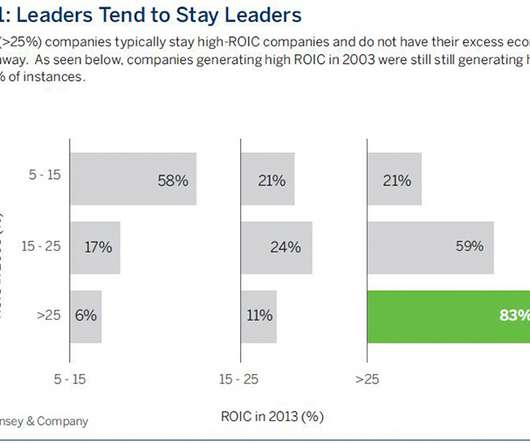

S&P 500® Index, ROIC, 2003-2013 Data based on a McKinsey & Company study, “Valuation: Measuring and Managing the Value of Companies”. Chart reproduced with permission from McKinsey & Company as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition.” 6th Edition, 2015.

Thu, 08/24/2017 - 15:12. For one, real estate tends to move more in concert with the direction of the economy, while stock prices, for example, tend to move in advance of a change in economic fundamentals. We can’t control the economy or predict its near-term direction. This lower correlation is driven by several factors.

Stocks with ultra-high valuations led that charge, as Tesla, Peloton, Pinduoduo and DocuSign all saw double-digit gains. Put simply, the market is willing to project fantastically far into the future to find the cash that can validate nosebleed valuations. 4 Visa , data as of August 2017. Catherine D. Survey period 2016.

Stocks with ultra-high valuations led that charge, as Tesla, Peloton, Pinduoduo and DocuSign all saw double-digit gains. Put simply, the market is willing to project fantastically far into the future to find the cash that can validate nosebleed valuations. Projected Infrastructure needs from 2017-2035 by region or country.

Conversation with the Portfolio Manager: Mid-Cap Growth Strategy achen Wed, 09/20/2017 - 16:43 Over time, the Brown Advisory small-cap growth team, led by Christopher Berrier and George Sakellaris, watched numerous successful investments compound and grow out of their investible universe. Second, we keep a keen eye on valuation.

Wed, 09/20/2017 - 16:43. While valuation is critical to our approach, it occurs near the end of our process. Second, we keep a keen eye on valuation. Conversation with the Portfolio Manager: Mid-Cap Growth Strategy. After that, we set target prices and model multiple scenarios. We target position sizes between 0.5 company.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. Reasons for this tendency are varied. company.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content