This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Dissecting Stock Performance & Valuations A lot of pundits are pointing to an overheated market, but on a 3-year basis, returns are looking more normalized (+8.2% Time will tell. per year) because of the -20% hit on stocks during 2022. Source: Yardeni.com As always, the future is uncertain, and risks abound for next year.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Dot-com hangover/9-11 October 2000 December 2001 -16.5% 9/21/2001 12/31/2001 52 18.9% at the beginning of the year to 16.6x by year-end. to nearly 3.9%

Pockets of attractive valuations exist despite above-average valuations in some high-profile areas of the market. The measure is at 80.7%, exactly where it was a year ago and higher than at any point between July 2001 and February 2020. Following the huge 11.2% But does a strong labor market raise inflation concerns?

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. RITHOLTZ: So you lasted two or three years, and then you get tapped to go to London in 2001. BARATTA: In November of 2001, when I moved over — RITHOLTZ: Sure.

In March 2021, we started to see nonearners’ performance roll over, which is more in line with historical averages; for the 2001–2021 period, earners outperformed nonearners by 3% on an annualized basis. Note: 2001-2021 period is annualized. Exhibit 3: Sector composition of R2G Source: FactSet. GICS Sectors. Data as of March 31, 2021.

In March 2021, we started to see nonearners’ performance roll over, which is more in line with historical averages; for the 2001–2021 period, earners outperformed nonearners by 3% on an annualized basis. Note: 2001-2021 period is annualized. Exhibit 1: Performance of earners vs. nonearners. Exhibit 3: Sector composition of R2G.

(AKA Western India Products Limited) is an Indian information technology, consulting, and business process services company that utilizes robotics, analytics, cloud, and other technological advancements to help their clients spread across six continents to aid and assist them to adapt to digital trends and help them adapt and thrive towards success.

Tech company valuations were cratering, but interest in tech was still high thanks to the exploding popularity of the internet. ” Even for advisors and clients who are interested in alternative investments , software and the broader tech sector might seem like a tough sell right now. “Making it the best it can possibly be.”

After joining the investment industry in 2001, he served as director of research at two firms, creating a small-cap growth strategy at one of them before joining Brown Advisory in 2014. While valuation is critical to our approach, it occurs near the end of our process. Second, we keep a keen eye on valuation.

After joining the investment industry in 2001, he served as director of research at two firms, creating a small-cap growth strategy at one of them before joining Brown Advisory in 2014. While valuation is critical to our approach, it occurs near the end of our process. Second, we keep a keen eye on valuation.

Through a comprehensive range of tailored wealth management solutions, the company serves the highly specialized and sophisticated needs of high-net-worth and ultra-high-net-worth individuals, affluent families, family offices, and institutional clients. The company was incorporated in 2001. The company had an AUM of Rs.

And then I was the beneficiary of the TMT bubble bursting in 2001. SALISBURY: At the simplest level we manage money for our clients. Three main client segments. So that’s essentially what we do from a client segmentation perspective and we do that globally — US, Europe, and Asia. What do they focus on?

He also spent time at Sebus and More Capital before launching his own firm in 2001. But that valuation, to be able to come up with the valuation, to be then able to work in a restructuring process, bankruptcy process, and say, Hey, I think at the end of this, we are buying debt at 50 cents. It could be worth 80, 90 cents.

NORTON: These are portfolios that we’re creating, whether they’re individual stocks, or whether they’re multi-asset portfolios that we offer to financial advisors who in turn offer them to their clients. And so our customer base is financial advisors and their underlying clients. NORTON: They can be.

RITHOLTZ: So let’s talk a little bit about what Stray Reflections is today and who your clients are. The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. The second, and what’s interesting about that period, is the fact that valuations actually peaked in 1961.

This Present is Accounted For: An Overview of Low-Basis Gifting Strategies achen Wed, 11/01/2023 - 11:20 After spending a career helping clients with tax and estate advice, I often see reminders and lessons about my job in the unlikeliest places. And for many years, that was the case for most clients in the U.S.,

The transcript from this week’s, MiB: Aswath Damodaran: Valuations, Narratives & Academia , is below. You’re known as the dean of valuation. He said, oh, dean of valuation, it’s easier to say. So let’s start with the question, what led you to focus on valuation? RITHOLTZ: Right. And I said, why?

So it’s been, you know, back in, in 2001, strategists were telling you to put about 70% of your money in stocks. But no, but I think that where I get my best ideas is from talking to super smart people like you, like our financial advisors, like our hedge fund clients, our, our long only investor clients pensions.

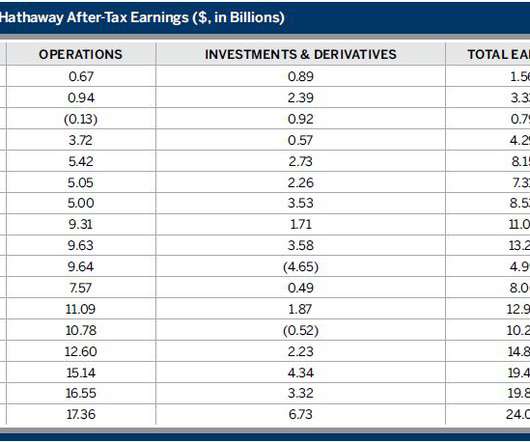

Reported earnings don’t grow every year due to the business cycle and occasional outsized insurance losses (2001), but the progress over time is clear. Low rates also raise valuations for business acquisitions. A quarter-point difference doesn’t sound like much, but on $60 billion [Berkshire’s cash balance], it is still painful.

Next day I had to go to Boston for a client meeting. Not only were they late to start tightening in, in 2001, they they 2021, they were late to recognize inflation peaked in 22. But we had a very mild recession in 2001. 00:07:41 [Speaker Changed] Yeah, yeah. He said, oh, it’d take at least two or three weeks, really?

He really is one of the most knowledgeable people in this space, and not just knowledgeable in the abstract, but helping to oversee just about a hundred billion dollars in client assets. So that was in, that was in 2001 early then. And you know, it’s the same thing when valuation gets outta control too.

RITHOLTZ: In the ‘80s, they were really a financial arm of GE and a way to facilitate its client base. COHAN: His memoir came out literally on September 11th, 2001. And this book comes out on September 11, 2001. So as part of the publicity that got picked up in October of 2001, by the way, the book was a big bestseller.

For the record, Mitchell Madison was formed out of a spinoff of a bunch of McKinsey partners and it was taking kind of a new way, a new approach frankly, to some of the similar types of clients as McKinsey had. And that’s also how I wanna approach things for my clients. Are they mom and pop investors? Are they institutional?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content