This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

(youtube.com) The biz Why Hightower Advisors is buying an institutional investment consultant. riabiz.com) Risktolerance Determining a client's risktolerance is more complicated than having them fill out a questionnaire. advisorperspectives.com) Does risktolerance change in retirement?

Pete is the Director of Sustainable Investing of Earth Equity Advisors, an RIA based in Asheville, North Carolina, that oversees approximately $200 million in assets under management for 250 client households. Welcome everyone! Welcome to the 419th episode of the Financial Advisor Success Podcast ! My guest on today's podcast is Peter Krull.

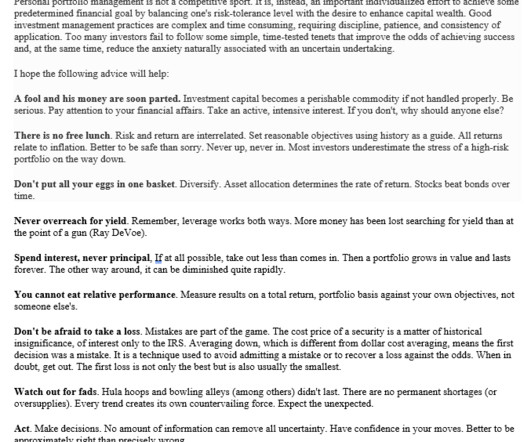

He co-authored Investment Analysis and Portfolio Management , now in its fifth edition. Zeikel famously shared his investing insights in a 1994 letter to his daughter: “Personal portfolio management is not a competitive sport. Investment capital becomes a perishable commodity if not handled properly. Stick to your plan.

What's unique about Nina, though, is how she has developed a "money personality" assessment that allows her to both better understand how her clients' money behaviors might affect the financial planning process and to ensure consistent client service among the advisors at her firm.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risktolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financial planning.

Which, according to Kitces Research on Advisor Productivity, can lead to higher productivity for advisor teams (but can require an investment in staffing and higher-end planning services to meet their complex planning needs).

Also in industry news this week: 43% of wealth management firms are frustrated with the effectiveness of their CRM software, spurred on by challenges with integrations and workflows, according to a recent survey The Social Security Administration this week announced a 2.5%

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

Category: Clients Risk. Determining the client’s risktolerance is not an exact science and requires you to communicate with your client. What Does The Word “Risk” Mean For Your Clients? For financial advisors and their clients, “risk” means the possibility of losing money, investment, or a business venture.

For example, if an advisor recommends an investment that prioritizes the commission they would receive rather than any benefit the client would derive from it, they could incur fines and sanctions for violating their fiduciary duty as an advisor.

Over the years, 2 types of measurement tools have emerged as the standards for assessing risktolerance: 1) psychometric tests, which feature a series of questions (such as, "What amount of risk do you feel you have taken with past financial decisions?") Would you agree to this investment?"). Read More.

Also in industry news this week: How Goldman Sachs’ RIA custodial platform is leveraging the resources of its parent company as it seeks to build momentum amidst a highly competitive environment among custodians How NASAA has changed the substance and/or scoring of the Series 63, 65, and 66 exams From there, we have several articles on college (..)

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

Podcasts Michael Kitces talks setting boundaries with Emily Rassam who is the Senior Financial Planner for Archer Investment Management. morningstar.com) Ryan Detrick and Sonu Varghese talk with Phil Pearlman about the connection between health and wealth planning. open.spotify.com) Cameron Passmore and Benjamin Felix talk with Prof.

Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. High deductible health insurance plans . These types of plans are becoming more common with employers and are available privately as well. How the HSA works . Click To Tweet.

Is this a valid investment strategy? As far as your investments, I think you’ll agree that the outcome of the game should not dictate your strategy. Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Costs matter.

The post Investing for Retirement: Strategies for Long-Term Success appeared first on Yardley Wealth Management, LLC. Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. What lifestyle do you envision?

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirement plans.

Your investing strategy is a personal approach based on your goals, life stage and risktolerance. There are so many different ways to invest, but two of the most common methods youll find are active and passive investing. What is active investing? What is passive investing?

It can be designed to accentuate your best features, made in a color and style that will both please you and be appropriate for the occasion in which it will be worn. The same is true of investment portfolios. The use of advanced investment strategies. One basic and popular strategy for building a portfolio is the 60/40 model.

Exploring the Benefits of Financial Planning appeared first on Yardley Wealth Management, LLC. With the complexity of modern financial decisions and the abundance of online resources, you might wonder if speaking with a financial planner is truly worth the investment. The post Is Talking to a Financial Planner Worth It?

Investment and risk are two closely related concepts. Risk refers to the potential for loss or negative returns when you invest your money in a market-linked security. There are different types of risks, including market, credit, inflation, and liquidity risk, among others. What is risktolerance?

Apart from new laws and changes in regulations, it is also important to pay attention to emerging investment trendsevery year. The financial planning industry is constantly undergoing change. This article will discuss some of the most pivotal financial planning industry trends to watch out for this year.

Enter bucketing, a powerful strategy that helps simplify your financial planning by categorizing your assets into three time-based buckets: today, tomorrow, and the future. By dividing your investments into these three buckets, you help create a clear plan for how and when your money will be used. What Is Bucketing?

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. Focus on risk. Do nothing.

Bonds, however, are more stable investments that provide income, but have much less upside. while bonds are broken down by duration and sectors (for example government bonds such as municipal or Treasury bonds or corporate bonds, including investment grade or high yield bonds), etc.

Start planning early. Yet far too many professionals delay the planning process. They max out a 401(k), skim through Social Security rules, maybe even dabble in stocks, but when retirement day approaches, they realize their savings, insurance, or investment mix just doesn’t add up. And the best way to do that? Doing it right?

If you are someone who loves a good Do It Yourself (DIY) challenge, whether it is fixing your own car or kitchen sink, you might think investing is just another task you can master on your own. Self-investing, or DIY investing, is incredibly popular. What is self-investing, and what are its pros and cons?

In the world of investing, this could not be truer. Long-term investing is where you put your money to work and give it time to grow. Below are 5 long term investment strategies you need to know about in 2025: 1. This is the segment you can explore for long-term investing. Because they hold real value. Why does it work?

Knowledge and Personalized Planning Financial advisors can bring a wealth of knowledge from extensive education and experience, helping enable them to craft tailored strategies that align with your unique financial goals. This personalized approach can help you make financial decisions that are well-informed and strategically sound.

The post Staying Disciplined: How to Stick to Your Financial Plan Despite Market Volatility appeared first on Yardley Wealth Management, LLC. Staying Disciplined: How to Stick to Your Financial Plan Despite Market Volatility Introduction: Market volatility is a fact of life for investors.

In this article, we will explore three popular savings and investment options: 529 Plans, Roth IRAs, and Real Estate. Each has unique benefits and drawbacks, and understanding these can help you decide which fits best with your financial situation, risktolerance, and goals.

As you work toward your financial goals, regularly reviewing your investment portfolio is essential. Whether youre new to investing or have years of experience, taking a step back to evaluate your strategy can help ensure that your portfolio remains aligned with your objectives, especially in times of market uncertainty and volatility.

Many of us are covered by one or more types of defined contribution retirement plans, such as a 401(k), 403(b), 457, or any of a number of other plans. What many of these plans have in common is that they are referred to as Cash Or Deferred Arrangements (CODA), as designated by the IRS. So, what should you do about this?

Financial planning can take your money game up a notch by bringing clarity, strategy, and intention to your financial life. A healthy financial plan gives you the tools to take control of your finances and start living your life with passion, purpose, and freedom. So what’s the value of a financial plan? Tax Planning.

The beauty of our approach—building investment strategies based on academic research and rebalancing back to the target risktolerance as markets move—is that we can find comfort in these times by revisiting the core tenets of our belief systems.

For investors, this may be a time to revisit your financial plan, not to panic. Consider speaking with a financial advisor about risktolerance and strategies like tax loss harvesting. Stay tuned for next week. Andres Disclosure: This material provided by Zoe Financial is for informational purposes only.

In this article, we’ll break down the concept of waterfall wealth distribution, its benefits, and how it compares to traditional investment strategies. We’ll also explore the role of income tiers, provide real-world case studies, and highlight key considerations when implementing this strategy in your financial plan.

Exercise strategy: Timing: Consider the tax implications of exercising vested options before or after the IPO, timing of sales, and tax planning opportunities. Sales and trading plan: Taking profits: Once the lockup period ends, consider diversifying your holdings to reduce risk.

Investing in an Individual Retirement Account (IRA) is an excellent way to save for retirement. However, selecting the right investments for your IRA can be challenging. In this article, we will explore some strategies to help you choose the best investments for your IRA.

Diversification: Diversifies investments across different market capitalizations. Balanced Risk: Merges stability from large-caps with growth prospects of mid and small-caps. crore 1-Year Return : ~28% Expense Ratio : ~0.65% Why it stands out : HDFC brings stability and a conservative investment style.

Think you don’t have enough money to start investing? You can learn how to start investing even if you start your investing journey with just $100. Although the amount you invest might start out small, it can be a turning point in your finances. Investing money for beginners doesn't have to be hard either!

You’ll be rewarded if you can invest it for the long haul. As this compound interest calculator demonstrates, investing $30,000 at a return of 8% for 20 years will leave you with $138,828. But where should you invest your $30,000? Table of Contents 16 Best Ways to Invest $30,000 in 2023. Invest in ETFs.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content