This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirementplanning process involves simulating whether the client's assets will last through retirement. That emotional connection supports confidence and increases the likelihood that the client will stick with their plan and stay committed through both good markets and bad.

Also in industry news this week: In the continued absence of formal SEC guidance on advisory firm use of Artificial Intelligence (AI), many firms are taking a curious, but cautious, approach toward adopting AI-powered tools A recent report identifies the growing total wealth controlled by women in the U.S.

Retirementplanning is a journey that generally takes decades to complete and most of us start out along the do-it-yourself path. More than likely, your first step was to enroll in an employer-provided plan such as a 401(k) or setting up an individual retirement account, also known as an IRA.

Unlike most types of retirementplans, the SEP IRA is funded by the employer. A SEP IRA (Simplified Employee Pension Individual Retirement Account) is a type of retirementplan specifically designed for self-employed individuals and small business owners. What is a SEP IRA?

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirementplanning.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

In this episode, we talk in-depth about how Seth built and provides his input deliverable (which calculates the appropriate amount of tax-exempt housing allowance pastors can take based on their individual circumstances, and even prepares a request and subsequent resolution that the Church's Board can then use) to demonstrate his expertise to prospective (..)

Enjoy the current installment of "Weekend Reading For Financial Planners"– this week's edition kicks off with the news that a recent analysis from Morningstar suggests that the Department of Labor's (DoL's) new Retirement Security Rule (aka Fiduciary Rule 2.0)

In addition, the TSP updated its website and introduced a smartphone app, which required participants to create new credentials and verify their personal information.

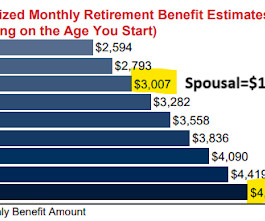

While future retirees can find nonreduced benefit estimates on their Social Security statements or online accounts, those already receiving benefits don't have access to this information – making it necessary to find a different way to predict how much their payments will increase once the law is fully implemented.

Also in industry news this week: A new advisor benchmarking study indicates that high-growth firms are excelling in 3 areas: client acquisition, "relationship alpha", and strategic scale A recent survey indicates that while advisors increasingly are leveraging home office investment models to save time and scale more efficiently, they often customize (..)

Also in industry news this week: The SEC settled its first charges related to its new marketing rule with a firm that advertised 2,700% annual returns A survey suggests that older Americans prefer the term "longevity" to "aging", perhaps informing the way advisors discuss related issues with their clients From there, we have several articles on retirement (..)

Also in industry news this week: The SEC this week announced a proposed rule that would require RIAs to collect and verify their clients' personal information in an effort to prevent illicit activity, though many firms likely are taking many of these steps already Why larger RIAs and those that have been acquired tend to have worse client and staff (..)

To start, the agreement should contain basic information about the adviser-client relationship, including who the client is (e.g., a single person, a couple, a business, or a retirementplan) and the date on which the agreement will become effective.

To start, the agreement should contain basic information about the adviser-client relationship, including who the client is (e.g., a single person, a couple, a business, or a retirementplan) and the date on which the agreement will become effective.

The answer largely depends on your financial situation, but understanding the value these professionals bring can help you make an informed decision. RetirementPlanningRetirementplanning is one area where talking to a financial planner proves particularly worthwhile.

Today’s Animal Spirits is brought to you by YCharts and Fabric: See here for 20% off your initial YCharts professional subscription Go to meetfabric.com/spirits for more information on life insurance from Fabric by Gerber Life On today’s show, we discuss: How Individual Retirement Accounts Changed the Stock Market Forever Social Security: (..)

However, there may be circumstances where it could make very good sense to separate your contributory IRAs from 401(k) plan rollovers – and it pertains to creditor’s rights. The article mentioned at the outset includes links to state law information with regard to these kinds of situations.

RetirementPlanning: Looking Beyond the Basics For 2025, it’s essential to think beyond the standard “maximize your 401(k)” advice. While that remains important, consider diversifying your retirement strategy. Consider whether your business structure optimizes both liability protection and tax efficiency.

Attorneys are telling us that 2024 is the time to review and change your estate plan as the lines may be out the door in 2025 for taxpayers wanting to make last minute changes to take advantage of the higher exemption amount. Lastly, I allocate the retirementplan contributions between Roth and Traditional 401(k) accounts.

Leave Space for Responses A common mistake is overloading posts with too much information. Instead of listing ten tips for retirementplanning, share your top three and ask, What would you add to this list? For instance, many people feel overwhelmed by retirementplanning.

Retirementplanning is deeply personal, and for single individuals, it comes with both unique opportunities and important considerations. Whether by choice or circumstance, retiring solo means you’re in full control of your financial decisions, but you also face distinct planning challenges that require thoughtful strategy.

Ask them directly about ALL forms of compensation they will receive from working with you, and if they will disclose this information on an ongoing basis. Financial Fraud – Tips to Protect Yourself Annuities: The Wonder Drug for Your Retirement? Ask how they select the financial and investment products they recommend to clients.

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it.

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it.

AI-powered search engines, including Googles AI Overviews and tools like ChatGPT, now generate responses by pulling information from multiple sources. AI prioritizes information from reputable sources secure media mentions in trusted finance publications and news sites. How Can Financial Advisors Adapt to AI-Powered Search Engines?

However, they also frequently work with clients whose businesses sponsor employer retirementplans that must adjust their systems and raise workers’ awareness to enable them to fully tap into their benefits. This article should not be considered tax or legal advice and is provided for informational purposes only.

Pivoting, the Wall Street Journal had a very short interview with Alicia Munnell as she retires from the Boston College Center for Retirement Research at age 82. Munnell along with Teresa Ghilarducci are like the aunties of retirement which I am saying in a positive way. People shouldn't put effort into retirementplanning?

Today I have Brian Williams of Northshire Consulting and were going to be talking about how financial advisors can help improve 401k plan access to the American people who are working at small businesses who currently do not offer them. What if the local baker had a 401k plan? Why are small business owners not offering 401k plans?

It's not like this is a bad problem but there can be expensive mistakes made in this sort of scenario I want to believe that it is not realistic that if someone has a set of maybe five or six assumptions that go into their retirementplan, that not all of them would have a worst case outcome.

Where Sam writes about FIRE, he asked Bengen what a safe withdrawal rate would be for someone who retired, planning to need the money to last for 50 years instead of the typical 30 used for planning purposes. Now, Bengen says the worst case has bumped up to 4.7%, I'm not sure I'm on board with that (listen to the podcast).

trillion market for 401(k)-type retirementplans as crucial to this growth. " I am not saying people should check their 401ks every day but any day that someone does check, the information should be current. This quote made my eyes bug out. I'm always going to read something like that to mean we need more suckers.

I’m not discounting the great information CNBC and the rest of the financial media provides, but you need to take much of this with a grain of salt. This is a good time to lean on your financial plan and your investment strategy and use these tools as a guide.

Be cautious of unsolicited calls: Medicare will never call you to sell you anything or to ask for your personal information. Know the common scams: Common scams include offers for free medical equipment or tests, fake Medicare plans, and calls claiming you need to provide information to keep your coverage. Talk to us today!

Retirementplanning, like any type of robust financial planning, should include stress testing your investment strategy and financial plan. Over the long term, as your life changes, you’ll need to consider whether your weightings in stocks vs bonds is appropriate. After all, volatility is a when , not an if.

Take advantage of tax-advantaged retirement accounts such as 401(k)s, IRAs, and Roth IRAs to maximize your contributions and benefit from tax-deferred or tax-free growth. Learn more about retirementplan options here. Aim to contribute as much as you can afford to these accounts each year to accelerate your retirement savings.

Both the Mega Backdoor Roth IRA and Mega Backdoor Roth 401(k) allow the additional contribution of funds to retirementplans after pre-tax and Roth contribution limits have been reached. Roth IRAs are also not subject to Required Minimum Distributions (RMDs), allowing more flexibility in retirementplanning.

Finding more information is also easy, as the navigation is well-designed with a straightforward menu. The site then goes the extra mile by allowing visitors to sign up for a free assessment to see how their retirementplanning is going and how they could improve it.

The fundamentals of Roth and traditional IRAs Traditional IRAs have long served as a cornerstone of retirementplanning, offering immediate tax benefits through deductible contributions while deferring taxes until withdrawal. Ready to explore whether a Roth conversion aligns with your retirement strategy?

Catch-up contributions and additional retirement savings vehicles, like IRAs, can help you increase your retirement savings. Check out our post, RetirementPlanning: What Will Work Best for You? , for more information. For more information on the services offered, contact Katie today.

Photo credit: jb Employers have been giving us lots of opportunities to make this decision of late: when leaving an employer, whether voluntarily or otherwise, we have the opportunity to rollover the qualified retirementplan (QRP) such as a 401(k) from the former employer to either an IRA or a new employer’s QRP.

When you take the savvy step of hosting educational seminars and webinars, you are strategically positioning yourself as an authority while providing valuable information to potential clients. Instead of a hard sell, youre offering insights that help them make informed financial decisionsbuilding credibility and goodwill in the process.

Spending $10,000 you weren't expecting on some sort of repair would suck but having that completely undo a retirementplan would suck worse. The information, analysis and opinions expressed herein reflect our judgment and opinions as of the date of writing and are subject to change at any time without notice.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content