This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

This week, Orion announced they were making it easier for those in need of free financial planning to find help, TIFIN and Morningstar partnered to enhance their AI-powered distribution platform and eMoney responded to recently-passed legislation with taxplanning upgrades.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year.

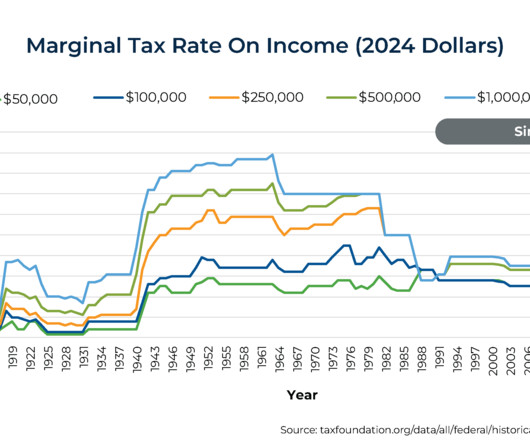

Because not only were very few households actually subject to the 1950s-era top tax rates (which were triggered at the equivalent of over $2 million of income in today's dollars), but the long decline in nominal tax rates has also come with the elimination of many loopholes and deductions that have resulted in more income being subject to tax.

A potential compromise during the lame-duck Congressional session could see a boost to the child tax credit and extended tax breaks for businesses. From there, we have several articles on taxplanning: How advisors can add value for their clients by managing their exposure to mutual fund capital gains distributions.

The IRA and Roth IRA contribution limits are unchanged but income eligibility for tax-deductible IRA contributions and Roth IRA contributions have changed. Also updated: health savings accounts, flexible spending accounts, estate and gifting limits, qualified charitable distributions and other cost-of-living adjustments.

For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs. Here are some of the most common RMD questions and planning opportunities for investors. How to take RMDs and avoid any taxes (legally of course).

This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on taxplanning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

Also in industry news this week: 2 House committees this week advanced legislation that would halt implementation of the Department of Labor's new Retirement Security Rule, which, combined with ongoing lawsuits, threaten to derail the regulation either before or soon after it becomes effective in late September A Federal judge has put the future of (..)

Qualified Charitable Distributions (QCDs) QCDs are direct transfers of funds from an individual retirement account (IRA) to a qualified charity. or older, QCDs offer a strategic way to contribute to charity while meeting required minimum distribution (RMD) obligations. Available to taxpayers aged 70.5

We would like to take this opportunity to remind you about your annual Required Minimum Distribution (RMD). As you may know, the Internal Revenue Service (IRS) requires that you take an annual distribution from your retirement accounts starting with the year in which you turn 72 years old and every year thereafter. Annual deadlines.

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

Estate planning is one of the most important steps in securing your financial legacy, but its also among the most complex. Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming.

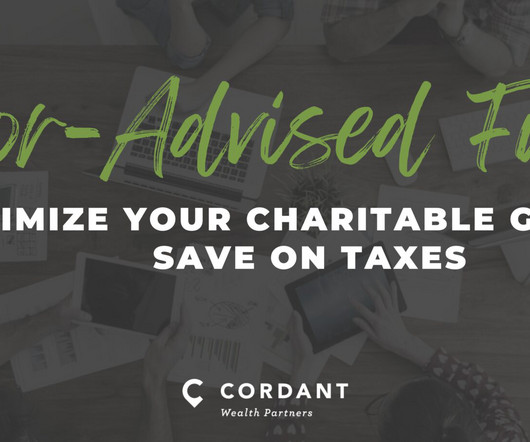

Donor-advised funds (DAFs) have emerged as powerful tools that deliver this exact combination, providing immediate tax advantages while offering flexibility to recommend grants to qualified organizations over time. DAFs also introduce welcome simplification at tax time by consolidating multiple charitable activities under a single receipt.

We also get you up to speed on the tax benefits of using a DAF. If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made.

Cost-saving taxplanning can be much more difficult to implement after your company is well-established and has reached the stage where an IPO, merger, or acquisition becomes a likely event. The first three options are pass-through entities, so profits and losses are distributed to the owners who are taxed on them.

Whether you are contemplating forming an LP or already operate one, gaining clarity on tax matters can optimize your financial outcomes and ensure compliance with state and federal regulations. LPs are governed by a partnership agreement that outlines the roles, responsibilities, profit distribution, and other operational details.

is significant legislation signed into law on December 20, 2022, and is expected to have several impacts on retirement income planning. It contains several provisions designed to improve Americans' retirement security, including later required minimum distributions (RMDs), 529-to-Roth rollovers, and other taxplanning opportunities.

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

No required minimum distributions (RMDs) for the original account owner Unlike IRAs and qualified retirement plans, a Roth IRA is unique in that required minimum distributions are not required during the original account owners lifetime. A spouse may also elect to defer RMDs if they inherit the account.

With proper planning, certain tax obligations can be legally deferred, reduced, or in some cases eliminated entirely. To maximize the value you ultimately receive from your exit, incorporating comprehensive taxplanning into your strategy is highly advantageous.

In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations. From maximizing deductions to managing capital gains, we’ll cover everything you need to know about smart taxplanning.

Retiring early is also even more difficult without taxable assets as you’ll need to bridge the gap before penalty-free distributions from 401(k)s or IRAs begin, perhaps to cover medical expenses. Dividends, interest, or capital gains distributions from mutual funds and ETFs received during the year are taxable annually.

For example, if you convert $50,000 and it grows to $100,000 in a Roth IRA over the next several years, that essentially results in $50,000 tax-free dollars. Keeping your funds in a traditional IRA only defers taxation on the full amount until the funds are distributed at some point in the future.

Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and taxplan. An endowment offers benefits that can extend beyond tax deductions and financial efficiency. The usage policy establishes the purposes for which the charity can use the fund distributions.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning.

The Tax Cuts and Jobs Act of 2017 eliminated recharacterization, transforming Roth conversions into permanent decisions requiring thorough analysis before execution. Roth IRAs offer unique advantages including tax-free growth, no required minimum distributions during the owner’s lifetime, and potential tax benefits for heirs.

Instead, partners (investors) are taxed directly on their share of the fund’s income, gains, losses, and deductions, regardless of whether those amounts are actually distributed. Each partner receives a Schedule K-1, which reports their share of the fund’s tax items. FIRPTA planning using a U.S.

This will allow you to bunch your donations in a single year but then distribute them over a long period of time. [1] 1] The benefit to this is that you can still gain the tax advantage of a large, itemized donation but can distribute your donations over more than just one year. [1]

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The simple examples above only illustrate the state tax impact, but federal tax implications will also apply. Further, both examples ignore other sources of income, such as wages, pre-tax retirement account distributions, dividends, etc., that could increase the tax due from the surtax.

If you are expecting sudden wealth from the sale of a business or other liquidity event, then it may not make sense to do a conversion in the same tax year, but could be worth considering alongside cash allocation discussions. The example above assumes the couple does not need the full distribution from the IRA to meet lifestyle expenses.

What Are Qualified Charitable Distributions (QCDs)? For those over 70½, you might already be familiar with Qualified Charitable Distributions (QCDs). For years, QCDs have allowed people to donate directly from their IRAs without paying taxes on those distributions.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. Raise the required minimum distribution age. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033.

The initial distribution of shares to your relatives would be classified as a gift, and the annual income from the gift would be taxed to the relative. You can make federal gift tax-free gifts of up to $16,000 per year per recipient under the annual gift tax exclusion. an affiliate of LPL Financial.

A financial advisor can help with maximizing your retirement income through taxplanning After retirement, your income sources may become limited to pensions, Social Security benefits, and investment income. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income.

By exploring these nuances, you can better appreciate the tax advantages and responsibilities that come with running a Co-op. Understanding Co-op Taxes Key Tax Deductions and Credits Taxplanning tips for a Co-op Final Thoughts on Understanding Co-op Taxes Partner with Harness for Expert Tax Support What Is a Cooperative (Co-op)?

A little bit of effort and forward thinking during our summer and fall months will lead to a much more palatable and, potentially, financially advantageous tax season the following year. The reason for this is quite simple – taxplanning requires actual planning. Timing: Ideally earlier in the year.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content