This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

The money goes into the account on a pre-tax basis much like a traditional 401(k) or IRA. This is a great opportunity for those who earn too much to make pre-tax contributions to a traditional IRA. Those who have made the maximum contributions to their 401(k) have another pre-tax savings option available to them as well.

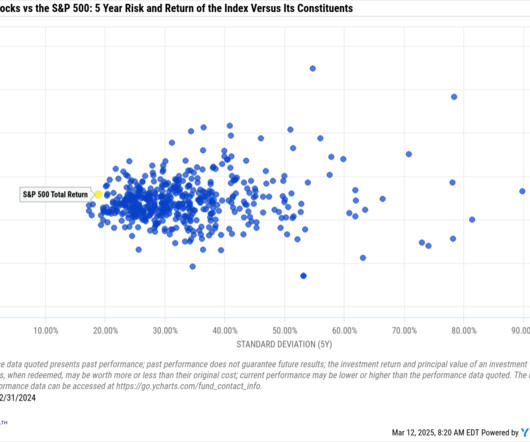

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median stock underperformance was almost -10%.(J.P. Morgan Private Bank) 6 ways to manage a concentrated stock position In no particular order, here are some strategies to reduce the risk of concentrated stock holdings.

It can also help reduce taxes and make life easier for your family during difficult times. Draft a will: Choose how your assets will be distributed and name guardians if you have minor children. A qualified local attorney can help you create a plan that honors your wishes and minimizes taxes. Yet, many people put it off.

Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and tax plan. An endowment offers benefits that can extend beyond tax deductions and financial efficiency. The usage policy establishes the purposes for which the charity can use the fund distributions.

They can assess your financial situation, long-term goals, risktolerance, and investment preferences to create personalized strategies. They can also help you optimize your savings and investment plans, ensuring that you maximize your earning potential while minimizing risks. Tax planning is not solely about federal taxes.

In the normal course, you don’t even need to file any additional tax or reporting documents with the IRS. But that distinction was eliminated for tax years beginning in 2020 and beyond. Tax-deferral of Investment Earnings Both a Roth IRA and a traditional IRA enable your funds to accumulate investment income on a tax-deferred basis.

I’m a big fan of the Roth IRA and investors that understand it’s massive tax-free benefits are also. A Roth IRA is a type of individual retirement account (IRA) that allows you to contribute after-tax money and withdraw it tax-free in retirement. What is a Roth IRA? What are The Benefits of a Roth IRA?

It’s also tax-preferred at the federal level and completely tax-free in many states. There are approaches to investing in retirement that seek to align your risktolerance with your need to turn investment assets into retirement income. You are encouraged to seek advice from your own tax or legal professional.

Distributions from the annuity with a living benefit rider will be taxed differently depending on the type of account and whether or not the benefit requires annuitization. We’ll also highlight the differences for the three main types of annuity ownership: nonqualified, Roth Individual Retirement Annuity (IRA) and pre-tax IRA.

An individual who learns to manage $4,000 a month after taxes will be equipped to manage $14,000 or even $40,000 a month as their earnings increase over time. By Lisa saving $6,000 into the plan, she reduces her federal taxable income to $94,000, meaning she will have a lower annual tax liability. Build Positive Financial Behaviors.

Real Estate: Best for Predictable Gains + Tax Benefits. Real estate also has valuable tax benefits, like depreciation expense. And since they rarely trade stocks, the capital gains they generate will usually be long-term, giving you the benefit of lower long-term capital gains tax rates. See Public.com/disclosures.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. RiskTolerance Identify and consider your risktolerance when setting your financial goals. Your advisor must have the expertise to assist with this.

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median underperformance was almost -10%. And tax implications, concentration, risktolerance and other factors should always be considered. Big losses are common.³ Strategies to diversify. Disclosures.

Your asset allocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. This is critical because without rebalancing, you may be taking on more risk than necessary to meet your goals. As you approach retirement, managing risk is even more important.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. RiskTolerance Identify and consider your risktolerance when setting your financial goals. Your advisor must have the expertise to assist with this.

Spread your investments across different asset classes Asset allocation involves distributing investments across different asset classes to balance risk and return. Alternative investments for diversification : Commodities, hedge funds, and private equity can reduce overall portfolio risk by adding non-correlated assets.

Asset allocation aims to balance risk and reward through a portfolio composition of different kinds of assets. If not allocated efficiently, you may become subject to a slew of taxes and other charges. As your portfolio is exposed to various markets, you can reap the benefits of these securities while effectively mitigating your risk.

It offers a way for employees to save for retirement on a tax-deferred basis, while also requiring employers to make contributions on behalf of their employees. Another key benefit of a Simple IRA is that it allows employees to make contributions to the plan on a pre-tax basis. Benefits of the Simple IRA vs 401k. Do not overlook this.

10 steps to manage a financial windfall Expert tip: Keep living your life normally Factoring in taxes How do you deal with sudden financial windfall? Tax refunds that are more than you expected. Also, determine how your money and other assets will be distributed in the case of an unfortunate event.

Tax-Efficient Management of 401(k) and ESOP After Employer Separation Efficient tax management of 401(k) and ESOP holdings post-employment is critical to help secure a financially stable retirement. Additionally, upon retirement, strategically withdrawing from retirement accounts can further optimize tax efficiency.

This tax-advantaged savings vehicle allows you to accumulate wealth steadily over a lifetime of diligent saving and investing. Start tax planning A traditional 401(k) is a pre-tax account. This tax-advantaged account offers you a tax deduction in the year you contribute. However, there is a trade-off to consider.

Invest in a Health Savings Account (HSA) An HSA is a tax-advantaged savings tool that can be used to build retirement health savings. It allows you to set aside money specifically for qualified medical expenses while enjoying several tax benefits along the way. However, it is important to stick to eligible expenses.

You make payroll contributions to this account on a cyclical basis which distributes funds to your portfolio and increases your savings over time. There are also important tax considerations with this approach which usually results in a higher tax bill. . Value stocks tend to be more cost-effective and have less risk attached.

Whether you opt for a fixed annuity that guarantees a consistent payout or a variable annuity that allows for growth potential based on market performance, you have the flexibility to choose a plan that aligns with your financial needs, goals, and risktolerance. This helps you sustain your retirement for a longer time.

The questions you ask your financial advisor should cover various aspects of your portfolio, such as fees, taxes, risk, and others. It is essential for your investment portfolio to align with your unique financial goals, risktolerance, and time horizon. Are there any tax implications associated with my investments?

Without effective personal financial management, you risk losing money to poor budgeting, poor tax planning, or even just to inflation. Taxes and Inflation: The Silent Killers of Returns Annual returns on investments are affected by both inflation and taxes, and they can drastically reduce the actual returns of your investments.

This retirement account lets you invest with after-tax dollars, meaning you don’t get a tax benefit upfront. However, your money grows tax-free, and you won’t have to pay income taxes when you withdraw the money after retirement.

Qualified employer retirement plans allow tax-deferred growth, which means accounts are not subject to taxes on dividends or capital gains until proceeds are distributed at a later date. By Ellie saving $20,500 into the plan she reduces her federal taxable income to $239,500, meaning she will have a lower annual tax liability.

As a couple aged 65 in 2023, you may need approximately $315,000 saved (after tax) to cover your healthcare expenses. Secondly, the HSA provides distinct tax advantages, making it an attractive component of a comprehensive retirement plan. It is easy to focus on accumulating a nest egg for a comfortable future.

Create a diversified investment portfolio to reduce risk and enhance your returns A sum as large as a million dollars can offer you a comfortable start to diversify your portfolio. Before you start investing, it is essential to also know your investment goals and risktolerance. How much risk are you willing to take?

Who doesn’t love a great tax break? Why not make best use of your tax-planning powers when you do? At a glance, it would seem qualified dispositions are the way to go: Qualified dispositions: Proceeds are taxed at (usually lower) long-term capital gains rates. Fewer taxes are better, right? Is this a risk worth taking?

Step 2: See if the financial advisor conducts an annual tax review Ensuring that your financial advisor reviews your tax return annually is a crucial step in maximizing your financial benefits. An effective financial advisor should be proactive in reviewing your tax plan before the year-end.

You can set up an account in minutes, and Betterment offers added benefits like portfolio rebalancing, dividend reinvestment, and tax-loss harvesting. Collect Dividends Risk level: Moderate When I talk about collecting dividends, I am of course talking about investing in dividend stocks.

Their primary objective is to ensure that the assets are managed & distributed according to the wishes of the client. and a risktolerance analysis, all of which are sculpted around an individual’s circumstances. Updated with Regulations: Estate laws and tax implications can be complex and ever-changing.

Betterment makes it easy to invest automatically, and they ask you questions to assess your risktolerance and get a better handle on your goals. This type of retirement account is only available to individuals whose incomes fall under certain thresholds, yet it lets you save money for retirement on an after-tax basis.

But life inevitably brings changes to every client’s risktolerance—usually because their circumstances, aspirations and obligations evolve over time—so there may be very valid reasons for making extensive adjustments to an existing plan.

But life inevitably brings changes to every client’s risktolerance—usually because their circumstances, aspirations and obligations evolve over time—so there may be very valid reasons for making extensive adjustments to an existing plan. With that backdrop, we highlight several positive factors: Income Tax. Tax Loss Harvesting.

Planning for retirement is one of the biggest financial challenges you will ever face, and a financial advisor can help you adopt a strategy that can take you to your goals, mitigate risk, and adapt to the changes that will inevitably come your way. Retirement planning can be a long-term journey, and a lot can change along the way.

” To learn more about the tax implications of rental income, you can refer to the IRS publication IRS Publication 925: Passive Activity and At-Risk Rules. Companies distribute a portion of their profits to shareholders as dividends, providing you with a passive income stream.

Moreover, if you have family members involved in your business, you need to consider aspects like business succession, asset distribution (from the business, if any), equity sharing, etc. If you have good risktolerance, you can look to invest in quality stocks that have the potential to give you good returns in the future.

Further, you can save money otherwise spent on tax if you take a home loan. Home loan tax benefits can lower your taxable income and help you save money. Premature withdrawals attract a 10% penalty, along with applicable taxes. A traditional IRA is a tax-deferred account. A Roth IRA is the opposite of a traditional IRA.

Its best use also depends on the investor’s investment philosophy, risktolerance, time horizon, and objectives. Dominating the consideration of how owning AI stocks could fit into each client’s holistic, long-term investment plan is the risk. How Does This Align with My Financial Plan?

The 401(k) often offers a traditional pre-taxed account and a post-taxed Roth account, with both sourced in a blend of stock and bond options the employee must choose and maintain with the appropriate risktolerance until retirement. It provides reliable income, respectable growth, sufficient liquidity and tax efficiency.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content