This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While many people approach their financialplanning with careful strategy, its easy to overlook the same level of intention when it comes to charitable giving. Lets explore several potentially effective financialplanning tools that may help you maximize your impact and meet your philanthropic goals.

Sponsored Content Alternative Investments Summit: Navigating the New Frontier Alternative Investments Summit: Navigating the New Frontier Apr 11, 2025 Cetera alternative investments Alternative Investments Cetera Launches First in a Planned Line of Alternative Investments Models Cetera Launches First in a Planned Line of Alternative Investments Models (..)

PEPs seem to be a great solution to the explosion of plan formations, but the downsides are real. allowed financial service providers to act as the pooled plan provider, the question is whether PEPs are the Wild West, with programs popping up like frogs during a monsoon. 4, 2025) 11 Investment Must Reads for This Week (Aug.

There is something to be said for owning your own distribution channel,” he said. His work has appeared in The New York Times , WealthManagement.com , FinancialPlanning , RIABiz , InvestmentNews , PC Magazine , numerous blogs and several books, including Technology Tools for Today's High Margin Practice.

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

If you’re heading into retirement—or already there—there’s one important rule you’ll need to plan for: Required Minimum Distributions , or RMDs. Once you reach a certain age, the IRS requires you to start taking money out of your tax-deferred retirement accounts like traditional IRAs and 401(k)s.

Maximize Your Retirement Contributions: Enhancing your retirement savings not only secures your future but also offers immediate tax benefits. For 2024, the IRS has increased contribution limits: – 401(k), 403(b), and most 457 plans: You can contribute up to $23,000.

According to Alge, the firm initially divided its RIA outreach into two distribution channels: “institutional” (which largely included RIAs and professional buyers) and traditional retail (including wirehouses and regional IBDs, among other segments). However, Alge acknowledged that most RIAs don’t fit neatly into one approach.

When carry is gifted or transferred before exits begin, it consumes very little of a partner’s lifetime exemption but still allows financial upside to accrue to the next generation of a partner’s family. Once the fund reaches its harvest stage and starts producing distributions, however, the value of the carry increases quickly.

The PLR addressed the application of IRC Sections 4941 (self-dealing), 4942 (qualifying distributions) and 4945 (taxable expenditures) in a structure involving tiered grant-making through intermediary foreign organizations. Grantmaking Through Foreign Organizations A U.S. Related: Will Hulk Hogan’s Estate Bring the Drama?

Each discussed how providing a more holistic approach to distribution-phase planning in their practices can amp up organic growth for advisory firms. I cannot say enough about how well received this last session was by advisors, several of whom came up later to say thanks.

At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations. This guide consolidates what we’ve learned to help you refine, update, or pressure-test your current retirement and estate strategy with confidence.

Healthcare costs are rising at a pace that demands attention, particularly for individuals nearing retirement. Without proper planning, healthcare expenses can quickly consume a significant portion of retirement savings. Healthcare financial advisors are invaluable in helping individuals tackle this complexity.

Imagine yourself on your last ride home from work on the day you retire. It probably depends on whether you have a strong plan in place for income during your retirement years. Having a retirementplanning checklist can help make this final commute the time of reflection and joy it should be.

Related: Zephyrs Adjusted for Risk: Growth Strategies at Gabelli Funds Earlier this year, SMArtX partnered with BondBloxx to construct and distribute multi-asset model portfolios to financial advisors. Raymond James Practice Mercer Advisors Lands $1.2B The deal gave the company access to BondBloxx’s fixed-income ETFs.

It plays a crucial role in helping people achieve financial stability, prepare for retirement, and leave a lasting legacy for their families. Yet even the best financialplans can stumble. Draft a will: Choose how your assets will be distributed and name guardians if you have minor children. The result?

Checklist: Year-end Tax Planning Strategies Review the following tax strategies with your tax advisor and/or financial advisor before the end of the year. Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income.

This can come from dividends, interest, rental income, and distributions from brokerage or retirement accounts. For example, if funds are invested in a brokerage or retirement account, they may generate dividends or interest, which contribute to total earnings. Save Saving involves setting aside money for future needs or goals.

When you actively contribute to your workplace retirement account, invest in a separate portfolio , and funnel money into your savings account, it can be difficult to open – let alone manage – another account. IRAs are a great addition to your retirement savings journey. Do you plan on using the funds for K-12, college, or both?

The most successful financial advisors are creating video content that addresses their audience’s most pressing concerns. A timely video explaining how recent Federal Reserve decisions might impact retirementplanning can position you as the go-to advisor for your niche. Check out our financial advisor case studies.

Earlier this year, the firms launched two funds for wealthy clients investing in bonds and private credit, and they could eventually market the slate of strategies to 401(k)s and other retirement funds sitting on more than $12 trillion. Blackstone Inc., and State Street Corp. have started products this year. BlackRock Inc.,

Key Takeaways: Maximize available deductions through strategic planning Consider timing of income recognition and deductions Leverage investment and charitable giving strategies Stay informed about AMT implications Regularly review and update your tax strategy FAQ Q: What are the best tax deductions for high-income earners?

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. The absence of required minimum distributions during the owner’s lifetime.

Do you want to be a distribution platform with an emerging high-net-worth base with a cross-section of private assets in way that is self-directed, guided or ‘do it for me.’ That’s a different approach from what Yieldstreet had been doing, correct? Or do you want to be an asset manager and asset manufacturer, because you are doing both.”

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. Start planning early. And the best way to do that?

Harnessing Tax-Advantaged Savings Retirement accounts and health savings plans offer the dual benefits of saving tax and building wealth. They arent just personal milestones but important life events and moments that should prompt you to update your financialplans.

You can make tax-free transfers from your Individual Retirement Account (IRA) to support a charity while also benefiting yourself. What Are Qualified Charitable Distributions (QCDs)? For those over 70½, you might already be familiar with Qualified Charitable Distributions (QCDs). Moreover, it simplifies the process of giving.

People usually arrive at this conclusion if they have changed jobs or just want better control over their retirement funds. A 401(k) rollover refers to transferring money from one retirement account, such as an old employer’s 401(k), into a new 401(k) or an Individual Retirement Account (IRA). Why consider a rollover?

Are you thinking about cashing in on your Roth Individual Retirement Account (IRA) early? There are several types of IRAs, such as Traditional, Roth, Simplified Employee Pension (SEP), and Savings Incentive Match Plan for Employees (SIMPLE). First off, let’s clear up some confusion. These withdrawals are taxed as regular income.

Qualified charitable distributions are made directly to the eligible charity from a traditional IRA, inherited IRA, inactive Simplified Employee Pension (SEP) plan and inactive Savings Incentive Match Plan for Employees (SIMPLE) IRAs. 2025 amounts should become available later this year.

Darrow Wealth Management offers asset management and financialplanning services; we do not provide tax advice or tax preparation services. Unrealized gains are not taxed, and you won’t owe taxes when selling assets held in tax advantaged retirementplans or IRAs, though there are tax implications when money is withdrawn.

According to the Federal Reserves 2022 Survey of Consumer Finances , heres how household wealth is distributed on average across all U.S. In contrast, the typical (median) household is far more concentrated in home equity and retirement savings, with limited exposure to stocks or private business ownership.

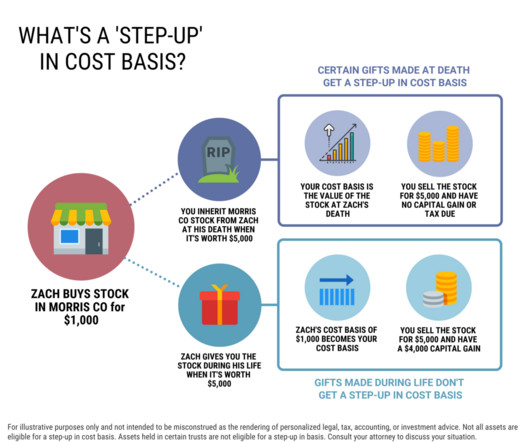

Non-retirement assets like stocks in a brokerage account, inherited home , antiques/art/collectables, or other real estate, are generally eligible for a step-up in cost basis. Retirement accounts and IRAs do not receive a stepped up basis. Inheriting a Trust Fund: Distributions to Beneficiaries Do You Pay Tax on an Inheritance?

Many of us all but ignore our retirement accounts for much of our working livesmost likely only vaguely aware of the portion of our paychecks going into our 401(k)s. If this describes you, its time to give retirement savings more attentionparticularly in the case of IRAs. Which one of these might work best for you?

The post How Do You Turn Retirement Savings into a Reliable Income Strategy? How Do You Turn Retirement Savings into a Reliable Income Strategy? You’ve likely spent years building your retirement nest egg—saving diligently, investing wisely, and contributing to retirement accounts along the way.

Good financialplanning is all about asset and liability matching across time. A financialplan with an asset liability mismatch is likely to fail over time. Nothing will nuke your financialplan like high credit card debts and other high rate liabilities. Asset and Liability Matching.

Fred Barstein , The Retirement Adviser University, June 9, 2025 6 Min Read Mihajlo Maricic/iStock/Getty Images Plus While the defined contribution market is finally capturing due attention from the financial services industry and mainstream media with $12.5 Convergence of wealth, retirement and benefits at the workplace 3.

One of those items on the estate planning to-do list is making sure your investment accounts and life insurance policies have their beneficiary designations filled out. However, it’s one of the most important aspects of estate planning. If married, your spouse will usually inherit by default, then your children afterwards.

Receive income : During the term of the trust, youor other designated income beneficiariesmay receive an annual distribution from the trust. For example, a $1 million CRAT with a 5% payout rate would distribute $50,000 annually for the duration of the trust. If it declines, so does your distribution.

The post Strategic RetirementPlanning Guide for Single Women: Expert Financial Advice appeared first on Yardley Wealth Management, LLC. Without a partner to rely on for financial support, single women must take proactive steps to ensure a secure and comfortable retirement.

We sometimes see this when families are in their peak income-earning years with retirement on the horizon. However, either the donor or the donor’s representative retains advisory privileges with respect to the distribution of funds and the investment of assets in the account.

The second amendment to the revocable trust agreement directed the following distributions: • 2 million dollars to the trustee of the MCC Trust, to be held for Maria’s benefit. The MCC Trust agreement included terms about the distribution of trust assets: 3.2. Administration of Trust Estate for Beneficiary.

The transition from employment to retirement can be complex. Retirement-related behavioral and financial changes raise many tax planning questions and opportunities. Social Security was designed to supplement personal savings and income from various retirement savings vehicles. Suddenly, that will slow or stop.

Wondering how to prepare for retirement the smart way? Whether your dream is to travel the world, spend time with grandkids, or simply enjoy a slower pace, retirement is one of lifes biggest transitionsand it deserves a solid plan. Financial freedom in retirement doesnt happen by accident. Youre not alone.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content