This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

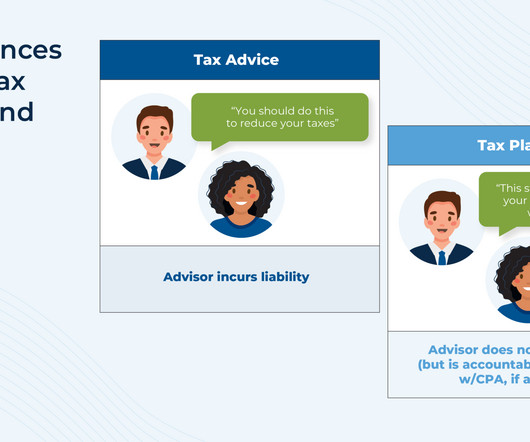

In recent years, financial advisors have increasingly embraced taxplanning as a core element of delivering value to clients. Despite this growing interest in tax conversations, most advisors are still quick to distinguish their services as "taxplanning", not "tax advice" – a distinction largely driven by liability concerns.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. GET STARTED 1. For those over 50, the limit is $8,000.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations. This guide consolidates what we’ve learned to help you refine, update, or pressure-test your current retirement and estate strategy with confidence.

Life transitions such as marriage, divorce, the birth of a child or grandchild, career changes, retirement, an inheritance, or the purchase or sale of a home can all influence your broader financial picture. These events may affect your investment approach, taxplanning strategies, insurance needs, and estate planning documents.

For audit-ready best practices, consider consulting with a tax professional in real-time, especially for mixed business and personal expenses. These variables can significantly impact the final deduction amount, necessitating strategic planning to optimize this benefit.

Employee Stock Ownership Plans (ESOPs) An ESOP allows owners to gradually sell their shares to employees through a qualified retirementplan. This can be an effective way to preserve company culture, reward loyal staff, and capitalize on significant tax benefits.

In this article, well examine the most effective end-of-year tax strategies to help maximize your deductions and reduce your taxable income. These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. Available to taxpayers aged 70.5

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k).

There are so many products out there – 401(k)s, mutual funds, Individual Retirement Accounts (IRAs), Exchange-Traded Funds (ETFs), bonds, Real Estate Investment Trusts (REITs), etc. Each comes with its own rules, returns, fees, lock-ins, and tax treatments. Today, you can work with fee-only advisors who charge by the hour or per plan.

Additionally, you must maintain appropriate business insurance and consult with wealth managers and legal experts to ensure ongoing protection. So, take calculated risks, research well, and consult experts as and when needed. So, consult with a qualified tax professional before executing it.

Donor-advised funds (DAFs) have emerged as powerful tools that deliver this exact combination, providing immediate tax advantages while offering flexibility to recommend grants to qualified organizations over time. This article should not be considered tax or legal advice and is provided for informational purposes only.

Unexpected events can derail your progress toward your goals and even your financial security if you don’t have a plan for managing them. Financial planning should ideally involve every area of your financial life because they are all interrelated. Taxplanning. Taxplanning is crucial. Plan for retirement.

This article will explore how to navigate complex tax situations arising from multiple income sources, examining various income types, reporting requirements, self-employment obligations, and strategic approaches to record-keeping and taxplanning that can help protect your financial interests.

Whether it’s investment planning, retirementplanning, tax strategy, estate management, insurance planning, or holistic money management, the CFP designation proves that you can deliver advice that is both competent and client-centric.

These include student loan interest, educator expenses, and certain contributions to retirement accounts. Why do tax credits exist? Whether it is promoting education, incentivizing retirement savings, or supporting parents and low-income workers, these credits serve as powerful policy tools.

Running focused social media campaigns that highlight their services and share their skills in areas like taxplanning or retirementplanning. This helps readers know what to do next, like visiting your website, setting up a consultation, or downloading something useful. Use clear calls to action.

A good rule of thumb is to set aside at least 30% of every payment you receive to cover your estimated tax obligationshowever, this percentage may need to be adjusted based on your individual tax bracket. On the whole, its advisable to consult a tax adviso r to develop a dependable taxplan.

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. Start planning early. And the best way to do that?

If the total positive UBTI across all applicable investments in a retirement account equals $1,000 or more, the tax-exempt entity is required to file Form 990-T and pay tax on the UBTI. This is an important consideration for high-income individuals using tax-advantaged retirement accounts for alternative investments.

This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on taxplanning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments. Different types of income maintain their distinct tax treatment as they pass through to a partner.

You should consider using tax preparation software or consulting with a tax professional. Deducting business vehicles, meals, travel, and entertainment: Business deductions are a common source of tax errors and abuse, as they often involve a mix of personal and business expenses.

Whether clients support the policies with cash gifts or split-dollar, the discussion of options will necessarily involve a combination of insurance planning, taxplanning, income and gift tax-oriented wealth transfer planning and investment planning.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. One of the Roth IRA’s most compelling features?

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

State-level variations: State tax laws can significantly impact the effectiveness of tax-loss harvesting strategies. As a result, its crucial to consult with a qualified tax advisor who understands your states tax laws. When should you avoid tax-loss harvesting? This article is a product of Harness Tax LLC.

The key benefits Reduced tax liability: So long as youre paying reasonable wages to your child, you can lower overall tax liability. For instance, children can earn a gross income up to $14,000 (2024) tax-free under the standard deduction, shifting income to a lower tax bracket. Do You Need an LLC to Claim Tax Write-Offs?

Cash balance plans have quickly become one of the most popular options in the defined benefit spacenow representing over 50% of all such plans. Their appeal lies in their flexibility, tax advantages, and ability to help small business owners save more for retirement while reducing taxable income.

Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Many people end up paying taxes twice. In 2024 and 2025, the highest marginal tax rate is 37%. Yes and no.

Good CTA Examples (And a Few to Avoid) Great CTAs: “Download Our RetirementPlanning Guide” “Join Our Webinar on Investment Strategies” “Get Your Personalized Financial Plan” “Subscribe to Our Weekly Financial Tips” Each of these is clear, benefit-driven, and actionable.

However, when exercised, holders must calculate the spread between strike price and fair market value for Alternative Minimum Tax purposes. Documentation significantly impacts ISO taxplanning. Companies provide Tax Form 3921 in January to detail the information needed for accurate calculations.

Add keywords your audience might use, like Financial Advisor | RetirementPlanning or “Wealth Management | TaxPlanning.” Examples of Winning Bios Retirement Ready? I help teachers plan their future Book a call Gen Z Money Coach Helping students crush debt & grow wealth.

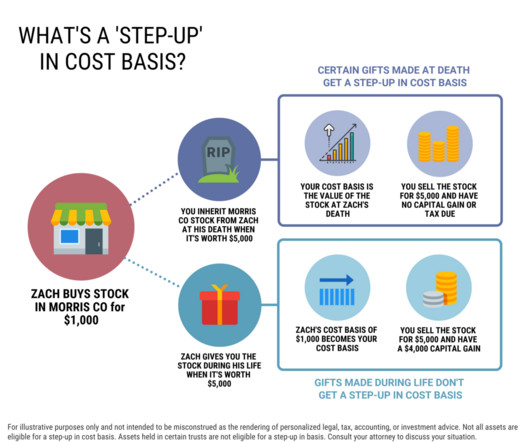

Example of a step-up in tax basis on stocks inherited at death What types of assets are eligible for a step-up? Non-retirement assets like stocks in a brokerage account, inherited home , antiques/art/collectables, or other real estate, are generally eligible for a step-up in cost basis. The post What is a Stepped Up Basis?

Tax Complexity: Many alternative investments issue Schedule K-1s instead of Form 1099, meaning investors may face additional tax reporting requirements, potential delays in tax filings, and increased preparation costs. Can I hold alternative investments in my retirement accounts?

Home office space deductions Business equipment deductions Travel expense deductions Vehicle mileage deductions Business meal deductions License fee deductions Health insurance deductions Retirement contribution deductions How do I claim home office tax deductions? How Harness can help FAQs Am I eligible for home office tax deductions?

Seek Wise Counsel: Consult knowledgeable advisors who understand both estate planning and Christian values. Estate planning underlines the significance of responsible stewardship the management of resources in a way that respects God’s desires and values. Ethical Investments: Align investments with Christian values.

In this guide, we’ll explore the key tax changes in effect for 2025, how theyll influence your filing status, retirement savings, investment, and estate planningand offer strategic advice to help high-income and high-net-worth individuals prepare more effectively for upcoming coming tax changes.

Unless Congress intervenes, the TCJAs sunset will usher in a swathe of tax increases in 2026, with analysts estimating that over $4 trillion worth of tax hikes could take effect. Estate and gift taxplanning Maximize gift tax exemption: Encourage clients to use the currently higher $13.61 million (single) / $27.22

Important Consideration: Due to the complexity of the rules and nuances, it is crucial to discuss your specific situation with a financial advisor, estate planning attorney, and tax professional. Roth conversions reduce asset balances subject to mandatory withdrawals and if holding periods are met, money can be taken out tax free.

The transition from employment to retirement can be complex. Retirement-related behavioral and financial changes raise many taxplanning questions and opportunities. Provisional income is your adjusted gross income PLUS tax-free interest PLUS 50% of gross Social Security benefits. Suddenly, that will slow or stop.

I am a CFA® charterholder and financial advisor marketing consultant. Andy Panko started a taxes in retirement Facebook group. Just say, “ I was researching this company and I know that taxes have just onge up in the local area. I just wanted to come in and do a seminar about how to do taxplanning in XYZ County.

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

Investment and retirement accounts : Stocks, bonds, mutual funds, IRAs, 401(k)s, pension plans. Beneficiary-designated assets like life insurance or retirement accounts may bypass your will entirely. Strategic taxplanning is essential for preserving wealth across generations. Start with your assets.

Develop a risk management plan to implement strategies that minimize or eliminate risks, and protect your business with appropriate insurance coverage, such as liability, property and business interruption insurance. Get Help with TaxPlanningTaxplanning is a critical component of financial management.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content