This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If youre looking for a fee-onlyfinancial advisor or wealth manager, its probably because you know fee-only advisors don’t sell products. Finding the right financial advisor is so important. Here are some ways to find the best fee-onlyfinancial advisor to suit your needs.

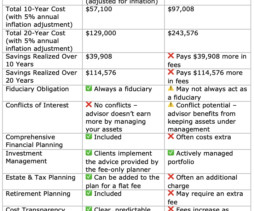

The two most common pricing models are fee-onlyfinancial planners (flat-fee or fixed-fee advisors) and AUM-based financial advisors (who charge a percentage of assets under management). While AUM advisors may seem appealing, they often come with high lifetime fees and potential conflicts of interest.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent survey sponsored by CFP Board demonstrates the upsides of a career in financialplanning, from a median salary of nearly $200,000 to flexible work schedules and a strong sense of purpose among advisors.

Traditionally, investment planning has been at the forefront of how financial advisors add value for their clients. But, with the rise of index funds and the commoditization of investment advice, generating sufficient investment ‘alpha’ to justify a fee has become more challenging for advisors.

Traditionally, investment planning has been at the forefront of how financial advisors add value for their clients. But, with the rise of index funds and the commoditization of investment advice, generating sufficient investment ‘alpha’ to justify a fee has become more challenging for advisors.

The post What’s a Fiduciary & Fee-Only Advisor? What’s a Fiduciary & Fee-Only Advisor? A Guide for FinancialPlanning When it comes to managing your finances, it’s crucial to work with a professional who puts your interests first. What is a Fee-Only Advisor?

.” Only 4 percent of Certified Financial Planner™ professionals identify as Asian American or Pacific Islander (AAPI), though they make up 6.2 1,2 Despite the small numbers, AAPI professionals remain the largest ethnic minority within the financialplanning profession. percent of the American population.

I can tell you that when I was editor of FinancialPlanning magazine, I discovered that there is a whole public relations ecosystem churning out favorable press releases and miscellaneous announcements that they would position as ‘news.’ Executive hires are very important for you to be aware of.

Fee-Onlyfinancial advisors and firms receive no sales-related compensation or incentives. They are compensated only by the fee the client pays. This can include mutual funds, insurance policies, annuities, and other financial products. Fee-based advisors are where it can get complicated.

During recent conversations, I’ve come across several people unfamiliar with the concept of fee-onlyfinancialplanning, let alone considering it as a feasible choice. To shed light on this, I want to articulate the distinctive approach we use at MainStreet FinancialPlanning.

An RIA firm’s financial advisors must follow the fiduciary standard which is believed to be the highest standard of care in the industry. Fee-only advisor – This is an advisor that does not charge commissions and hence is believed to be more aligned with the client’s best interests.

They can offer flexible engagement options Financial advisors are not just for the super-rich. Today, you can choose from different types of financial advisors , such as fee-only, commission-based, hourly, AUM-based, or whatever works for your financial situation. You also do not need to commit forever.

How Conflicts of Interest Shape Financial Advice: A Conversation with Mike Garry and Amy Patterson Conflicts of interest in financial advice can greatly impact the recommendations that clients receive, especially from fee-only advisors. Today, many advisors have moved to a fee-only model.

As the move to transparency in financialplanning takes hold, regulations are changing in Colorado and other states. Here’s the triumph of virtue that financialplanning transparency will (FINALLY) bring to planners across the country and the benefits to clients that come along with it. What should financial advisors do?

What does it mean to be a Fee-Onlyfinancial advisor ? Fee-Onlyfinancial advisors and firms receive no sales-related compensation or incentives. They are compensated only by the fee the client pays. This can include mutual funds, insurance policies, annuities, and other financial products.

Below are the different types of financial advisors you can choose from based on their fee model: 1. Fee-onlyfinancial advisors Average cost: $200 to $400 an hour/ $1,000 to $3,000 per plan/ 1.18% to 0.59% of AUM Fee-onlyfinancial advisors are professionals who do not receive commissions from selling financial products.

A financial advisor is a certified financial planner who is licensed and regulated to take mandate decisions on multiple aspects of financialplanning. They may charge for their services either on a commission basis or hourly rates. First of all, the financial advisor has the expertise to do your research.

Your teen will receive their own debit card with no account fees, account minimum or trading commissions. Financial Literacy Books for Parents. You can read about more of my favorite resources and advice in my “How to Improve Your Financial Literacy” post. About Your Richest Life.

The primary fee structures are: Fee-only : Advisors only receive payment from their clients for the services they provide, not receiving any commissions or other incentives from product providers. Fee-based : This structure is a blend of fees and commissions.

Financial advisors provide financialplanning or investment guidance to clients. Financial advisors may work for themselves, with small firms or large organizations. They generally provide advice to help their clients pursue their financial goals. . IARs can also charge different types of fees.

There are two types of Financial Advisors in India – Fee-Only Advisors and CommissionOnly Advisors. Fee-only advisors need to be registered with SEBI certified financial advisors (Securities and Exchange Board of India) as an RIA (Registered Investment Advisor).

My client’s estate planning attorney said they should hire a fee-only advisor to manage their assets, and then they asked me if I charge fees or commissions. As a fiduciary, I charge 1% of your assets, and do not accept commissions.” I’m a Social Security expert.

If you are already working with a financial advisor, assessing their track record can provide valuable insights. If the financial advisor consistently delivers impressive returns, aids in achieving primary financial goals, or offers extensive financialplanning services, the 1% fee may be well-justified.

If you’re as old as Methuselah, like I am, you might remember a pivotal moment in the evolution of the planning profession, when Forbes magazine noticed that brokers, life insurance and tax shelter salespeople were starting to call themselves ‘financial planners.’ Pandemonium!

You never hear anyone talk (or write) about this, but it’s really stunning how often the financialplanning profession has been, and is, ahead of the curve in the evolution of our social environment. The whole idea of turning financial customers into clients was invented in the fee-onlyfinancialplanning world.

FINANCIALPLANNING, INVESTMENTS. 03% for IXUS and they can be bought commission-free and the spreads on each average only $.01. Please contact us if you’d like to discuss your financialplan. Our law firm is Yardley Estate Planning, LLC and is in the same place. The expense ratios are.09%

Providing financialplans vs. canned financialplans with a sales agenda. Fee-only vs. fee-based. But… Fee for service (and onlyfee for service) is a haven where the sales agenda mimicry cannot follow. .” Fiduciary vs. ‘best interest.’.

The obvious next priority to put on the regulatory watch list is sales commissions. I think it’s self-evident that any product that has to pay people to recommend it is probably not competitive on its own merits.

Then came Reg BI, in 2019, where the Commission decided that adopting a separate rule restricting these terms was ‘unnecessary.’. 202(a)(11)(c) of the Advisers Act,” the petition says, “the Commission can increase investor protection by (re-)asserting a distinction between product sales and stand-alone investment advice.”.

His smart career decisions after university allowed him to avoid the being tortured and exploited in a wirehouse, bank, and insurance company financial advisor program. Instead, he got his first job at a feeonly RIA firm instead which worked out brilliantly for him! From here you can move into a more senior planning role.

If their sole method of compensation is a product, and/or they are taking commissions, then in reality it is less likely they are embracing all the values that the standard requires. Commissions are opaque. But if they are acting in the capacity of a broker or agent then they are not bound to follow the fiduciary standard.

Most often, until someone has been a victim of financial fraud, they fail to recognize the growing intensity of these crimes. According to the Federal Trade Commission (FTC), in 2021, American consumers lost over $5.8 You can check the company’s financial statement on the Securities Exchange Commission (SEC) EDGAR filing platform.

Additionally, you would not be so overwhelmed or stressed about planning for multiple goals and can instead concentrate on the pressing issues ahead of you. People who start retirement planning and other financialplanning at a later stage in life often struggle with multiple financial responsibilities together.

Additionally, you would not be so overwhelmed or stressed about planning for multiple goals and can instead concentrate on the pressing issues ahead of you. People who start retirement planning and other financialplanning at a later stage in life often struggle with multiple financial responsibilities together.

Rostad is currently focused on what he sees as our best chance for meaningful reform: getting the Commission to revise the Form CRS disclosure so that it provides a clearer explanation of the different business models of broker-dealers/wirehouses, on the one hand, and fiduciary RIAs registered with the SEC on the other.

An hourly financial advisor is someone who provides financial advisor for a set hourly rate. These services often include recommendations on investments, financialplanning, retirement, Social Security, Medicare, tax planning, and other wealth-related topics. Hourly financial advisors are not common.

Financialplanning services can assist with developing a comprehensive estate plan. A good financial advisor can provide investment advice and help navigate the various types of financial advisors, such as registered investment advisors and fee-only advisors.

Financial advisors have many options at their hands to solve it, from financialplanning and investment management services to fixed products such as annuities. With annuities now being able to be offered in 401k plans, the playing field has changed. Are commissions bad? Are commissions bad?

The problem for them is that they went into this deal thinking they were gonna hurt and ET 788%, and they actually end up earning 3 E45%, and that… Is that now their whole financialplans… Erectus Earl. Yeah, you have a short fall. SARA GRILLO: Other than five and a half, six. Excuse exactly. Does that make sense?

We’ll discuss these questions: The CFP Board has specifically stated that it wants the CFP® mark to be a requirement for anyone who practices financialplanning. The debaters are: Robert Wright, CFP®, a financial consultant with Advocacy Wealth Management. What is your opinion? Robert will be on the “for” team.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content