This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

How advisory firms charge for financialadvice has long been a central question in the profession. Now, as financialadvicers expand their services beyond traditional planning into more holistic, personalized advice, the very definition of financialadvice continues to evolve.

Just a few decades ago, giving financialadvice was largely a manual process – printing lengthy financialplans, processing physical checks, and managing paper files. Many client concerns are deeply personal, requiring empathy, trust, and a nuanced understanding of complex emotional and financial situations.

Financialadvicers often market their comprehensive financial services as a way to differentiate themselves from other advisory firms and to stand out in the broader landscape of financialadvice. While advisors may make educated guesses about client preferences, this approach has its limits.

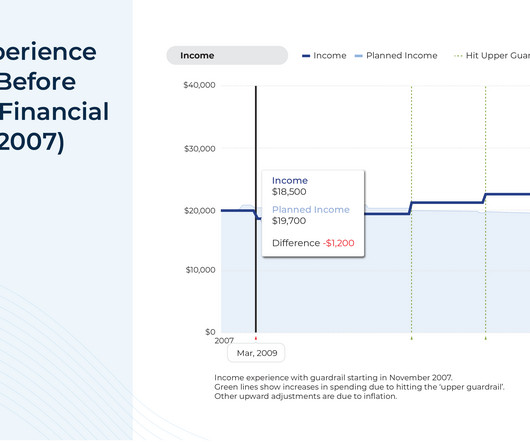

is perhaps the most fundamental question a client brings to their advisor. Advisors want to help clients set a secure, reliable retirement plan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree. "How much can I spend in retirement?"

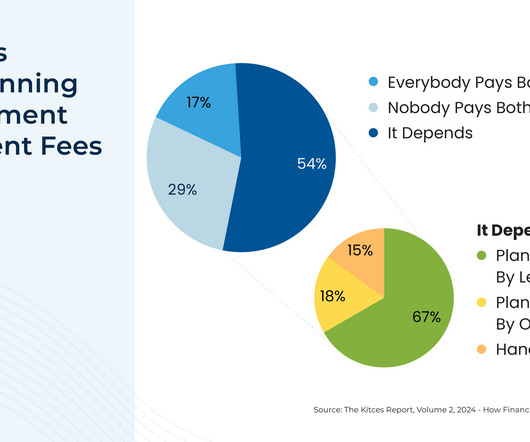

How much to charge for financialadvice is rarely a decision made lightly. Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning. Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning.

In these moments, the conversations that advisors have with their clients play a crucial role in helping clients maintain perspective, avoid emotional decisions, and stay committed to their long-term financialplans. Using mirroring language (e.g., Read More.

I help clients in retirement by doing X, Y, and Z."). However, not all prospects have immediate financial concerns. While these individuals may genuinely be interested in financialadvice, they might also feel ambivalent about the timing, relevance, or ultimate value of working with an advisor. Read More.

The possibilities at the intersection of AI and financialadvice are exciting – faster processes, better connections, less time on ‘busy work’ – but also come with uncertainty about the future of the field. What might the field of financialadvice even look like in 10 years? Read More.

Which could prove to be a boon for the financialadvice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?). Read More.

Fran is the CEO of Toler Financial Group, an RIA based in Silver Spring, Maryland, that oversees nearly $200 million in assets under management for 280 client households. My guest on today's podcast is Fran Toler.

New financial advisors often start with below-market fees – sometimes to build confidence that prospects will actually pay, other times to attract clients quickly and establish a base. And while new clients often come in at higher fees, early clients may still be paying well below the firm's current rates.

In fact, they may be the missing piece in your clients’ portfolios—and AssetMark is betting big on that future. Q&A: What Was Behind Schechter’s Decision to Sell to Arax? June 27, 2025 Private markets are no longer just for the ultra-wealthy.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that a recent survey found that long-feared fee compression in the financialadvice industry has yet to come to pass, though some advisors continue to see potential for small reductions in asset-based fees in the future.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with a recent survey indicating that a majority of advisors are viewing new client acquisition as their primary challenge in the current competitive environment for financialadvice (followed by compliance and technology management) and suggests (..)

As the financialadvice profession has matured, behavioral finance has become an increasingly important element of modern advice. From the prospect’s point of view, it’s easier to not hire a financial advisor than it is to hire one (at least in the short term). Read More.

Seth is the founder of Heartwood FinancialPlanning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households. My guest on today's podcast is Seth Scott.

For instance, the financialadvice industry has seen many changes to regulations (for both advisors and their clients), advisor business models, and the advisor technology landscape. The changing patterns in how financialadvice is delivered can be compared to the similar trends seen in the evolution of medicine.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that Republicans in the House of Representatives this week released their long-awaited tax plan to address the impending sunset of many measures in the 2017 Tax Cuts and Jobs Act.

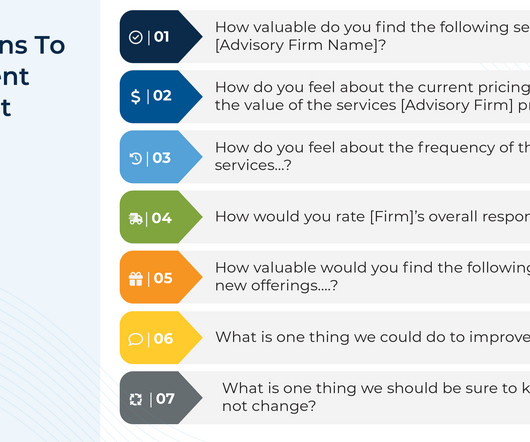

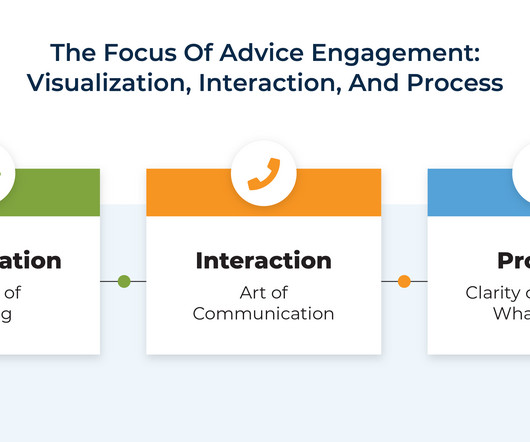

Financialplanning is inherently complex, especially when it comes to data gathering, analysis, and crafting well-reasoned recommendations. But delivering those recommendations in a way that clients can understand and act on is a separate skill. One way to simplify delivery is to build meetings around a single core takeaway.

Podcasts Daniel Crosby talks with Michael Kitces about automation and the future of financialadvice. kitces.com) Brendan Frazier talks with Samantha Lamas and Danielle Labotka about why clients hire and fire their financial advisers. wsj.com) Advisers How to speak to clients in a way that they understand.

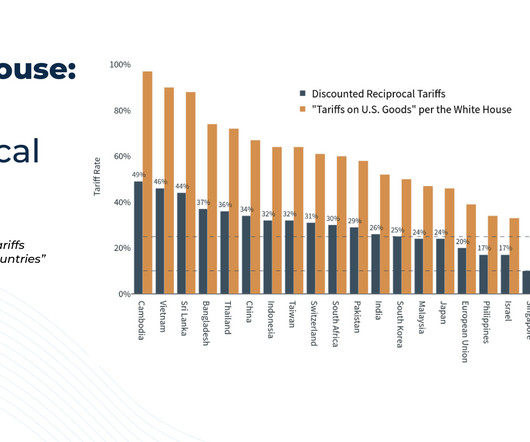

2025 has had a tumultuous start for most advisory firms, as tariffs-driven market volatility has increased client anxiety and the amount of required hand-holding, forcing advisory firms to manage their own expenses a bit more closely in the face of greater revenue uncertainty.

Which suggests that, amidst ongoing debate over fiduciary-related regulations, an advisor's status as a fiduciary could both lead to greater client trust (both in their individual advisor relationship and perhaps in the financialadvice industry as a whole) and, ultimately, higher client retention rates.

Financial advisors have a fiduciary obligation to act in their clients' best interests, and at the same time are prohibited by state and SEC rules from making misleading statements or omissions about their advisory business.

downtownjoshbrown.com) How indexing has made for a better financialadvice industry. morningstar.com) The biz Creative Planning was able to retain some 60% of the United Capital assets. riabiz.com) XY Planning Network is launching a new in-house RIA, XYPN Sapphire. citywire.com) A lot of RIAs are in that in-between stage.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the "Social Security Fairness Act" was signed into law this week, eliminating the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO) provisions, which previously reduced the Social Security benefits (..)

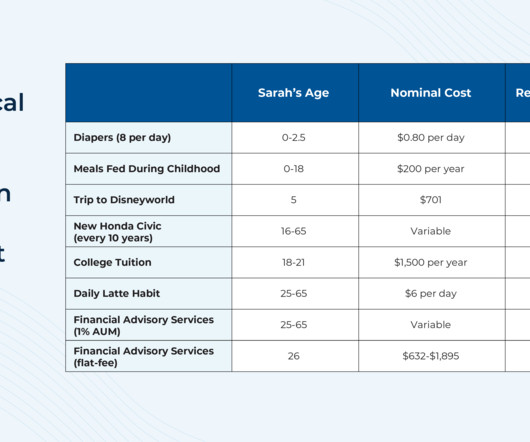

While the financialadvice industry has transformed in many ways over the past several decades, one aspect that has remained relatively constant is the use of the Assets Under Management (AUM) fee model as a common way for many advisors to get paid. So too does the impact of the infamous daily latte.

dollars) in assets under management for 2,400 client households. Cameron is the CEO of PWL Capital, a wealth management firm based in Ottawa, Canada, that oversees just over $5 billion Canadian dollars (or approximately $3.5B million U.S.

Working as a financial advisor can be both financially rewarding and emotionally satisfying. By helping clients develop financial goals, creating a financialplan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives.

While some of these programs still exist, the role of an associate advisor has evolved alongside the broader financialplanning profession. Even for advisors with a CFP certification or other credentials, honing these skills and the confidence to use them in real-time client interactions requires additional practice.

The requirements to run a successful, growing advisory firm are often less about doing the technical work with clients and more about marketing value to get prospects in the door in the first place. comprehensive, planning-centric, fee-based advisors) versus 'bad guy' (e.g.,

Podcasts Michael Kitces talks with Nick Rodkin, managing partner of Stoic Financial, about working with client couples. kitces.com) Matt Zeigler talks with Danika Waddell, founder of Xena FinancialPlanning. epsilontheory.com) Aging How financial literacy declines with age. alphaarchitect.com)

At Wealth Management EDGE , I had the privilege of moderating a panel— “Work Smarter, Not Harder: AI’s Role in Operational Excellence” —where we talked about how artificial intelligence is already automating advisor workflows, transforming client meetings into structured insights, and reshaping the nature of operational roles within firms.

Working as a financial advisor can be both financially rewarding and emotionally satisfying. By helping clients develop financial goals, creating a financialplan, and supporting the implementation and monitoring of the plan, advisors help clients live their best lives.

One of the main goals of financial advisors who market themselves is to build a foundation of trust with their prospective clients so that they feel comfortable in discussing often-sensitive financial topics and ultimately acting on the advisor's recommendations.

As financialplanning has evolved over the years, better tools have become available to help advisors maximize their impact with more clients by increasing their efficiency. robo-advisors) might someday replace human advisors, there are still many elements of financialplanning that benefit from engagement with a human advisor.

In the competitive market for financialadvice, advisory firms often seek to find ways to differentiate themselves from one another. However, advisers may also realize the operational cost benefits of launching a private fund since they would not need to execute many individual trades for clients through separate accounts.

When it comes to politically charged discussions, financial advisors generally try to stay neutral and focus on providing clients with objective financialadvice. This can make it increasingly difficult for the advisor to work with these clients.

In the modern era of financialadvice, the advicer/client relationship is tightly centered on trust. Then, because the client isn't "bought in" to the recommendations, they simply don't act on what the advisor recommends.

It's not news that financialadvice will increasingly be grounded in psychology and therapy—but how an advisor builds a business around those client demands is still evolving, according to speakers at the Future Proof wealth festival.

paulkrugman.substack.com) Jess Bost and Mark Newfield talk with Ashley Quamme about her journey to financialadvice. podcasts.apple.com) Charles Schwab Charles Schwab ($SCHW) is launching a new program aimed at helping financial advisors go independent. citywire.com) How to learn about financialplanning on the cheap.

The traditional way that most financialplanning has been offered was for an advisor to create "The Plan": a comprehensive document outlining a client'sfinancial strategy that was delivered either on a one-time basis or updated annually.

There are many financial advisors who take issue with the financialadvice offered by popular personal finance personalities such as Dave Ramsey. Though many potentially valid criticisms of this process tend to concern technical details (e.g., Read More.

Podcasts Christine Benz and Amy Arnott talk with Preston Cherry, author of a new book "Wealth in the Key of Life: Finding Your Financial Harmony." morningstar.com) Carl Richards and Michael Kitces on whether a client should take time before coming on as a client. How to do better for clients.

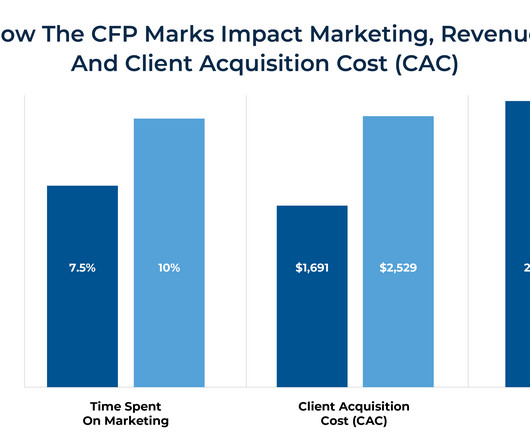

According to the 2022 Kitces Research study, “How Financial Planners Actually Market Their Services”, advisors without the CFP marks typically spend more of their time on marketing activities relative to CFP practitioners (allowing them to spend more time on higher-value tasks).

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content