This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

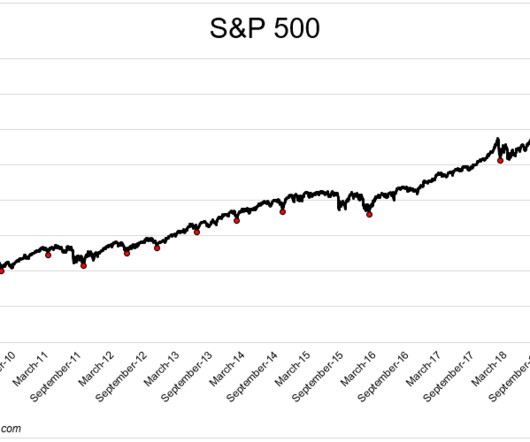

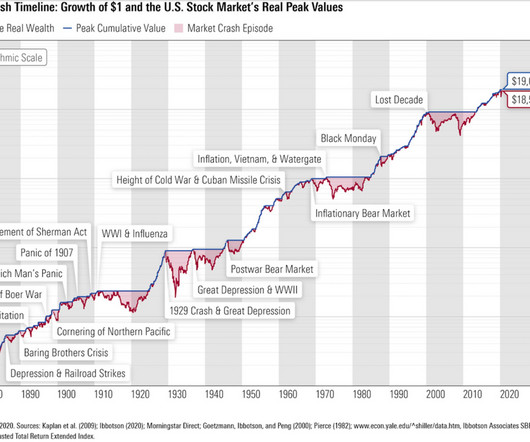

Chart above is from March 2009, but that’s cheating) Compare this to the average 15-year return periods over the past century, which generated ~8.7%. In October 2009, I called the move off the lows The Most Hated Rally in Wall Street History. Financial Repression was the rallying cry for underperforming managers.

This is Masters in business with Barry Ritholtz on Bloomberg Radio 00:00:17 [Speaker Changed] This week on the podcast, Jeff Becker, chairman and CEO of Jenison Associates, they’re part of the PG Im family of AssetManagements. Jenison manages over $200 billion in assets. Each of these assetmanagers had A-A-C-E-O.

At Validea, we’ve built our version of the All Weather Portfolio based on the core principles of asset class diversification that underpin Dalio’s original concept. All Weather Portfolio: Asset Class Behavior Across Economic Regimes Asset Class Performs Well In Why It’s Included U.S. 2008 -0.4% -21.0%

Related: Zephyrs Adjusted for Risk: The Art of RiskManagement in Volatile Markets Is Diversification Overrated? As you can see in the Zephyr graph, correlations between different asset classes and the S&P 500 index typically increase during periods of inflation.

In a bull market, protecting one's downside gets punished, and after being burned enough times, people tend to lighten up on riskmanagement, or abandon it altogether. In a bull market the more risk you take, the more you're rewarded, and the more you're rewarded, the more you forget about risk.

We are currently experiencing one of the most volatile times in decades, on top of the start of the pandemic and the 2008-2009 recession. That’s why, when facing market volatility, stewards of long-term assets held at all types of nonprofit institutions recognize the importance of a well-thought-out investment process. .

And before that, Morgan Stanley, doing technology and operations planning for the wealth and assetmanagement group. What percentage of the assets are in ETFs relative to mutual funds? So fast forward to where we are today, we have over $40 billion in assets under management. BERRUGA: You know, great question.

Northern Arc Capital IPO – About the Company The company was founded in 2009. Fund Management includes managing debt funds and providing portfolio management services. It uses data-driven riskmanagement and credit underwriting processes. Keep reading to learn about the company. crores in FY24, and Rs.

One of the few movies which portray the 2008 financial market crisis in the most accurate way possible, this thrilling movie’s inciting incident begins when a risk-management division head is laid off due to the company’s downsizing. Moreover, be aware of assets sold at a heavily discounted price (also known as a fire sale.)

As of June 30, 2024, their assets under management were Rs. in 2009 to 12.3% The Capital to RiskAssets Ratio (CRAR) stood at 21.28% in FY24 compared to 22.97% in FY23, which is higher than the regulatory requirement of 15%. Non Performing Assets in FY24 stood at 0.10% compared to 0.08% in FY23.

So, the Portfolio Solutions Group advises mainly institutional clients on all kinds of challenges that they have and thinking about the expected returns, portfolio construction, riskmanagement, et cetera. You mentioned in the beginning of the book lower asset yields and richer asset prices have pulled forward future returns.

So if you start with the S&P 500 or in this case stocks and bonds, you only have two asset classes, right. So the proper benchmark for those pools has to look a little bit like the underlying assets they’re investing in. If you look at the types of assets that Yale invests in, you can create a benchmark for each pool.

We view sovereign bonds as an asset class with the potential to achieve progress on the United Nations Sustainable Development Goals (U.N. Investors across the globe increasingly seek to incorporate ESG research into investment decisions across asset classes to align their investment outcomes with their sustainability goals.

We view sovereign bonds as an asset class with the potential to achieve progress on the United Nations Sustainable Development Goals (U.N. Investors across the globe increasingly seek to incorporate ESG research into investment decisions across asset classes to align their investment outcomes with their sustainability goals.

We view sovereign bonds as an asset class with the potential to achieve progress on the United Nations Sustainable Development Goals (U.N. Investors across the globe increasingly seek to incorporate ESG research into investment decisions across asset classes to align their investment outcomes with their sustainability goals.

We view sovereign bonds as an asset class with the potential to achieve progress on the United Nations Sustainable Development Goals (U.N. Investors across the globe increasingly seek to incorporate ESG research into investment decisions across asset classes to align their investment outcomes with their sustainability goals.

And it restarted in, I wanna say March of 2009, but like onlya little bit. It was derivatives math, it was like working with the traders on like riskmanagement. And if you’re thinking about your portfolio systemically, like that creates different incentives for you and for your portfolio company’s managers.

He is the managing director of Vanguard’s Financial Advisor Services Division, where he began back in 2002. That group provides investment services, education and research to more than a thousand financial advisory firms, representing more than $3 trillion in assets. They have a riskmanagement technology. RAMPULLA: Yeah.

The transcript from this week’s, MiB: Ken Kencel, Churchill AssetManagement , is below. BARRY RITHOLTZ, HOST, MASTERS IN BUSINESS: This week on the podcast, I have an extra special guest, Ken Kencel of Churchill AssetManagement, CEO, Founder, President. This is really a fascinating story. It’s fantastic.

And that, quite frankly, was the beginning of the of the asset class. And emerging market is not this homogeneous asset class. And you can see, you know, assets have gone. And if you look on your Bloomberg screen today, on that day, the asset went from 6 cents to 12 cents — RITHOLTZ: Wow. KOENIGSBERGER: Yeah.

I wanna say it’s about $179 billion in client assets. You’ve probably heard some aspects of this from the various interviews I’ve done with Howard Marks talking about the distressed asset fund they set up in 2007. That had mismatched assets. It’s not an asset that other creditors can go after.

I want to get into that before we start talking about assetmanagement. And the third, the one that nobody talks about is riskmanagement. Riskmanagement. So those two things, longevity, a little bit of excess return and, and riskmanagement would be the key. What is that?

The DJIA closed 1999 at 11,497 and 2009 at 10,428. At the GFC bottom, March 9, 2009, the Dow traded at 6,547. who became a professor at the University of Michigan before setting up his own assetmanagement firm. High on that success, as of September 2010, Hussman managed $6.7 So, he missed it by a mile. billion.

No income, no job, no assets were exactly ninja, Sean Dobson : No pulse seems reasonable. We see it as, like I said, about 50 million assets and we’re modeling up the value of every home in the country, every, every week, basically. We’re we’re the quant shop in real estate, in the quant shop in physical assets.

So, it’s 150 million voucher times $20 gives you a $3 billion of vouchers in circulation and this $3 billion of vouchers in circulation were exchangeable for 30 percent of the share capital of all Russian companies, which meant that the market cap of the entire country of Russia, every asset in the country, was $10 billion.

And what I was ended up doing though, was the beginning of what we call asset-backed securities today, pulling together credit card loans for Sears, for MBNA and first USA car loans. And, and commercial paper and asset-backed securities were the first securities that the Fed gave banks permission to underwrite.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content