This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We learned everything, you know, across from accounting to auditing to, to tax and valuation. I ended up in what was called the valuation services group, where we valued real estate and businesses either for transactions or for m and a activity. 00:14:50 [Speaker Changed] Yeah, it was about the middle of 2009.

The funds did well in the Financial Crisis and they did well in 2022 but from 2009 onward, one of his two long standing funds has a negative annual growth rate and the one with a positive growth rate was less than 1/3 of a plain vanilla 60/40 portfolio.

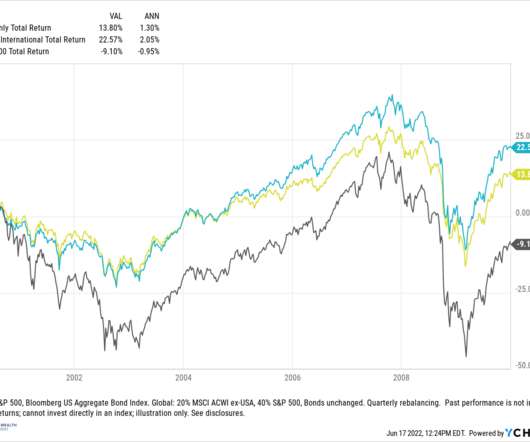

Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% Since trying to time regime changes is very difficult in real time without the benefit of hindsight, there are reasons to consider allocating both U.S. equities to an assetallocation. Valuations. These bouts can be significant.

Smart investors are very careful about market valuations (prices) and investor behaviour. The chart below illustrates that the smart money enters when valuations are low and the majority of the investors aren’t looking at that asset class or security.

1 Also, from fiscal year 2009 until fiscal year 2016, federal agencies cut annual grants to private and public organizations by 3.4% Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains.

I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular. And actually Ben Inker is the head of our assetallocation group. That’s the key to quality investing. 00:18:41 [Speaker Changed] Yep. It was over 50 right? In 2000, right.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. At the same time, the resilience of the U.S.

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Investment Perspectives | Bubbles II. Wed, 04/01/2015 - 16:48.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

Below is the price chart of HUL from Jan 2000 to Jan 2009. If you do not have requisite skill-set or don’t have time, then you should hire an investment adviser who has the expertise to evaluate fair investment valuation and has the experience, temperament and skill-set to alter assetallocation with changing market dynamics and cycles.

is dragged down by 2008-2009 when the index tumbled 37%. We maintain our preference for equities over fixed income and cash in our recommended tactical assetallocation. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. The average of 1.1% How can this be?

This helps to meet your immediate needs and instill discipline in a longterm context, averting excessive spending when valuations are rising. After the 2008-2009 financial crisis, many clients could use loss carry-forwards to reduce taxes against gains taken in subsequent years. By Taylor Graff, CFA, AssetAllocation Analyst.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Valuations are elevated but nowhere near the bubble levels of the late 1990s. The short answer is that it’s very much a mixed picture.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Valuations are elevated but nowhere near the bubble levels of the late 1990s. The short answer is that it’s very much a mixed picture.

Exhibit 1 at right illustrates this pattern; for example, it shows clearly how the relative performance of active managers has slipped during the bull market that started in 2009. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations.

Exhibit 1 at right illustrates this pattern; for example, it shows clearly how the relative performance of active managers has slipped during the bull market that started in 2009. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations.

84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009). Company case studies and practitioner-oriented books provide an outlook on the business case for corporate environmental strategies (Esty, 2009). Deutsche Asset & Wealth Management White Paper. John Wiley and Sons.

84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009). Company case studies and practitioner-oriented books provide an outlook on the business case for corporate environmental strategies (Esty, 2009). Deutsche Asset & Wealth Management White Paper. John Wiley and Sons.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets.

I recall one particularly glaring moment during 2009 when AIG became mostly owned by the US government and failed to meet S&P liquidity requirements, but they just ignored it. It forced me to think in a multi-temporal sense which has completely changed how I think about assetallocation.

I think it’s very hard to say stocks are objectively cheap because all of these valuation metrics have, have become unreliable over the decades as the nature of the stock market has changed. And then on top of that, of course we ran straight into the 2008, 2009 great recession. 00:21:46 Everything was a headache.

While we acknowledge that a V-shaped recovery is probably not in the cards and prior valuation targets no longer appear achievable, we remain constructive on equities for the second half, but not complacent. Remember stock valuations are inversely correlated to inflation and interest rates. So a P/E over 20 is probably too rich.

President Obama’s term, starting in 2009, began when stock market valuations were near the bottom and as is well documented now, the stock market went on to its longest bull market in history. For example, the September 11th terrorist attacks and the 2008 Great Financial Crisis occurred under President G.W. Probably not.

President Obama’s term, starting in 2009, began when stock market valuations were near the bottom and as is well documented now, the stock market went on to its longest bull market in history. For example, the September 11th terrorist attacks and the 2008 Great Financial Crisis occurred under President G.W. Probably not.

It’s just a fascinating conversation about looking at the world from both bottoms up and top-down, as well as thinking about what valuations are like, how likely are macro events, the impact you’re getting not just the return on capital, but as famously said in fixed income, a return of your capital. RITHOLTZ: Really quite fascinating.

The DJIA closed 1999 at 11,497 and 2009 at 10,428. At the GFC bottom, March 9, 2009, the Dow traded at 6,547. 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.” 2020 : “[E]xtreme valuations. So, he missed it by a mile. percent in losses.

And what we figured out in 2009, really when we started buying homes is that we made the bet that it, I mean, it wasn’t a very exotic bet, but we made the bet that the subprime mortgage market wasn’t coming back at all. And so, so starting in 2009, we, we, there was no flip market.

She was CIO at Merrill Lynch Asset Management, and now CIO at both Morgan Stanley Wealth Management and runs their assetallocation models and their outsourced chief investment officer models. 00:20:56 [Speaker Changed] So, so let’s talk a little bit about what goes into managing a hundred plus billion dollars in assets.

The parent company handles all the asset liability management side of things. They give us assetallocations, we go ahead and and and and invest those dollars. 00:32:17 But it’s, it is, it creates a, an interesting opportunity in different asset classes to refine excess returns. 00:59:12 [Speaker Changed] Hmm.

He launched his own firm right into the teeth of the collapse in ’09, which turned out to be quite a fortuitous time to launch an asset management shop. Everybody wants to sell a company when they get a good valuation. RITHOLTZ: So you’re there for 20 years, from 1988 to 2009. They wanted to hear a bear story post 2009.

And so graduating right into 2009, right out of the financial crisis, I said, I don’t think I’m gonna get a job. 00:21:21 [Speaker Changed] So this story came out that, oh, value is defensive because it has this valuation buffer to it 00:21:28 [Speaker Changed] In that one example. And I just caught the bug.

And so I worked a lot on the assetallocation side. Again, as I said, we’ve worked in assetallocation. So you mentioned financial repression, you and the rest of the quants in your core group, including gun lock, decide to stand up your own firm in 2009. And so it’s not just me. Jeffrey Sherman : Both.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content