This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The post Investing for Retirement: Strategies for Long-Term Success appeared first on Yardley Wealth Management, LLC. Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. What lifestyle do you envision?

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

As a result, they may not survive economic downturns as easily, and their stock prices can be a lot more volatile. If you are willing to take a few calculated risks and stay the course, small-cap stocks can be a powerful tool. Your employer contributes extra to your retirement account based on how much you put in.

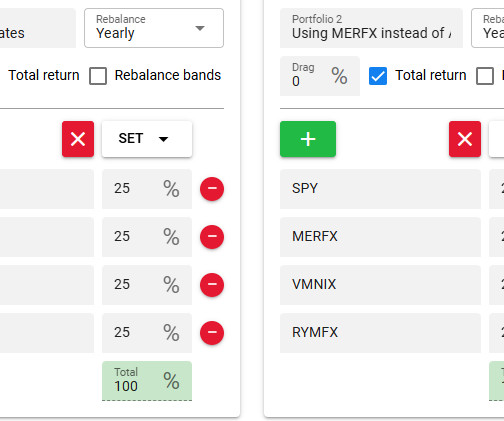

They talked about "four pillars" as being "economic growth (equities), income defensiveness (bonds), absolute return (alpha) and trend following (tail risk)." Research Affiliates (RA) threw its hat in this ring with a long writeup about managed futures. Portfolio 1 is an attempt to be true to the RA paper using AGG for bonds.

How much do I need for retirement?” Your financial needs in retirement can depend on dozens of factors – some known and some unknown. One or two million dollars may seem like a lot of money to have set aside for retirement. A Retirement Reality Check. The concept of retirement continues to evolve with the world around us.

When it comes to their investment portfolios many tend to have a low-risktolerance and with the unsettling economic situation with the ongoing pandemic, the word “risk” has become even more of a fearsome word for clients. This will allow you to get a general sense of where your client’s risktolerance stands.

Which means that longer-term projects, such as creating a succession plan to have in place for the firm when the owner retires, may tend to get put on the back burner.

For people nearing retirement, these challenges can be even more daunting. A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors. Many near-retirees see their highest portfolio values just before retirement.

According to a survey, a significant majority of Americans, approximately 80%, share the common notion that the point of working hard in your adult life is so you can enjoy a nice retirement. After years of dedicated labor and hard work, the prospect of a peaceful retirement appeals to everyone.

Our relationship with money is complicated: Speak to someone at the bottom of the economic ladder and they will tell you in no uncertain terms that a lack of money can lead to misery; but speak to enough millionaires and billionaires and it’s pretty clear that money doesn’t automatically lead to happiness.

In a world where the cost of living is steadily climbing and market uncertainties loom large, the idea of a serene retirement can seem like a distant dream. But let’s face it: the importance of saving for retirement hasn’t waned; if anything, it’s become more crucial. When to start saving for retirement?

Planning for retirement requires a well-thought-out investment strategy. A well-diversified portfolio helps protect against market volatility and minimizes the risk of significant losses. This article explores various strategies for diversifying an investment portfolio to ensure you have enough funds to live comfortably in retirement.

A Roth IRA is a type of individual retirement account (IRA) that allows you to contribute after-tax money and withdraw it tax-free in retirement. Contributions to a traditional IRA may be tax-deductible, but withdrawals in retirement are taxed as ordinary income. However, like any investment, a Roth IRA carries some risk.

Invest in the Stock Market Suggested Allocation: 40% to 50% Risk Level: Varies Investing Goal: Long-term growth The stock market is where most of us save for retirement already, mostly through the use of tax-advantaged retirement plans, like a 401(k), SEP IRA, or Solo 401(k).

Recessions often arrive unexpectedly, even for investors tuned in to the latest economic news. According to the eighth annual Advisor Authority survey, powered by the Nationwide Retirement Institute, over 40% of women believe the U.S. Align client portfolios with their risktolerance and time horizon.

That’s because each investment strategy will apply in different economic and financial environments. Traditional IRA: Best for Dedicated Retirement Planning. Roth IRA: Best for Retirement Planning + Immediate Funds Access. In addition, Roth IRAs are the only retirement plan that’s not subject to RMDs. Ads by Money.

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirement planning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirement planning.

Prices can go from all-time highs to major lows in just a few days, all thanks to global economics, interest rates, and political happenings. Bear markets signify a downward trend in stock prices , often triggered by economic recessions, political uncertainties, or market saturation. When is a good time to invest in the stock market?

As you enter your 50s, the urgency of retirement savings becomes palpable. For those who find themselves behind on their retirement savings, the path ahead may seem daunting. However, despite the challenges, there are strategies to catch up on your retirement savings.

It ensures that your portfolio aligns with your risktolerance and enables you to establish the desired equilibrium between stocks and bonds. This helps you maintain a risk profile that resonates with your financial goals. Major life events often coincide with changes in your risktolerance.

Overindulgence in information can lead to poor decisions, and excessive monitoring of your retirement account balance can result in stress. Checking your retirement account balance too often can have a psychological impact on you. Therefore, exploring the optimal frequency for checking your retirement account is essential.

Preparing for retirement is a significant life transition that demands a clear understanding of your financial situation. This data can serve as a baseline for tailoring your retirement plan, taking into account factors such as inflation, your current age, and your desired retirement age.

Track your retirement. Ad Online Financial Advisors are ready to provide you with quality economic planning and investment management. Did you know you might be able to actually retire with $1 million? Take a few minutes to read my case study right here: [Case Study] Can You Retire Early with Only 1 Million Dollars?

When failure is not an option However, where we are in our life cycle largely determines just how much risk we can take and whether we have the time necessary to pick up the pieces in the event of failure. If you’re reading this and approaching or in retirement, you’re going to need a different solution.

based on the investor’s goals, risktolerance, and investment horizon. For instance, you can have an aggressive portfolio if you have a high-risk appetite and are inclined towards earning aggressive returns. For investors having a higher risktolerance, more funds will be allocated to stocks in an aggressive portfolio.

Investing is essential to achieving our financial goals, whether saving for retirement, funding our children’s education, or building wealth for the future. They are professionals who hold specialized degrees or certifications in finance, economics, or related fields.

Inflation is currently at 40 year highs with increasing signs of slowing economic growth. A few other tailwinds that bode well for dividend-paying stocks include historically high levels of corporate cash, low bond yields, and a demographic of baby boomers needing income to last throughout retirement.

Their primary objective is to help clients make informed investment decisions, manage risks, and achieve financial objectives. Investment advisors analyze market trends, assess the client’s economic situation, and develop personalized investment strategies tailored to their goals and risktolerance.

Precious metals like gold and silver have been sought after for centuries as a store of value and a hedge against economic uncertainties. Each of these alternative investment options offers its own set of risks and rewards. Assess Risk and Return Profiles Consider your investment goals, risktolerance and time horizon.

Precious metals like gold and silver have been sought after for centuries as a store of value and a hedge against economic uncertainties. Each of these alternative investment options offers its own set of risks and rewards. Assess Risk and Return Profiles Consider your investment goals, risktolerance and time horizon.

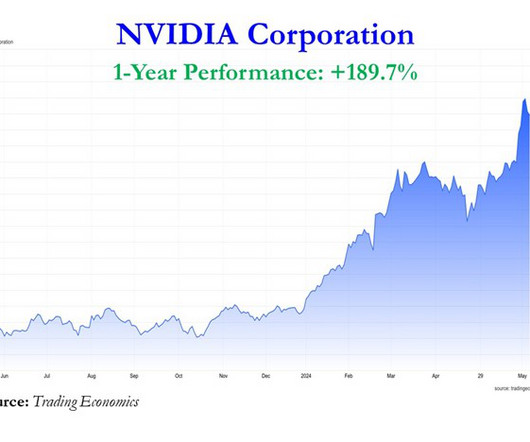

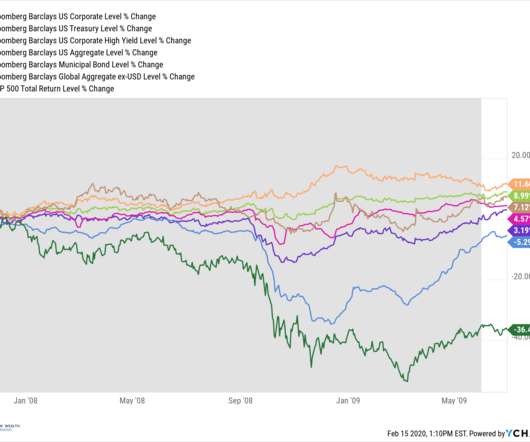

Bad economic news turned out to be good news for stocks. This time around, good economic news meant bad news for stock prices, primarily because the Federal Reserve was slamming the brakes on the economy by increasing the Federal Funds interest rate target. The S&P 500 surged +16.3% (see chart below). What did the stock market do?

Assess your risktolerance: Cryptocurrencies are known for their volatility, with prices that can fluctuate significantly in a short period. Avoid relying solely on crypto for critical financial goals like retirement. When investing in cryptocurrencies, securing your assets is crucial due to the risks of theft and hacking.

A recession is defined as a temporary period of economic downturn. A country is considered to be in recession if its Gross Domestic Product (GDP) has witnessed negative economic growth for two consecutive quarters. A recession is a stage in the economic cycle that is bound to recur over time.

These services typically include: Wealth Management: Advisors can offer customized investment portfolios aligned with your risktolerance, time horizon, and financial objectives. This plan may cover estate and retirement planning, college savings, debt management, and more.

When choosing between RSUs and NQSOs, you should consider personal concentration risk and plan for how much you should have allocated in your company’s stock. Understand Your Investment RiskTolerance. Investment risktolerance ranges from conservative to aggressive in most discussions.

It is essential for your investment portfolio to align with your unique financial goals, risktolerance, and time horizon. Similarly, the professional may advise investing in different instruments for goals such as retirement planning, funding your children’s education expenses, buying a home, or other objectives.

Regular updates should include insights into market conditions, economic trends, and how these factors impact your investments. If you are retired, you must make sure that your financial advisor possesses a strong understanding of Social Security taxes. Transparent communication is paramount in risk management.

Imagine you make enough money through investments and savings that you can retire early. Keep working toward financial independence Related posts on financial independence We'll discuss how you can become financially independent to retire early through the FIRE (financial independence, retire early) method. What is FIRE?

Adding another layer, the stocks in your portfolio can be across economic sectors like pharmaceuticals, finance, and petroleum. . Building on diversification, asset allocation is an investment strategy that builds your portfolio by weighing an adequate amount of risk for your goals. Asset Allocation. Building Your Strategy.

Taking steps to help ensure you’re reasonably prepared for any type of economic uncertainty or recession, personal financial crisis (loss of a job, divorce, medical expenses, etc.), Trying to anticipate and subsequently prepare for the next market correction/recession/etc. is a fool’s game. So many things to say here.

Crafting a Comprehensive Financial Plan: This includes a detailed net worth statement, defining SMART Goals including retirement, children education etc., and a risktolerance analysis, all of which are sculpted around an individual’s circumstances.

These investments serve not only to grow their wealth but also to protect it against market volatility and economic downturns. They are characterized by rapid economic growth and increasing integration with the global economy. Political unrest in these regions can disrupt economic activities and erode investor confidence.

A financial plan is a comprehensive blueprint designed to help you meet your financial goals, whether that’s achieving a comfortable retirement, sending your kids to college, or planning for unforeseen events. Exploring Illustrative Economics Consider the comparison below between a pre-tax retirement account and a post-tax alternative.

This especially becomes true in the distribution phase of your retirement when you are relying on your portfolio to provide income. I had many clients that began to feel the pinch of rising costs after they retired. If you are retired or close to retirement, inflation can erode the value of your savings. Warren Buffett.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content