This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Estateplanning is one of the most important steps in securing your financial legacy, but its also among the most complex. Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year.

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

For high-net-worth individuals, continuously refining your strategy over time is what keeps your plan efficient and aligned with evolving goals. She wants to minimize taxes while aligning her legacy with charitable values. Individual results will vary based on specific financial circumstances.

No required minimum distributions (RMDs) for the original account owner Unlike IRAs and qualified retirement plans, a Roth IRA is unique in that required minimum distributions are not required during the original account owners lifetime. A spouse may also elect to defer RMDs if they inherit the account.

A financial advisor can help with maximizing your retirement income through taxplanning After retirement, your income sources may become limited to pensions, Social Security benefits, and investment income. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income.

In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations. From maximizing deductions to managing capital gains, we’ll cover everything you need to know about smart taxplanning.

The Tax Cuts and Jobs Act of 2017 eliminated recharacterization, transforming Roth conversions into permanent decisions requiring thorough analysis before execution. Roth IRAs offer unique advantages including tax-free growth, no required minimum distributions during the owner’s lifetime, and potential tax benefits for heirs.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

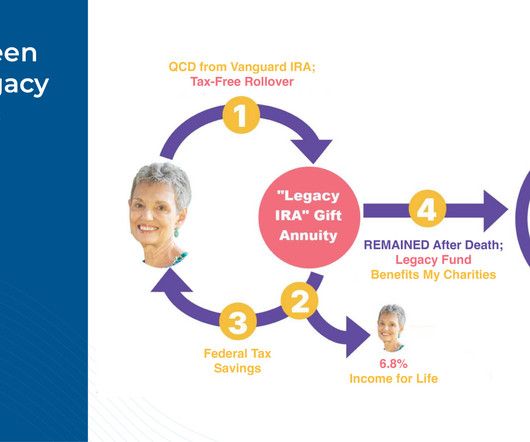

What Are Qualified Charitable Distributions (QCDs)? For those over 70½, you might already be familiar with Qualified Charitable Distributions (QCDs). For years, QCDs have allowed people to donate directly from their IRAs without paying taxes on those distributions.

Only 26% of Americans have an estateplan. If you’re thinking, “But my clients are high-net-worth…many more have an estateplan.” These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions.

Unlocking the Power of Net Unrealized Appreciation (NUA) Many workers receive company stock as part of their compensation package or can take advantage of a company 401(k) plan, choosing from a menu of mutual funds, exchange-traded funds and company stock for their investments. The remaining assets may be rolled over.

Blind Spot 3: Inadequate estateplanning In today’s age, where 60 is the new 50 and people are more active and health-conscious than ever before, it is common to think that estateplanning can wait. Life is inherently unpredictable, and unanticipated circumstances can arise at any moment.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. They are well-versed in various aspects of financial planning, including investments, retirement planning, estateplanning and tax management.

Financial Planning Needs: Retirement planning Education and family planning Obtaining appropriate insurance coverage Business and taxplanning Significant asset purchases Strategies for Serving Clients in This Stage: Clients at this stage are experiencing life events — both large and small — that will impact their financial planning needs.

When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median underperformance was almost -10%.³ Taxes should always be a component of any investment decision — but not the main driver. If so, there might not be any material tax impact from selling shares.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. They are well-versed in various aspects of financial planning, including investments, retirement planning, estateplanning and tax management.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Retirement planning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estateplanning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

Key Takeaways: Accounting advisory services extend beyond traditional tax preparation to offer strategic financial guidance. Specialized areas can include estateplanning and tax-efficient investment strategies.

While it may seem like a luxury that is only available to the wealthy, anyone is capable of building an effective financial plan and putting it into action. Without effective personal financial management, you risk losing money to poor budgeting, poor taxplanning, or even just to inflation.

The donor relinquishes ownership of the assets but retains advisory privileges over how the contributions are invested and how grants are distributed to charities. Donations to a DAF are tax-deductible in the year they are made, which can help reduce the donor’s taxable income.

A great way to save for college costs (and even K-12 education) is with a 529 plan. A 529 plan is a state-sponsored tax-advantaged way to save for education. While contributions are after-tax, both investment gains and qualified distributions are tax-free. . Check-In On Your EstatePlan.

It’s important to note that tax advisors include three types of tax professionals : Certified Public Accountants (CPAs) Enrolled Agents (EAs) Tax Attorneys All three may offer different fee structures depending on the services offered and their firm’s unique expertise.

presidential election, we have grappled with the lack of clarity regarding the details of new tax legislation. The outcome of the tax reform debate is likely to impact how we advise clients on taxplanning, estateplanning and a host of other topics. are distributed to beneficiaries.

If you want to donate a certain amount to charity over a period of time, a donor-advised fund allows you to take the entire donation as a tax deduction in the first year, but then contribute to the charity over time. Additionally, the funds in the account can grow tax-free. The charity just needs to be a registered nonprofit.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. Possible future increases in income and wealth transfer taxes, including the potential reversion of certain elements of the U.S.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. Possible future increases in income and wealth transfer taxes, including the potential reversion of certain elements of the U.S.

Rather than reacting to market fluctuations or headlines, they build a plan based on data and long-term strategy, helping you stay on course even when the market is volatile. Failing to do so could mean losing a substantial portion of your returns to taxes, which ultimately defeats the purpose of investing.

The second amendment to the revocable trust agreement directed the following distributions: • 2 million dollars to the trustee of the MCC Trust, to be held for Maria’s benefit. The MCC Trust agreement included terms about the distribution of trust assets: 3.2. Administration of Trust Estate for Beneficiary.

The key to creating a diversified portfolio is to distribute your money across multiple asset classes, such as stocks, bonds, real estate, and alternative investments. A financial advisor can recommend investment strategies, risk management tips, taxplanning methods, estateplanning tips, and other financial approaches.

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges. This allows the account to grow on a tax-deferred basis, with income to beneficiaries being taxed when distributions are made. Read More.

Act, passed in December 2022, created the ability for individuals over age 70 1/2 to make a one-time Qualified Charitable Distribution (QCD) of up to $50,000 of IRA funds into a CGA, with the amount distributed to the CGA being excludable from the donor's taxable income. But the SECURE 2.0 legislation at the end of 2022. Read More.

Make sure they take their required minimum distributions Clients who are age 73 or over must take required minimum distributions (RMDs) from their qualified plans and IRAs. Businesses There are several steps that business owners may want to take in 2022 to minimize taxes.

With proper planning and professional advice, you can enjoy a secure and fulfilling retirement while effectively managing your healthcare costs and ensuring peace of mind for the future. Pillar 3: TaxplanningTaxplanning is indispensable for optimizing your retirement finances and safeguarding your wealth for the future.

But for those interested in charitable giving, there may be a way to address the tax concerns associated with highly appreciated assets and give meaningfully over time. Receive income : During the term of the trust, youor other designated income beneficiariesmay receive an annual distribution from the trust.

If you are over 73 you should be starting to take requirement minimum distributions. Do so before year-end and plan for next years RMD now. Make sure you have some liquidity to meet RMDs in case your portfolio is in a drawdown when you need to take your distribution. EstatePlanning Do you have a trust and will?

Key Takeaways: Net Unrealized Appreciation (NUA) is the difference between the cost basis of employer securities in a retirement plan and their market value at the time of distribution. NUA is not taxed as ordinary income at the time of distribution, which can offer significant tax advantages.

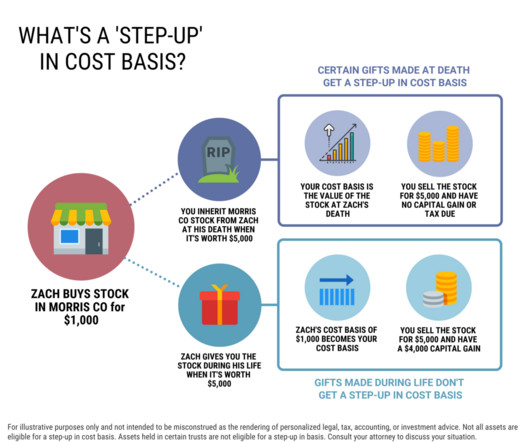

Inheriting a Trust Fund: Distributions to Beneficiaries Do You Pay Tax on an Inheritance? At a high level, if the asset is part of the decedent’s estate it’s typically eligible for a step-up. This can get very tricky so it’s important to work with the estateplanning attorney settling the estate.

These services often include recommendations on investments, financial planning, retirement, Social Security, Medicare, taxplanning, and other wealth-related topics. An hourly financial advisor is someone who provides financial advisor for a set hourly rate. Hourly financial advisors are not common. Jon Luskin. Rick Ferri.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content